Q4 Concall highlights

Collection Efficiency & Bounce rate

68% of customers paid their EMI in June. The collection trend has improved further in July

and most likely 75% of customers are expected to pay. Management believes that the normal

collection rate of 95% can be achieved by October/November if Covid flattens out.

The collection rate is 95%+ for non-moratorium customers (chosen not to opt for June and

in cases where company did not find requirement), which is comparable to pre-Covid era.

Though the first presentation bounce is slightly higher currently (17-20% v/s 15% before

Covid).

Almost all customers who opted/given moratorium in June are the ones who were under

moratorium in the first moratorium period.

Disbursements

Disbursements are now at 50% of pre-Covid level. By end of Q3 FY21, company believes

that it can achieve 80-90% of pre-Covid quantum.

The initial focus of disbursements would be on better CIBIL score clients.

About Rs90bn of the loan book (nearly 80%) is in Tier 2-4 cities. Negligible competition from

banks and other HFCs for fresh disbursements; however, most PSU Banks and some private

banks have been aggressive in loan takeover from Repco.

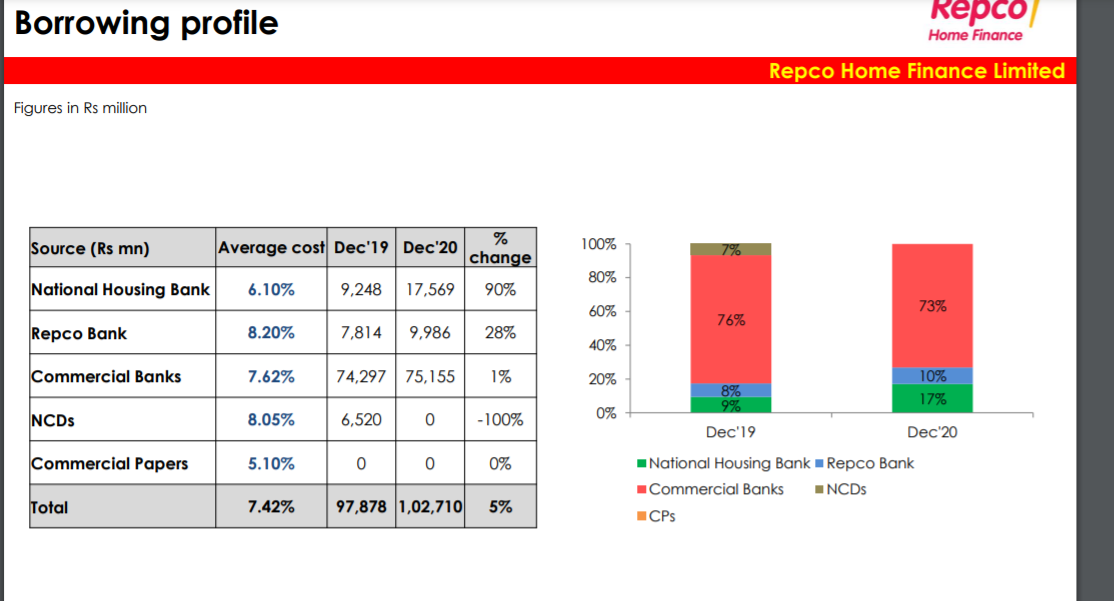

Liquidity position

Even in the second moratorium phase, Repco has not availed moratorium from its lenders.

Company currently has Rs3bn worth of cash/FDs, about Rs20bn of undrawn sanctioned lines and additional sanctions in the pipeline. Liabilities maturing in coming 3 months is about

Rs8bn and coming 6 months is Rs12bn.

Incremental cost of borrowing has been coming down at a fast clip. Incremental funding tie-

up was at around 7% during the April-July period, but it included liquidity from NHB at lower

rate.

Asset quality and additional provisions

The additional covid-related provision of Rs0.4bn made by Repco was based on portfolio

assessment on four parameters viz. a) customers’ area/location in context of Covid incidence, b) borrower’s occupation, c) number of defaults in six months before Covid and d) whether moratorium taken or not taken.

These provisions represented management overlay on the ECL requirement and are thus

additional provisions spread across Stage 1, 2 and 3 customers (majority attributable to

Stage-3). The management intends to make further prudential provision in Q1 FY21.

GNPLs in Home Loans segment stood at 3.8% and in LAP at 6.6%. GNPLs for salaried

customers was at 1.6% and for self-employed borrowers at 6.7%.

Repco expects to reign in GNPL ratio at 4.5% by the end of current fiscal. This expectation

stems from a) improving collection trends (morat % coming down and normal collection

efficiency in non-morat book), b) significant reduction in Stage-2 assets over FY20 and

sustenance at lower level even as of June, c) >90% of loans for self-occupied homes and b)

only 5% of home loans representing booking for under-construction apartments in projects

of small and large builders.

The collection of soft and hard buckets is in-house and only in cases of chronic NPLs (2+ year

older) the company seeks support of recovery agencies.

Majority of the LAP NPLs represent high-ticket (>Rs10mn) legacy loans. Over the past three

years, the average ticket size of the portfolio has been brought down significantly and concentration has been reduced.

In FY22, management believes that GNPLs could come down to 3.5% if the macro scenario

improves.