I am new to this forum but have been investing since 5 years. I have recently come across Resonance Specialities - Mumbai based Chemical Company. They are in the business of producing API and Drug Intermediaries which are used in pharma and agri sector (feed for animals).

I found this stock worth considering but wanted opinion of the forum here

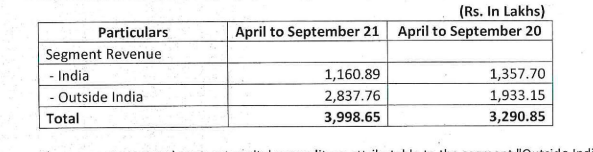

Financials:

In last 3 years , revenue has gone from 43 cr to 71 Cr

20% Net Profit Margin

PE : 16.4% , Sector PE : 22%

Pros:

Stable client base with relation lasting a decade

Focus on R&D for cost optimization

60% revenue from exports

Cons

Some of the raw materials are imported. thus susceptible to FX changes. However company is trying to mitigate this.

High Working Capital use

Growth Plan is not specified in detail.

No indication of capacity expansion

Credit Report:

There recent credit rating has been bumped to ‘Stable’ by CRISIL. Below is the report

Their main product is Pyridine, which is a versatile chemical used in the manufacture of agrochemicals, pharmaceuticals & bulk drugs, dyes, rubber chemicals, etc.

The financial performance has been consistent and improving over the quarters, with such a small-scale company the optionality of getting big is quite possible given that the specialty chemicals and chemicals sector has a huge tailwind due to pharma & API.

Post Acquistion by the IPCA group last year, I am quite confident of the sustainability of the financial performance and corporate governance even with the small size in coming years.

The company’s plant is located in the Tarapur Industrial Zone near Mumbai , India. The plant is spread across 32,000 square meters of land with class one structures. The company has plants to manufacture Pyridines, Picolines, Lutidines, Collidines, Cyanopyridines and for various value added products.

Resonance Specialties’s business

Resonance produces value added drug intermediates & APIs.

The company is presently producing nutritional products such as:

Zinc Picolinate: Zinc picolinate is the zinc salt of picolinic acid which has the molecular formula Zn(C₆H₄O₂N)₂. Zinc picolinate has been used as a dietary zinc supplement.

Chromium Picolinate: Chromium(III) picolinate (CrPic3) is a chemical compound sold as a nutritional supplement to treat type 2 diabetes and promote weight loss.

Chromium Polynicotinate: Chromium(III) nicotinate is an ionic substance used for chromium supplementation in some nutritional products, where it is also referred to as chromium polynicotinate .

Niacinamide: Niacinamide or nicotinamide (NAM ) is a form of vitamin B3 found in food and used as a dietary supplement and medication.

Isoniazid: Isoniazid , also known as isonicotinic acid hydrazide (INH ), is an antibiotic used for the treatment of tuberculosis.

Picolinic: Resonance is also India’s first and largest manufacturer and exporter of important drug intermediates such as Picolinic and Dipicolinic acid. Picolinic acid is a bidentate chelating agent of elements such as chromium, zinc, manganese, copper, iron, and molybdenum in the human body. Many of its complexes are charge-neutral and thus lipophilic. After its role in absorption was discovered, zinc dipicolinate dietary supplements became popular as they were shown to be an effective means of introducing zinc into the body.

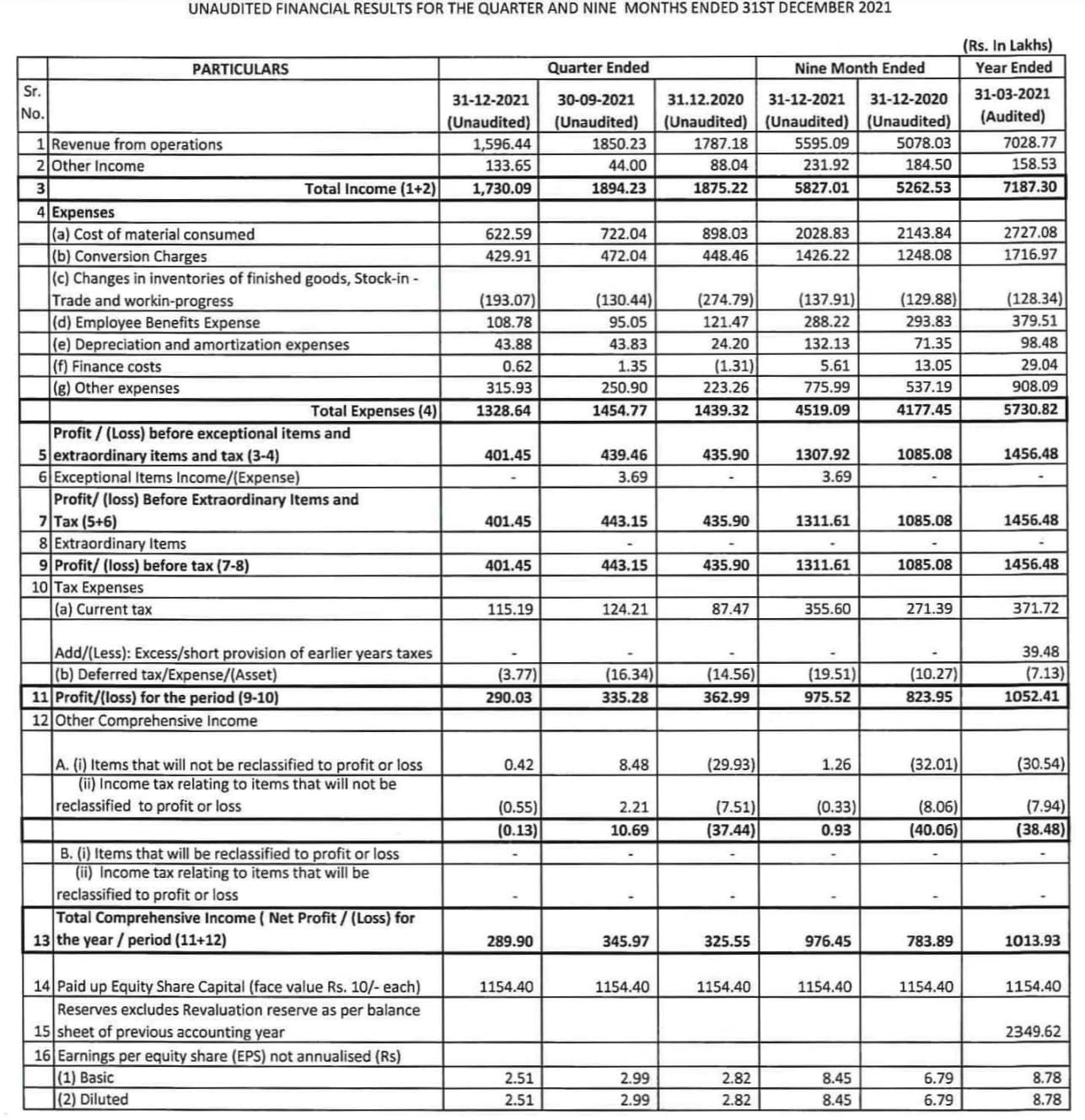

Okayish result, was happy to see the stock price held on, in the recent carnage. Guess the market was expecting a good result, let’s see how it reacts to these numbers on Thursday 27th Jan '22.

@Sachin_12 , They do not conduct any calls as per my knowledge. There could be ups & downs in revenue at this scale, I think. I am not reading too much into it. I hope business keeps growing as the sector grows, there is a tailwind for the spec chemical sector. Given that Resonance is one of the key players in Pyridine & picolines products in India It will keep growing.

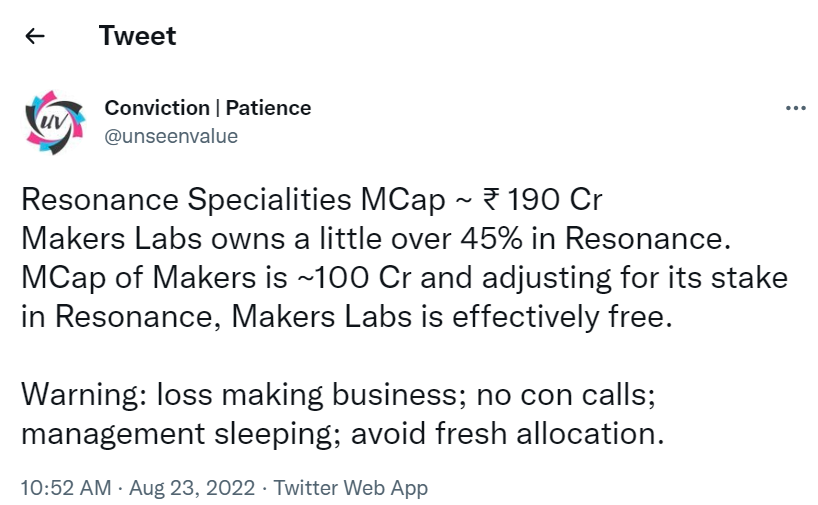

I have taken stake in this through Makers Lab which actually holds main control of Resonance.

And Makers lab is none other than IPCA promoters.

Now why not in Resonance directly. Because resonance is actually a good consistent profit making company. But Makers has turned from net loss to net profit this year.

So I personally feel Makers is far undervalued than Resonance.

Thats why.