decent results, slightly reduced NPA’s, increased disbursements and 2.7rs dividend declared.

2 Likes

Q4FY24 Con-call Notes:

Loan Book and Disbursements

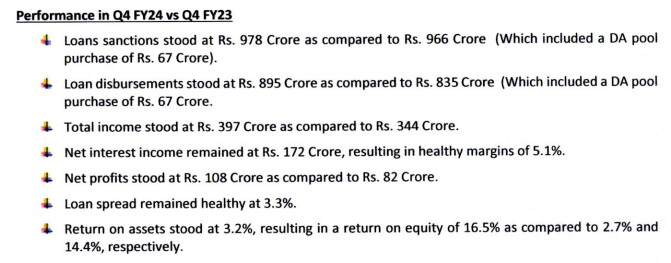

Q4’24 & FY24 performance

• Disbursements

(figures in crores)

o Q4 FY24 = 895 (Q4 FY23 = 835) i.e. 7% growth

o Full FY 24 = 3,135 (Full FY 23= 2,919) i.e. 7% growth

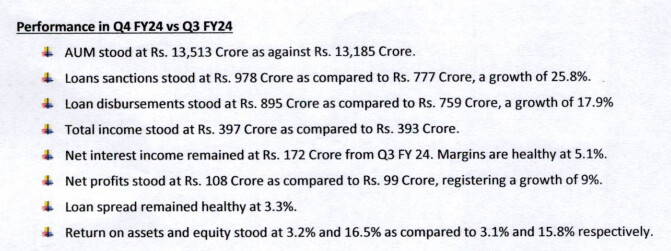

• Loan Book

(figures in crores)

o Q4 FY24 end = 13,513 (Q4 FY23 end = 12,449) i.e. 8.5% growth in FY24 vs FY23

(Note: The management had targeted 14,000 CR loan book by FY24 end, however missed the target. Reasons given were - intense competition in home loan segment & also due to 169 CR of GNPA reduction, which was reduced from the loan book.)

• Segment wise loan book:

| Loan Book (value & growth) | |||

|---|---|---|---|

| As on 31st March 2024 | As on 31st March 2023 | YoY Growth | |

| Home loan (A) | 10,135 CR | 9,835 CR | 3% |

| Non home loan (B) | 3,378 CR | 2,490 CR | 36% |

| Total (A+B) | 12,449 CR | 13,513 CR | 8.50% |

(Note: As can be seen, the non-home loan segment which includes LAP, commercial real estate etc. is growing much faster than home loans. Non-home loans constitute about 25% of the book.)

Guidance on growth in FY25

• Targeting 15,000 CR loan book by FY25 (11-12% growth) net of BTs & GNPAs reduced from loan book.

• 3,600-3,800 CR disbursements targeted.

• Growth drivers – (i) 40 new branches to be added (half in TN, half outside); (ii) Field sales team to grow from 200 to 300 employees; (iii) More focus on home loan & salaried segments with slight compromise in yields.

• In FY25, Q1 might not show much growth as new branches and sales team members added will take some time to get productive.

• FY27 end loan book target is INR 20,000 crores (Non-home loans will be 25-30% of this)

• There was no firm comment on growing loan book through direct assignment route.

Profitability related guidance

PAT

• For full FY24 PAT is 395 CR vs FY23 PAT of 296 CR– jump of 33%.

• PAT guidance for FY25 is 450 to 475 CR. This includes 40-60 CR of projected write backs.

ROA, ROE, Spread & NIM guidance

• FY25 ROA guidance = 3% (vs FY24 ROA = 3% i.e. same range)

• FY25 ROE guidance = 15-16% (vs FY24 ROA = 15.8% i.e. same range)

• FY25 Spread guidance = Around 3% (FY24 spread= 3.4). As company will target higher growth, it might translate to somewhat lower yields.

• FY25 NIM% guidance = 4.8% to 5.2% (FY24 spread= 5.2%). Again might drop due to higher growth targeted.

Cost of borrowing and cost to income

• Since Net NPAs have reduced, they are eligible for NHB funding. Final decision on that after AGM. This might bring down the cost of borrowing from the current avg of 8.3%.

• Cost to income ratio for FY25 is likely to remain in the same range as FY24.

Asset quality related

• The GNPA trend over the last 12 months has been as follows: -

| GNPA% (stage 3) | |||

|---|---|---|---|

| 31-Mar-24 | 31-Dec-23 | 31-Mar-23 | |

| Home Loan | 4% | 4.50% | 5.40% |

| Non-Home Loan | 4.30% | 5.20% | 7.10% |

| Overall | 4.10% | 4.7% | 5.80% |

• Company is targeting overall stage 3 GNPA% of 3% by end FY25. And below 2% by FY27.

• To reduce GNPAs – (i) Company will take steps like auction properties, taking possession etc. for current bad loans; (ii) They are also planning to double to their collection team from 80 to around 150 to reduce further slippages.

• Current stage 2 GNPAs are 11% (of total loan book), company targets to bring it to around 7-9% by FY25 end (Note: Stage 2 GNPAs have always been historically higher for Repco vs some of other HFCs, so it might be something to watch out for)

• As per the mgmt. new loan book (loans given since Jan’22) has a stage 3 GNPA of just 0.24% (Note: Since a big chunk of this is non-home loans, one still needs to be watchful of how it pans out in future)

• Currently, Provision coverage ratio for stage 3 GNPA = 65.2%

• Management is confident of writing back 40-60 crores of these provisions in FY25 (total provisions of 31 Mar 24 are 518 crores).

10 Likes

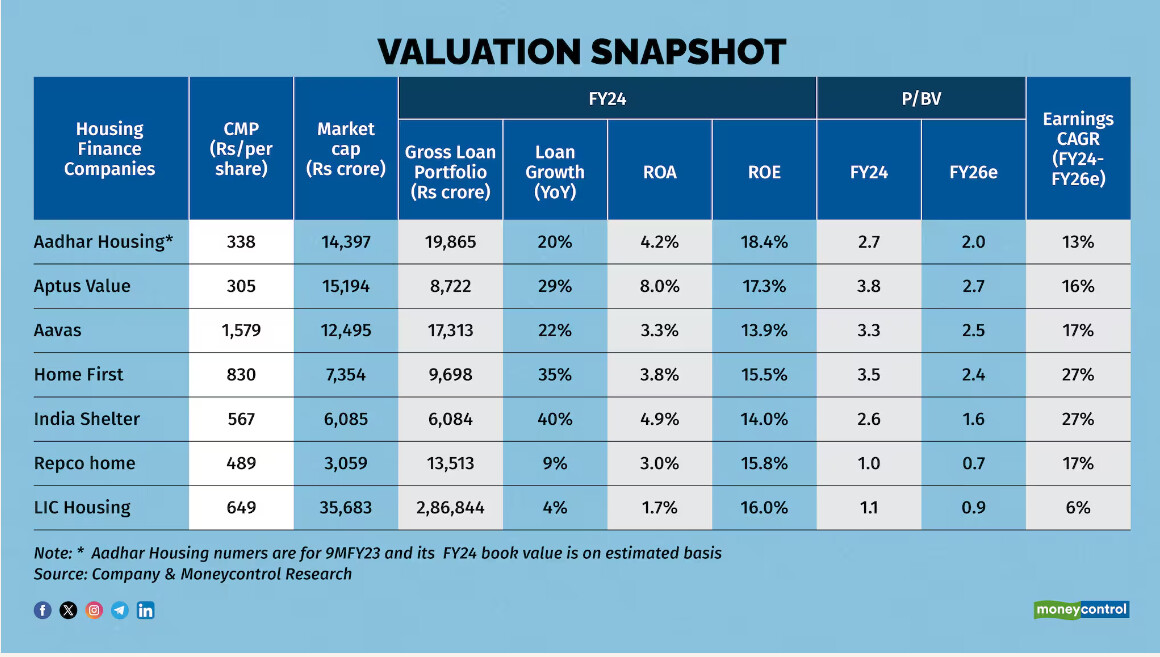

Refer to below mentioned moneycontrol article which points out.

- Repco Home Finance is most undervalue HFC stock.

- Affordable housing finance set for consolidation.

- Shriram Housing finance had a deal with PE investor at valuation of 2.4 times FY24 book value.

D: Invested

8 Likes

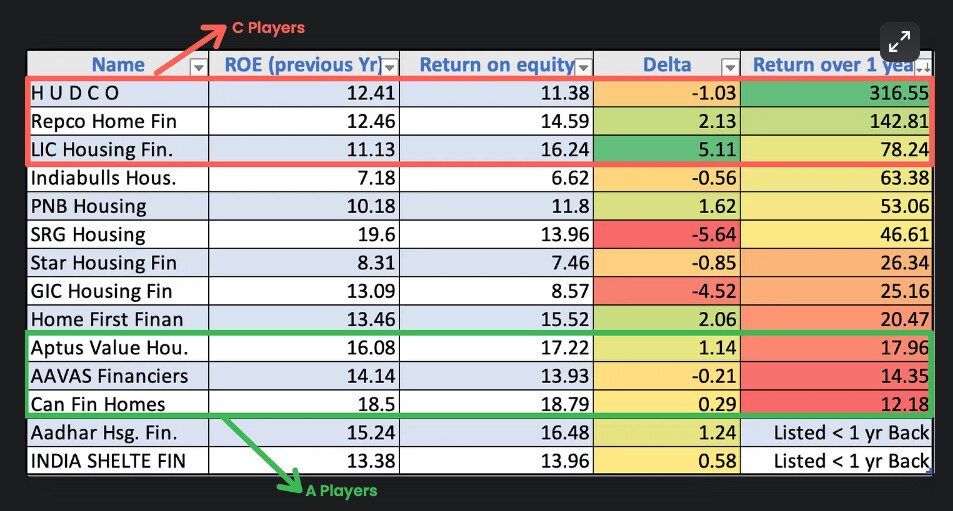

Another article which analyze all HFC by segregating them in different buckets A,B,C.

Though Repco is in Bucket C (poor) Delta in RoE is highest for REPCO and return over 1 year is also higher then other HFC.

Valuation and GNPA reduction is main points to stock return. Interesting read.

D: Invested

6 Likes

This does look like it is trading cheaply at 0.9 * Book value but some of the key monitorables and triggers to track could be:

Growth guidance - They missed the guidance of Rs 14,000-crore loan book by FY24. Management expects AUM to reach Rs 20,000 crore by FY27. So they need atleast a CAGR of 14-15% over the next three years.

Expansion - New branch addition in Tier 2 and 3 towns of Tamil Nadu as planned and also expand its presence in non-core states.

NIMS - NIMs improved to 5.2 percent in FY24 despite the higher cost of funds. Maintain this pricing power

NPAs - Asset quality must continue to improve (especially non-salaried segment). On the right track since FY22 but needs to keep it that way.

Credit Cost - Keep the incremental credit cost low in FY25 to boost earnings

ROA - Maintain atleast its current ROA of 3%

Policy impact - Govt’s rural focus, potential higher allocation under the PMAY-Gramin scheme (Pradhan Mantri Aawas Yojna) and impending rate cuts - will all be positive triggers

4 Likes

Would it be safe to assume that without dilution & with a 15% (post-dividend) RoE, REPCO can double its book value in 5 years. It will also have re-rating from 1 times price to book to at least 1.5-2 times price to book which means there is some chance that the stock price might triple (21.5 = 3) or quadruple (22=4) in 5 years from here?

5 Likes

No one is tracking this actively??? @shubham_sethi would you want to start this thread?

2 Likes

The loanbook growth rate seems to be the main hurdle and most important thing deciding the rerating. NPA will not be an issue. If growth doesn’t happen rerating might not happen.

3 Likes

what is the issue with their loanbook? affordable housing is in a sweet spot. are they not aggressive or something fundamentally wrong with their strategy?

1 Like

On the surface level growth rate seems to be very low… though it has increased recently. Nothing is wrong with the asset quality. I’m studying the company presently.

2 Likes

The company has posted fair results for the previous quarter and seem to guide for a 16K crore book target for this financial year. For this, they need about 1400crore more in the next 3 quarters. They also say they can source more cheaper credit. Has the company been able to stay true to their guidance before? They might be a good company but executing ambitious targets isnt easy

They have missed their loan book targets for most years. One of the reason, market values them low.

But could the past 5 years be due to a very bad old loan book giving them problems? The pre 2022 loan book(40% of book) is the one with high NPAs. There’s new leadership as well now.

1 Like

I exited the position after holding it for over 5 quarters and tracking the progress diligently. I do not see any intention or interest on management side to grow the book aggressively despite asset quality issues improving significantly.

If there is no growth, there would be no re-rating. Additionally, I would have appreciated if the management reinvested in growth of the book instead of paying dividends (this is only my personal opinion).

Lastly, capital is limited, so need to move it into growth opportunities.