Equity Research: Ind Swift Laboratories Ltd

Company Overview

Ind Swift Laboratories Ltd (ISLL) is a prominent player in the Indian pharmaceutical industry, with a strategic focus on the formulation business. The company recently completed a slump sale of its API and CRAMS business to Synthimed Labs for ₹1,650 crore on March 18, 2024, allowing it to reduce debt and concentrate on higher-margin formulation products.

Key Highlights

- R&D Capabilities: ISLL retains significant R&D capabilities at its Thane Center, focusing on formulation development and process R&D.

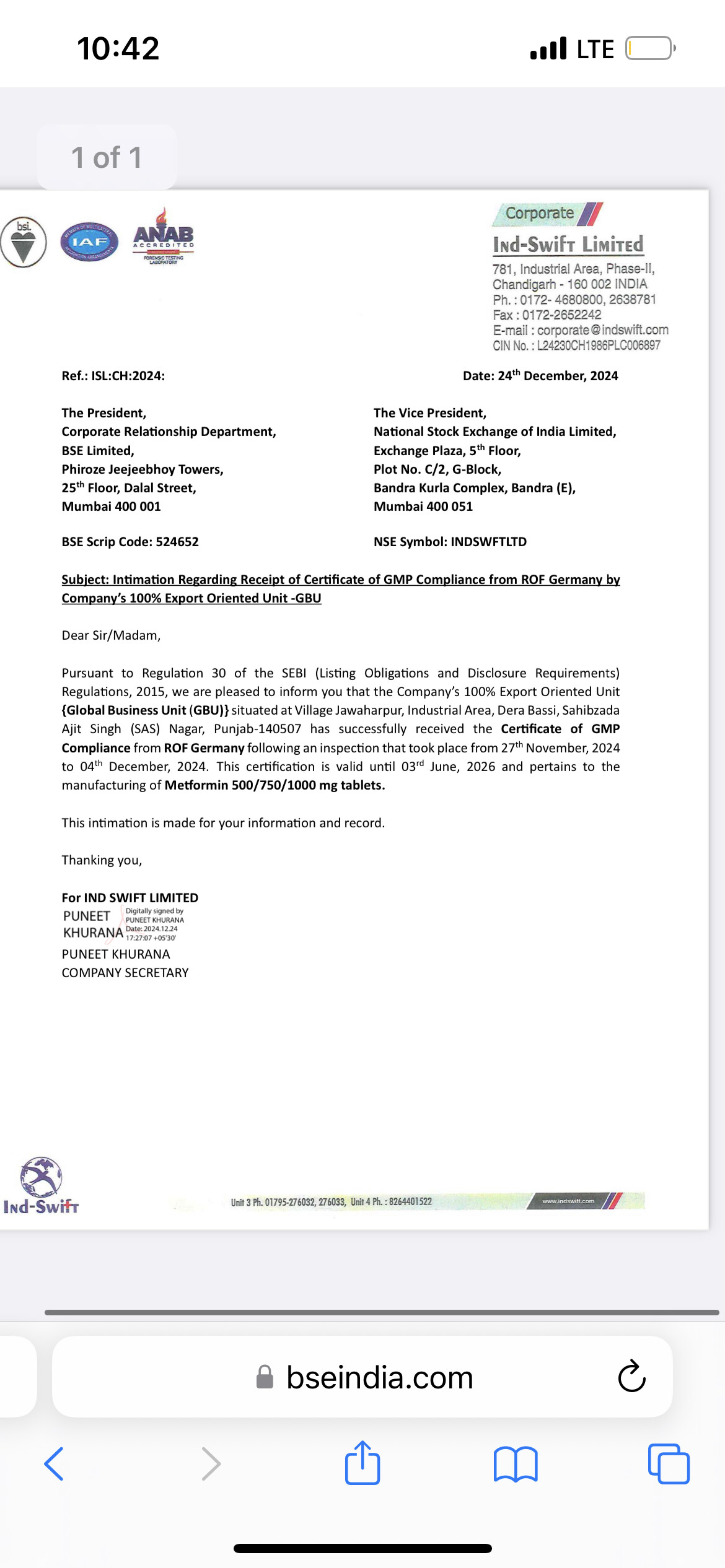

- Manufacturing Facilities: The company operates multiple manufacturing facilities across India, including locations in Punjab, Jammu & Kashmir, and Himachal Pradesh, dedicated to the production of pharmaceutical formulations.

- Strategic Shift: The sale of the API business provides the necessary capital to reduce debt and invest in the formulation business.

- BIOSECURE Act: The U.S. legislation encouraging diversification away from Chinese suppliers presents significant export opportunities for Indian pharmaceutical companies.

- Management Experience: The management team has over three decades of experience in the pharmaceutical industry, providing a strong foundation for future growth.

- Future Plans: As per the 2024 AGM, the company plans to pursue a Follow-on Public Offering (FPO) for expansion, indicating a focus on organic growth without increasing debt.

Financial Overview

- Current Market Price: ₹137.34

- Book Value: ₹158

- Debt Reduction: The proceeds from the slump sale are expected to significantly reduce the company’s debt, improving its financial health.

- Valuation: The stock is trading at a relatively low price-to-earnings (P/E) ratio of around 6 compare to Avg Industry PE of 33, indicating potential undervaluation.

Examples of Successful and Unsuccessful Pivots from API to Formulation Business

- Dr. Reddy’s Laboratories

- Period of Pivot: Early 2000s

- Reason for Success: Dr. Reddy’s Laboratories successfully transitioned from API manufacturing to formulations by focusing on generic drug development and entering regulated markets like the USA and Europe. Their success was driven by strong R&D capabilities, strategic acquisitions, and a robust pipeline of generic drugs.

- Sun Pharmaceutical Industries

- Period of Pivot: Late 1990s

- Reason for Success: Sun Pharma shifted its focus from APIs to formulations, particularly in the specialty and generic drug segments. The company achieved success through strategic acquisitions, such as the purchase of Ranbaxy Laboratories, and by expanding its presence in regulated markets.

- Teva Pharmaceutical Industries

- Period of Pivot: 2000s

- Reason for Success: Teva transitioned from API manufacturing to becoming a global leader in generic formulations. The company’s success was due to its extensive product portfolio, strategic acquisitions, and strong presence in key markets like the USA and Europe.

- Aurobindo Pharma

- Period of Pivot: Early 2000s

- Reason for Success: Aurobindo Pharma successfully pivoted from APIs to formulations by focusing on generic drug development and entering regulated markets. The company’s success was driven by its strong R&D capabilities, strategic partnerships, and a diversified product portfolio.

- Wockhardt

- Period of Pivot: Late 1990s

- Reason for Failure: Wockhardt faced challenges in its pivot from APIs to formulations due to regulatory issues, quality control problems, and financial difficulties. The company struggled to maintain compliance with international regulatory standards, leading to import bans and loss of market share.

Analogy with Ind Swift Laboratories Ltd

Ind Swift Laboratories Ltd is well-positioned to replicate the success of companies like Dr. Reddy’s, Sun Pharma, and Teva due to several factors:

- R&D Capabilities: ISLL retains significant R&D capabilities at its Thane center, focusing on formulation development and process R&D.

- Financial Strength: The company has a substantial cash reserve of ₹432 crore from the slump sale, providing the necessary capital for expansion.

- Management Experience: The management team has over three decades of experience in the pharmaceutical industry, providing a strong foundation for future growth.

- Strategic Focus: The company’s strategic shift towards formulations aligns with industry trends and offers significant growth potential.

- Organic Growth Strategy: The plan to pursue an FPO for expansion indicates a focus on organic growth without increasing debt, reducing financial risk.

Pros of Investing in Ind Swift Laboratories Ltd

- Debt Reduction: The sale of the API business will significantly reduce the company’s debt, improving its financial stability.

- Focus on Formulations: The strategic shift towards formulations, which offer higher margins, positions the company for better profitability.

- R&D Capabilities: The retained R&D facilities and expertise in formulation development provide a strong foundation for new product development.

- Export Opportunities: The BIOSECURE Act and increasing demand for pharmaceutical products in regulated markets like the USA present significant growth opportunities.

- Management Experience: The experienced management team and their industry contacts can drive expansion and growth.

- Organic Growth Strategy: The plan to pursue an FPO for expansion indicates a focus on organic growth without increasing debt, reducing financial risk.

Cons of Investing in Ind Swift Laboratories Ltd

- Market Competition: The formulation market is highly competitive, with established players like Dr. Reddy’s, Sun Pharma, and Aurobindo Pharma.

- Execution Risk: Successfully transitioning from API to formulations requires effective execution of strategic plans and maintaining high-quality standards.

- Dividend Policy: Despite reporting profits, the company has not been paying dividends.

- Market Volatility: The stock price has shown significant volatility, which may concern risk-averse investors.

Conclusion

Ind Swift Laboratories Ltd has the potential to successfully pivot to the formulation business, given its strong R&D capabilities, regulatory approvals, and strategic focus. The company’s experienced management team and the opportunities presented by the BIOSECURE Act further enhance its growth prospects. Investing in ISLL at a price below its book value of ₹158 could be a prudent decision for those looking for undervalued stocks with growth potential.

Recommendation

Buy: Given the company’s strategic shift, debt reduction, and growth opportunities, ISLL appears to be a good investment at any price below its book value of ₹158.

Disclaimer:

I am not a registered equity research analyst under the Securities and Exchange Board of India (SEBI) regulations. The information provided in this report is based on publicly available data and personal analysis. I hold investments in the stocks mentioned in this report. This report is not intended to be a stock recommendation or investment advice. Investors are advised to conduct their own research and analysis, and consult with a qualified financial advisor before making any investment decisions.