Responsive Industries Limited (RIL) is a leading manufacturer of PVC Products with the following product verticals –

Sheet Vinyl Flooring

Synthetic Leather

Luxury Vinyl Tile (LVT)

Synthetic ropes

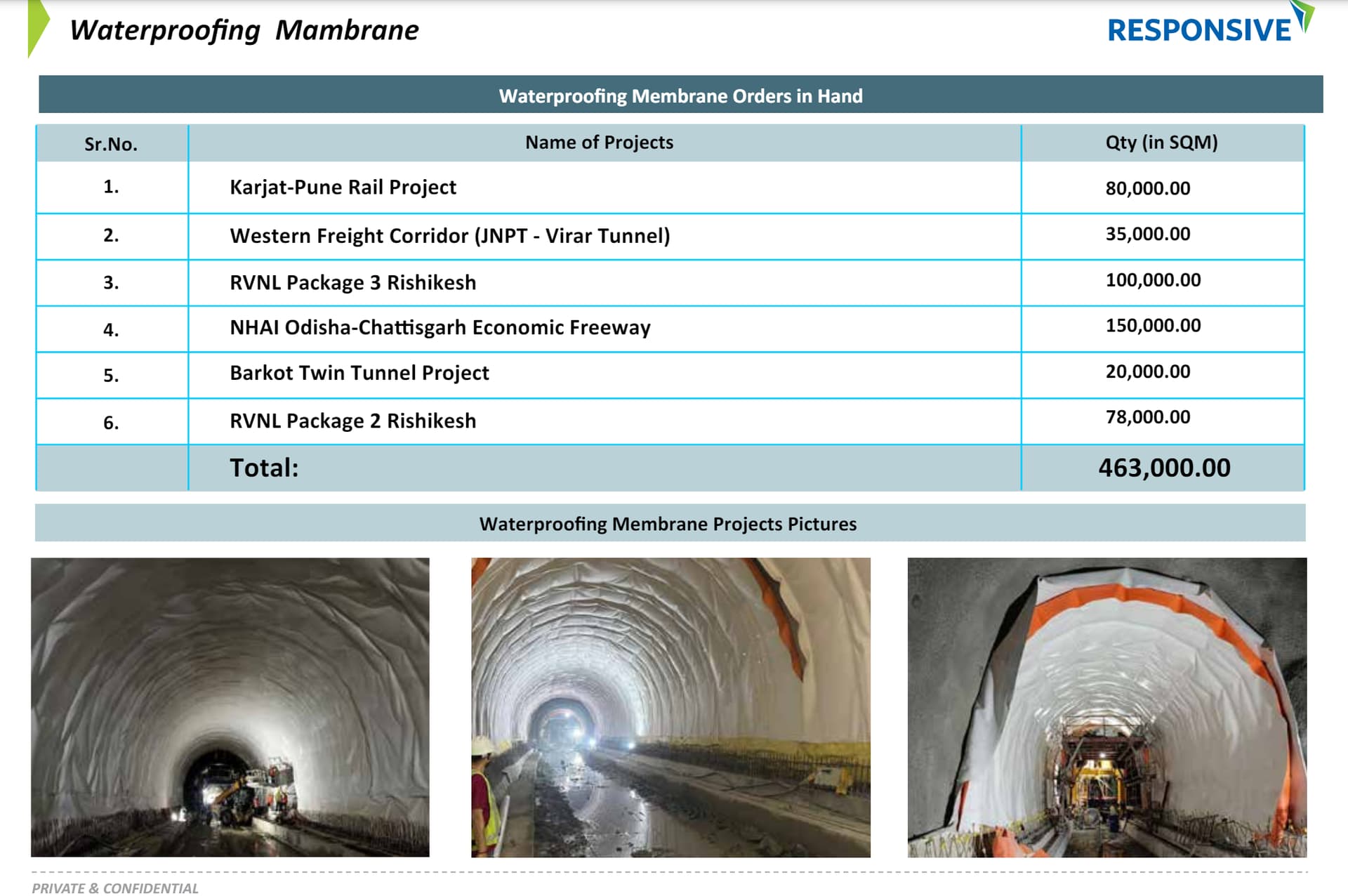

Waterproof Membrane

It is the largest Indian producer of PVC flooring and synthetic leather cloth and caters to healthcare, hospitality, transportation, retail, sports 6 infrastructure and real estate sectors. It is amongst the top 4 producers of vinyl flooring globally.

The promoters have extensive experience in the PVC (Poly Vinyl Chloride) flooring products and shipping ropes industry. It has been almost four decades since the company began in the -verified tiles and Indian flooring market, which was dominated by mosaics or conventional materials like carpets. Now they are in the period of evolution. Over time, they have seen a rapid pace of development in the flooring industry and the preferences of flooring have migrated from hardwood to ceramic, then to laminate and now from laminate to resilient or vinyl flooring. Luxury Vinyl Tile (LVT), Stone Plastic Composite (SPC) besides this the company has entered into waterproofing membranes, which has sparked the industry and is expected to be the next biggest evolution in flooring.

Manufacturing Facility and Subsidiaries:

It has a state-of-the-art factory and infrastructure set-up at Boisar in Palghar district in Thane, spread across 52 acres of land, having 15 manufacturing lines. The Company has 1 Indian subsidiary - Axiom Cordages Limited, 3 wholly owned foreign subsidiaries - Responsive Industries Limited (Hong Kong), Responsive Industries Limited LLC USA and Responsive Industries Limited (Singapore) and 1 foreign step-down subsidiary - Axiom Cordages Limited (Hong Kong). It has a presence in the shipping ropes business through its subsidiary Axiom Cordages Limited.

HK subsidiary has manufacturing operations in China with an additional 5 million SFT / month capacity for Luxury Vinyl Plank

Luxury Vinyl Planks:

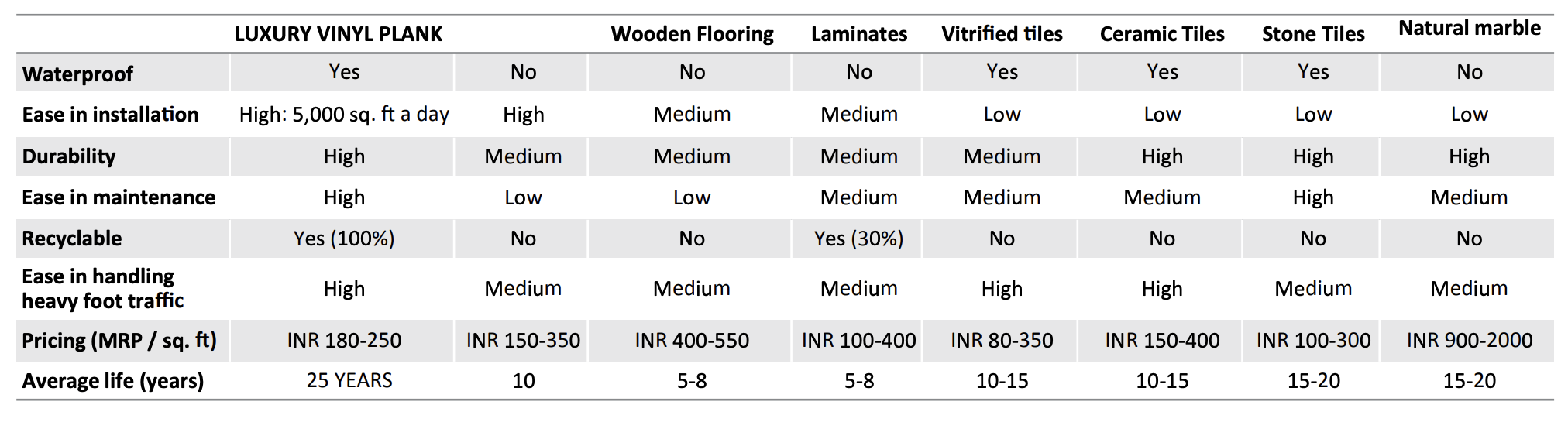

Luxury Vinyl Plank is a 100% waterproof wooden and tile visual that replaces laminate, hardwoods, engineered woods, carpet, and ceramic tiles.

Among the flooring products, Luxury Vinyl Tiles (LVT) is gaining prominence across the globe, due to its superior qualities.

The Company has introduced a new type of IMPACT flooring which is hard layer interlocking flooring in wide range of looks substituting wooden flooring, marble, granite and tiles.

It is very easy to use and fast to lay, environment friendly as well as good in cost and looks. It is so easy and fast to install, full large area can be covered in hours where it would take days to do so.

LVP’s click system is so easy that it is marketed as DIY (do-it-yourself) installation in Western countries.

80% of LVP is residential with 20% commercial split between offices, retail and hospitality

In 2022, LVP outsold Ceramic Tile in the USA. Vinyl Flooring has tripled in market size in the last 15 years. Outsold traditional hardwoods and engineered flooring last 5 years

US market prediction for LVP at 72 Billion $ by FY 2027

QoQ sales are profits are rising rapidly. The company has shifted from loss to Profit. Maybe their new LVT product is getting acceptance in the export market.

As margins have moved higher lately, I tried to look underneath the reasons for this change. Below are some of the interesting items that I found which are possibly contributing to this change in trajectory for Responsive:

Responsive launched Vinyl Flooring business in the US by setting up a subsidiary on March 06, 2020 (just before the Covid lockdowns started in the US). Their US business grew > 100% for FY2023 according to the AR. It will be very interesting to see how their US business did in FY2024 when AR is released.

FY2021

FY2022

FY2023

Turnover (cr)

5.3

90.4

194.6

Luxury Vinyl Tile as a flooring category has been making great progress in the US flooring industry. LVT has surpassed carpet in 2022. LVT category represented 23.1% of the entire floor covering industry in terms of volume in the US. Below lines from this article shows how LVT is gaining market share from other flooring alternatives in the US:

Of course, it’s the rigid core subsegment of the resilient flooring category that is driving the overall growth—not just in resilient but for the industry as a whole. FCNews research found rigid core (SPC/WPC) garnered 60% of total resilient sales in 2022 and 47% in volume. That translates to $5.727 billion in sales and 2.87 billion square feet. Compare that to 2021 when WPC/SPC claimed just 45.6% of total resilient sales and 34.8% of volume ($3.845 billion in sales and 2.047 billion square feet.)

That growth in sales and volume is even more impressive when compared to 2020, when rigid core checked in at just $2.617 billion and 1.63 billion square feet. That means rigid core’s claim has essentially doubled in just two years. To put this in perspective, total LVT sales just eight years ago was $1.45 billion. So, rigid core alone is nearly quadruple the entire LVT market in 2015.

I highly recommend reading these two articles as it shares a lot of numbers around how LVT and flooring industry performed in 2023.

About 80%-85% of resilient floor (LVT is a majority portion) is imported by the US and mainly supplied by China.

“2022 was a significant year in that a fair amount of that domestic capacity came online, specifically in the world of SPC,” Mannington’s Sheehan said. “For us, we’ve been the one and only WPC producer here. Our domestic business has continued to increase and you had at least five to six additional plants come online in 2022 and a fair number of retailer and OEM opportunities began to take shape in 2022. So, whereas this category was probably 90%-95% imports, that shifted down to about 80%-85% in 2023. There was a significant amount of domestic capacity that began to ship into the market in 2022.”

LVT is quickly becoming the largest flooring category in the U.S. Our sources generally agree that imports account for roughly 80% of domestic consumption and even more for rigid core. Like America, Asia is rich with the raw materials needed and has created economies of scale around the growing category.

“All the cost advantages shifted to Asia,” says David Thoresen, senior vice president of business development for Nox, an OEM supplier based in Korea with a factory in Ohio, as well. “The infrastructure you need to manufacture PVC-based flooring is all in Asia. You can buy PVC more competitively, you can buy the equipment more competitively, and the labor is obviously cheaper.”

US imposed 25% tariff on China made LVT in late 2020 which has made local brands to look for alternatives to China and also manufacture onshore. It just probably made Progressive’s presence in the US as being at the right place at right time. Progressive has their own warehouse in Simpsonville, South Carolina stocking supplies and increasing their distribution network by adding new distributors at ground level here.

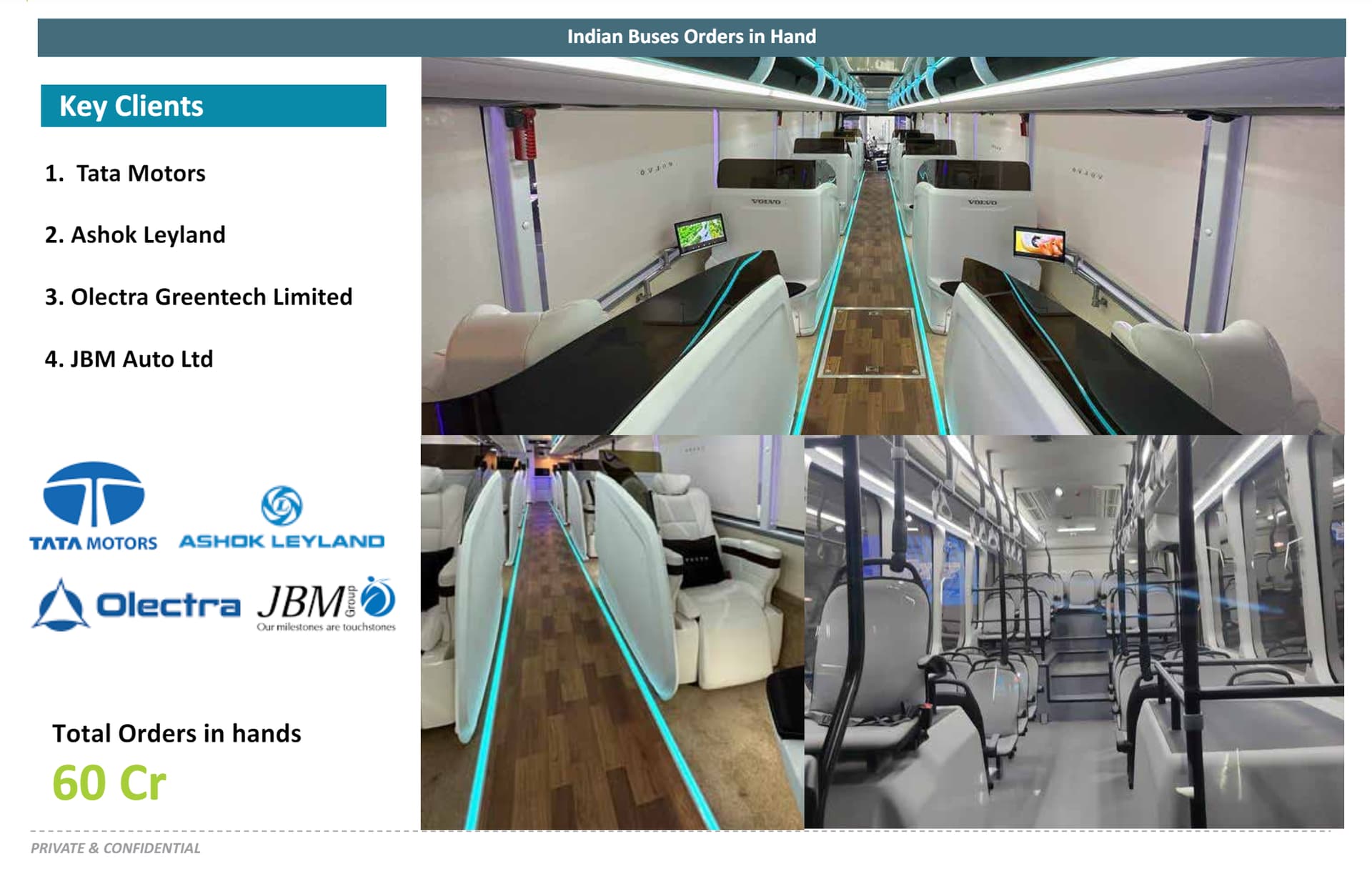

Indian government imposed anti-dumping duty on imports of LVT from China and Taiwan in April of 2023 possibly increasing in Vinyl high value add flooring margins with Railways and E-buses.

As per their first con-call for Q4FY24, management shared that its able to sell higher value/margin products due to better demand from Indian Railways as its upgrading the specifications of floors in a meaningful way. Also, they are able to sell these higher margin products with increased demand from e-buses by Tatas, Marcopollo, etc.

Local Scuttlebutt findings:

One of their distributors All South Flooring happened to be few miles away for me. They confirmed that they have been buying LVT from Responsive since 2021 as they were looking for China alternatives. They sell it forward to local dealers/installers through their own brand and not through Responsive’s brand. They have found Responsive to be very good with their product quality. I also visited local nearby installers referred by All South who are their customers. I saw them stocking All South branded LVT floors in their shops along with competitor’s to be sold to the end consumer.

LVT’s main USP is its durability, water-proof, scratch proof features as compared to hardwood and carpet. Due to advanced technology – LVT can now replicate the shape and feel of real wood planks with patternless precision. This has been the case for last 6-7 years, imho. It has really picked up after getting the authentic wood like look of LVT. Same evolution as quartz countertop – where it picked up after quartz designs improved so well that they were able to replicate the grains and variations of an exotic natural granite on a quartz counter top. Something similar has happened with LVT, imho.

Lower end LVT has been picking up quite well in commercial applications too.

End applicator/installer is the one who is going to guide the customer in choosing between hardwood and LVT/LVP product and hence plays a critical role in decision making process for the buyer.

There are certain areas where carpet, hardwood, tile cannot be replaced by LVT from application standpoint. But LVT has big room to creep into from both carpet and hardwood for new installations along with remodeling installations.

Opportunities:

US flooring market. Ventura’s research report is projecting whopping 1020cr revenue of US business by FY27. It is very bold projection but something that is achievable given current tailwinds for Responsive, imho. Even if they land 20-30% short of 1000cr by FY2027 and maintain the margins - I think the business will be in a different orbit.

India residential market is completely untapped market as far as LVT is concerned. Very difficult to crack but size of opportunity is huge.

B2B demand from railways, e-buses, hospitals, sports centers, gyms has been picking up well and can grow many folds from here.

Synthetic Ropes and PVC specialized covers offer good margin and decent growth

Management has stated that the current capacity is good enough to do Rs. 2500cr topline.

Risks:

PVC commodity price risk. Sudden spike in PVC prices can erode margins just like it did in FY22 and FY23.

Tariffs imposed by US government on any Indian imports for LVP products.

Current starting valuation is not desirably cheaper

Links to Videos/Articles/Research Reports to better understand the opportunity that lies ahead for Responsive:

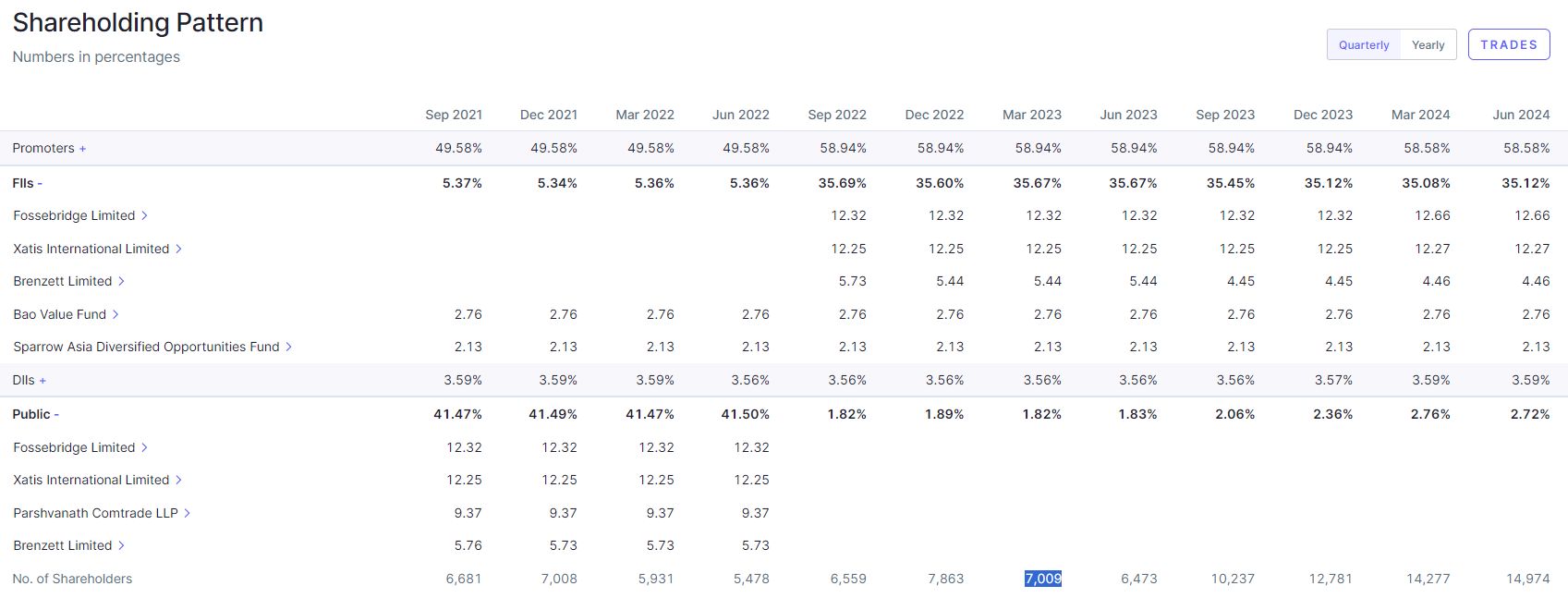

If you look at the shareholding, in September 2022, there’s no actual increase in FII shareholding, earlier there were three companies in public shareholding data- Fossebridge limied, Xatis international, and Brenzett limited and these 3 companies were shifted to FII shareholding from public shareholding(I don’t know why). All 3 are registered in British Virgin Island and their beneficial owners are Baidyanath Mahto, Kalpana Kole and Meera Ghosh. Also these 3 companies holds only Responsive Industries shares.

The promters are also not indviduals but different companies registered with the same directors or owners . The increase in promoter % also is a transfer of entire stake from Prashavnath comrade llp to Fairpoint tradecomp llp.

I have looked at the holding breakdown. I would let the regulators do their work and not worry about it until something negative is officially announced by the regulator. It’s just me and how I process these kind of items - which might not be the right approach for someone else.

The entities you have mentioned have been holding the stake for last many years now. Public shareholding has gone up by ~1% since March of 2023 which has been supplied by FII and Promoters. Available float is just 2%-3%. 150cr-200cr max given current market cap.

Two things can happen when float is so low, in my view. Either these entities might offload more which can act as overhang on the price and one can get an idea that “smart money” and insiders are cashing out. Or there can be crazy momentum on the upside, if the demand from new investors starts to roll in as business execution continues. So one would have to keep a close eye on no of shareholders and future shareholding breakdown.