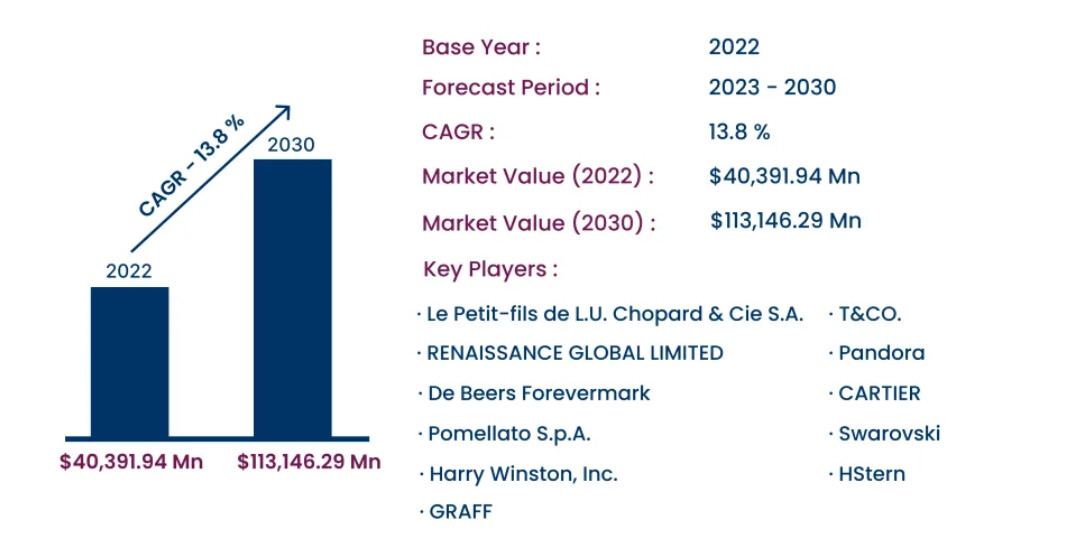

Interesting article from Cognsegic Business intelligence on global online Jewellery market, it’s expected to grow from 40 Billion USD in 2022 to 113 Billion USD in 2030 with CAGR of 13.8%.

The Renaissance is also one the player in the space:

=============================================================

My Observations:

The Company is changing , the management is restructuring the business, they are now focusing more on high-margin D2C segment (direct to customers) and branded jewellery.

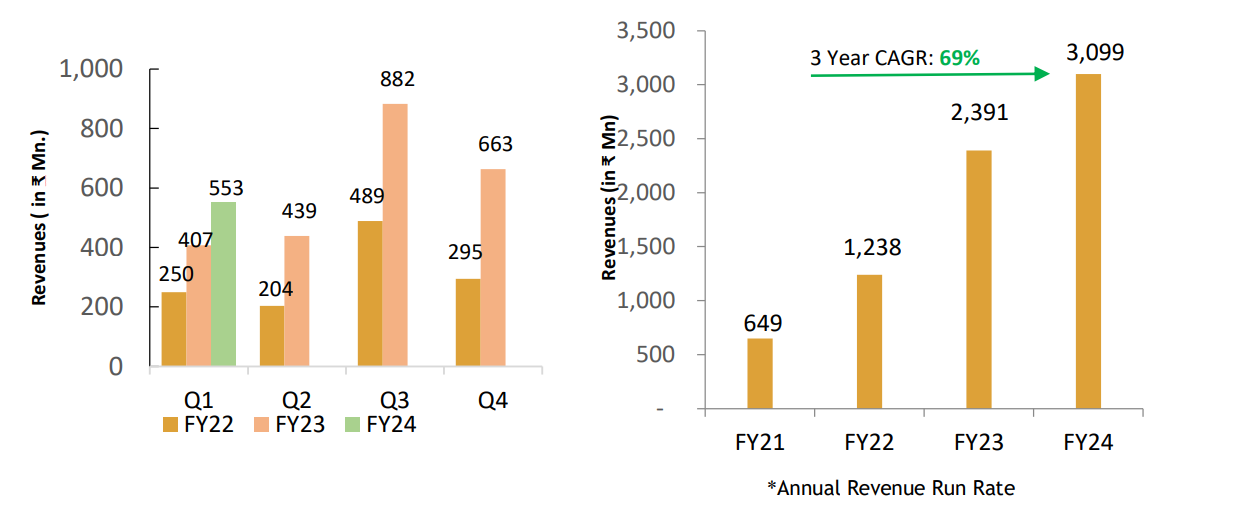

They are able to achieve 92% CAGR over last two years in the D2C segment,

The branded jewellery segment is heling in achieving high D2C growth which will eventually lead to improvement in the OPM.

They are trying to improve the position in global branded jewellery by partnering with Marvel, Disney and NFL (National Football League, USA).

RGL acquired the the rights of Enchanted Disney Fine Jewelry in 2019 and then the company signed agreements with Hallmark, Star Wars and Disney Treasures.

In January 2022, RGL announced a licensing agreement with the US National Football League - NFL. Through this agreement, Renaissance and the NFL will collaborate to design a unique branded jewellery collection using NFL intellectual property.

With the success of licensed jewellery on their online portals, RGL is poised to become a leader in the Direct-to-Consumer (D2C) business.

The D2C growth in the recent past:

By tying-up with global brands like Disney, NFL, Netflix they are trying to attract the younger generation of the consumer. for example, the management said, ‘villain jewellery’ contributes about 40% of sales, these designs are inspired by inspired by drama, magic, and mystery of Disney’s most glamorous villains. Consumers seek products that connect with them on an emotional as well as aesthetic level. For instance, the black rose in the Maleficent Disney Villain ring that we have crafted, symbolises rebirth and new beginnings. There is a strong preference for established brands because of the trust factor.

During the pandemic time to reachout to customers, the company has launched five D2C websites for in the international markets: Enchanted Disney Fine Jewelry (www.enchantedfinejewelry.com); Star Wars Fine Jewelry (www.starwarsfinejewelry.com); Hallmark Fine Jewelry (www.hallmarkfinejewelry.com); Made For You (www.diamondsmadeforyou.com); and Jewelili (www.jewelili.com).

For the period April to December 2021, the D2C business more than doubled (+123%) to ₹ 94.3 crore compared to ₹ 42.3 crore a year earlier.

Company also says they are getting more demand on customised jewellery segment. The customers can create their own digital designs using the options and tools available through the company’s website. This also lead to reduced working capital and reduced inventory as it’s made on the order basis.

IRASVA:

This brand is launched in India, it’s online and store, provides omni-channel experince service. The stores are opened in Mumbai and hydrabad.

Over the 25 years the company has transformed from pure B2B player to integrated branded jewellery player with licenses from iconic global brands along with online and physical store

Some of threats:

-

Higher inflation rate, reduced consumer demand in developed market where the company has major presence (though company says it affects only certain segment in the business - high affluent class section may not affected)

-

Risk of concentration on single market USA.

-

B2B vertical depends on the strategies of the partners/B2B customers.

-

Capital intensive business.

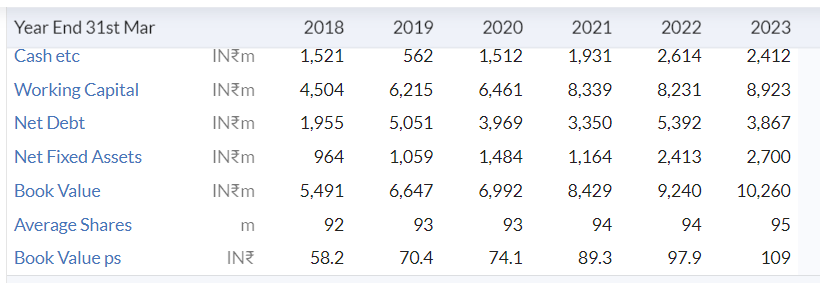

Financial Summery:

Balance Sheet:

Valuation:

Valuation looks good: trading at P/E of 10.8

P/B of 0.93

disclosure:

Not Invested, started tracking.