Sure, see POD is a term loosely used here for Ingram but technically its basically Print on Demand. Repro does both Print on Demand /Book on Demand + Short Run Digital ( Which is basically an alternative to offset printing for printing books with short run (Less than 1000 copies usually) instead of going for the costlier Offset Printing Model.

So when it comes to Ingram, yes repro is doing it but POD as a term is used for normal digital printing for books of other publishers also where the competition is immense , where prices are given per page

Could not find the reason to cancel the conall. The Q2 result was nothing great as such but balance sheet has improved considerably. The business profile is definitely making moves towards low capex and low working capital intensive going forward. Even gross margins have improved.

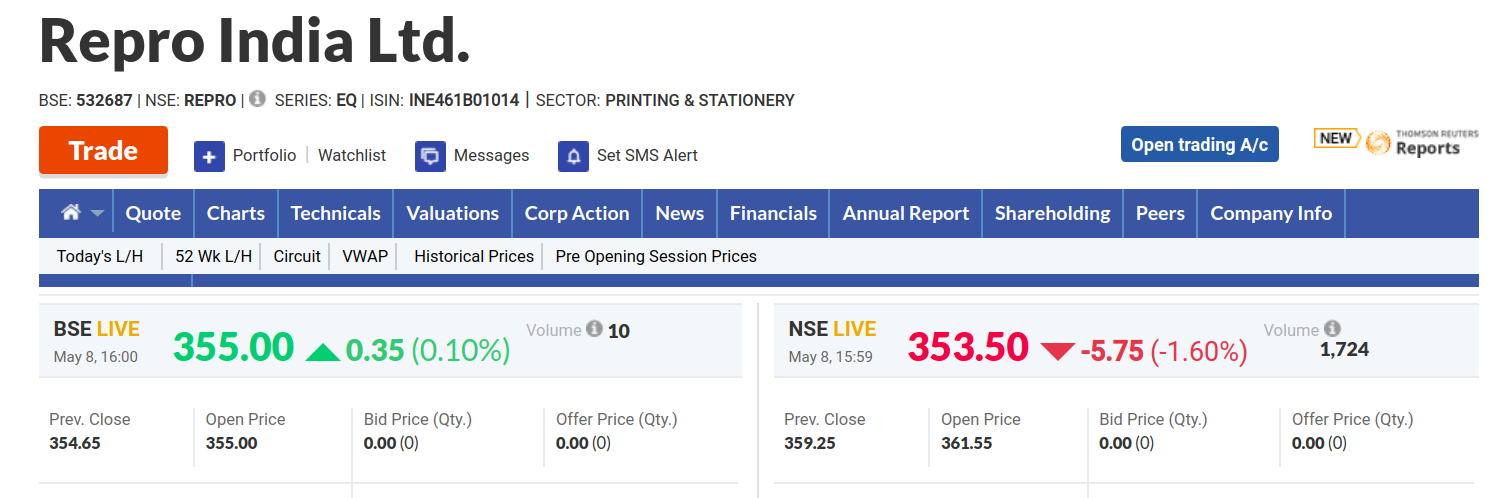

Agree. …balance sheet improved but see the valuations does it justify 800cr mcap.

Its a pure publication company nothing else what ever they talked are all over projected.

Now they have started using word RELEVANT thats fair enough …all ingram titles are IRELEVANT…now they started accepting it…

I personally lost opportunities in other stocks due to repro. Still exited at profit yesterday. The company and the marque investors projections are unreachable in real. Nothing is improving at PAT level

According to kedia,the disruption in the book buying space will be drastic as people will switch from buying books physically to buying one online and hence there will be sudden demand for BOD publishers.He said this in one old interview in 2018 that whenever anyone buys a book,the money goes into the pocket of repro first and then it later pays it’s commission.According to other articles the new units in haryana and karnataka arethe only investment needed and the company does not need to maintain any inventory.

However,your point about Ingram is well taken,if ingram thought it’s ‘8 million titles’ would lead to atleast 100 crore revenue in india,it would cut out the middle man and put BOD units for about a hundred crores.

Need to see if the company can come out of the crisis good because as far as i know,the company is not having much cash in the books.

Its a purely case of creating very positive sentiment and take advantage of it.

Nothing else i can see… …

Now they r shouting about “grat days coming” is only because mr.kedia wants to sell his holding !mark my words and check next shareholding pattern …

I have talked with many industry experts they have told Repro will never fetch any sustainable margin from online selling…

The biggest fraud from repro managment is that " Ingram agreement is not exclusive".

Mr.kedia and Malabar both have judged repro chapter in wrong manner.

Kedia, Malabar holdings remain same q-o-q. Mukul Agrawal decreased, The Ram Fund LP increased.

Jagdish Master name appears in latest shareholding, holding 1,72,209 shares (1.42%)

There are some things that can happen right now in terms of working capital issues.The company may need to close to 50 crore(a rough estimate) for being idle for about 5 weeks ,but the company does not have any cash on the books.This is the time where they would not be selling a single book since amazon and flipkart are not doing any home delivery and it’s traditional biz is sleeping.

The company needs to clear the air with regards to Ingram on whether Ingram broke any agreement by allowing printing rights to others.

Either way nothing will be happening anytime soon,their haryana unit is expected to start

production only in 2021.Anyone can confirm whether their bangalore unit is now up?It was supposed to be finished by Q4 2020 …

Main question is the operating margin?If the company even successfully scales up but the opm is 10 percent,then the stock is already priced in.

Global Distribution through Ingram touches Rs.87 lakhs in 2018-19

E-booksbusiness started with Amazon. Sales in Q4: Rs.2.2 lakhs

Repro Books Sales on Flipkart cross 5% of Sales on Amazon in Q4 2018-19

I wonder what this means.The company apparently sold Rs .2 lakh worth books on amazon.Am I misreading this?The sales on Flipkart are 5 percent of the sales on amazon.Where does the company sell it’s books online if not flipkart or amazon?I was under the impression that most of the POD biz is through flipkart or amazon.Can someone make sense of this.

Global Distribution through Ingram touches Rs.87 lakhs in 2018-19

This means, Repro is making available the Indian publishers’ digital content that they have partnered with so that ingram can inturn do a POD/BOD in the countries they are doing business in. this is a win for Indian domestic publishers, to have their books available and sold in other countries. this is will gain traction as Repro adds/partners more Publishers into their repository.

E-books business started with Amazon. Sales in Q4: Rs.2.2 lakhs

Note, below are my notes from the contents from the conf call

*>> 1. Ebooks beginning: repro was already procuring digital files so they decided to try and start selling E-Books on Amazon & see how it goes. so last two, three months they have begun sales which is around 2 lakhs odd in the last quarter.

Flipkart is taking more interest in building their business in the books category, we are seeing sales improve on that platform and it has grown last quarter we almost more than 5% of our sales came from Flipkart and the balance from Amazon*

Repro Books Sales on Flipkart cross 5% of Sales on Amazon in Q4 2018-19

^ Flipkart is stated to have taken interest again because they had given up on the ebook biz, its a very small market for them India and amazon was already there.

I wonder what this means. The company apparently sold Rs .2 lakh worth books on amazon. > this is the ebooks biz and not the regular physical book BOD/POD or stock books publishing

Am I misreading this? The sales on Flipkart are 5 percent of the sales on amazon. Where does the company sell it’s books online if not Flipkart or amazon? > they started selling in both channels.

Amazon’s ebook sales are the larger share in this 2.2 lakhs worth of sales. Flipkart is just 5% of that pie and the remaining is 95% ebook pie of Amazon.

I was under the impression that most of the POD biz is through Flipkart or amazon. Can someone make sense of this?

Recently in an interview Vijay Kedia said this:

" It is like a snake and ladder game. If you go to sell shares worth Rs. 50,000, the market capitalisation plunges by Rs. 50 crore."

" I have to rethink my strategy for the future. I have decided that going forward, I am not going to invest in small-cap and mid-cap stocks which are illiquid. I want peace of mind"

Opposite is also true. When going in good, illiquid stocks moves higher faster. Since last 2 years, small and midcap stocks has not seen major buying hence such comments. People will be back to such stocks when liquidity starts chasing them. Most of the multibaggers identified in valuepickr forum are illiquid stocks.

But his point is different. He has been holding the stock for last 5-6 years. Now in this crisis situation, if he wants to book partial profit to conserve cash, he cannot do that. Note that, Repro is one of his largest holding…

I have been following Mr Vijay Kedia 2 or 3 years ago each time I bought shares he recommended every time I’ve been cheated it could be his strategy or or a coincidence but I have very bad impression of Mr Vijay Kedia.

For me the intention behind his recommendation of Repro India only to create volume in the counter

Mr. Kedia is definitely not a bad investor. I guess you only follow his public shareholding where his holding is more that 1% in a company. I think a significant amount of his money also parked in mid and large cap stocks but you cannot find him in these companies’ shareholding pattern. Mr. Kedia also admitted that his portfolio has taken a big hit in last 2 or 3 years due to complete bloodshed in micro cap and small cap sector. Please do not follow any investor without your own research and understanding. You do not know what their plan his or you do not have the full information.

Yes, but when stocks correct many people intend to hold them and do not book loss. Hence as much the stock goes down it does not give an opportunity to buyer to book profit. Hence liquidity reduces with correction in price.

This company is supplying books in Kolkata after tying up with various schools.

I thought Repro was trying to get into this business . If Repro have had the infrastructure in place would have gained serious traction once COVID issue came up.

Dis : Previously had a holding but sold out few months back as company not been executing as per my expectations.