This unit has been hived off from Reliance Capital during monsoon of 2017. came up with good set of numbers yesterday. Its half yearly EPS is 3.61 with management guiding for even faster growth in coming times. Going just by the run rate for EPS, @86, the stock is available at PE of 12. Given the huge run up in the housing finance companies in last 1-2 yrs, does Reliance Home Finance sound to be cheaper bet at current level of Rs. 86.

Reviving this thread which was locked as the initial post didn’t have due details and disclosures. Request everyone to take care while initiating new threads.

Reliance Home Finance is part of the Anil Ambani group, focused on home finance and related space. This company had got de-merged from Reliance Capital in mid November 2017 and had listed at about Rs 100.

The company has been late to target this area but they seem to be very aggressive with ambition to reach 50,000 AUM in next few years.

Interestingly their GNPAs have been coming down gradually.

Though the valuations look attractive given the growth prospects but there are several risks too:

Their loan book has a lot of LAP (20%) and commercial finance book (28%). And these have been big ticket loans. If there are problems then due to the leverage things can become really bad in a short period.

I think credit rating report had also highlighted the same

Too much of competition in this space. And their book is not seasoned so one doesn’t know the real problems and NPA.

Lets try to research more on it.

Regards,

Ayush

Disc: Invested. Small exposure to understand.

I wouldn’t say it is undervalued unless the comparison is only with its own 6-mths price performance or the technicals showing it has rebounded from low 60s a couple of times even though forming lower highs from such rebounds. I wouldn’t prefer to base my valuations on such aspects. Though one thing is clear that it listed on 22-Sep-17 and has been going down since.

It seems to be valued at similar valuations as that of Dewan Housing at around 1.6-1.7 PB although expensive in PE terms at around 18 pe assuming they close 2018 with 175cr.

The other thing which strikes me in such businesses like loans is that the management reputation plays the most important role and if the management isn’t perceived as good then valuations can stay low for long periods like Dewan, etc.

During times like these with industry tailwinds such businesses would want to restructure their businesses and create an impression of a re-energised operation but we should be vary of such impressions.

It is in management’s interest to offer a lead to investors like a huge target…in this case growing AUM by three times in 2-yrs. Even though anyone would regard such a target as outrageous if not idiotic, we as investors can get into a tendency to hang on it and also discount it to justify our valuations.

Also valuing this co on PB may not be right as they have recently raised equity so it will appear undervalued.

Just bcoz the size of the company looks small doesn’t mean it will also grow with industry tailwinds as the likelyhood of higher NPAs is highest in this segment like subprime, MFIs, etc. In this business, you can’t have the best customers paying higher rates so you have to compromise on quality.

Given relatively low valuations, high targets, good numbers but very bad promoter reputation, I can at best, consider taking a bet of 1% of my pf knowing I might be falling for some or all of the above biases

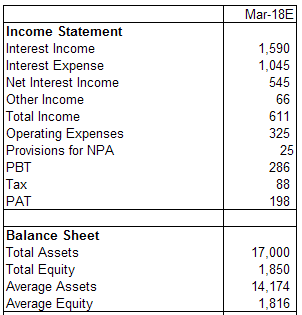

Here is my quick back of the envelope calculations for estimated March 18 numbers using the numbers for last 3 quarters.

Source: Capitaline

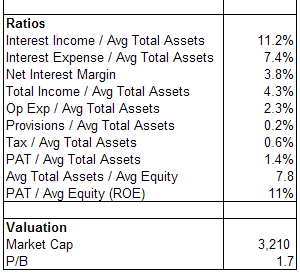

Ratio Analysis

Interest Income to total assets of 11.2% is in line with others and also in-line with composition of the portfolio.

Interest Expense to total assets of 7.4% is somewhat high for a housing finance company but given the troubles of ADAG group, this is not bad. Also RHFL NCDs are yielding 9% relatively higher than others.

Net Interest Margin of 3.8% is decent for a company of this size.

It also earns a small other income so total income to total assets works out to be 4.3% which is good.

Operating expenses are at 2.3% of total assets. This is on the higher side. For HFC this ratio should be less than one. Others (IBHFL 0.4%, LICHFL 0.4%, Dewan 1.1%, Canfin 0.8%, Repco 0.8%, Gruh 0.8%) are much lower. Even HFCs with affordable porofilio have lower opex. Not sure why it is incurring such higher operating expenses. Need to dig out further. It may be paying commission to agents to grow aggressively. This ratio is also not showing any improvement over last 3-4 years so it is not getting any benefits of economics of scale.

Credit costs at 0.2% is much lower than others. This will go up as portfolio ages. this will further dent ROA.

Tax is at normal rate.

Return on Assets is at 1.4% which is lower than average for HFCs. This should higher than 2% and preferably higher than 2.5% for a company with somewhat risky portfolio. Higher opex is causing lower ROA.

Leverage is at 7.8 which is somewhat lower than other HFCs but given the nature of the portfolio, I don’t think company will increase the leverage.

All this translate to a ROE of only 11% which is much lower than others even lower than Dewan. I also don’t see how this can improve.

Given its fundamentals a Price to Book value of 1.7 appears fair or even high.

I have this stock in my portfolio along with Reliance Capital. Few of my comments:

At CMP, the stock is trading quite cheap on PB multiple and PE multiple is slightly inflated due to higher operating costs compared to other HFCs, which if comes in line with peers, should lead to higher profit growth in the future and normalization of PE ratio

They are planning to double their outreach locations in the current year along with 3 affordable housing centers which should help them grow aggressively

The management was a little cagey in the previous conference call when asked about growth prospects and the next 2 quarter numbers will give us indication where growth is headed. This is a key monitorable along with GNPA ratio going ahead

Even if we assume a lower growth rate of 20-25% for the company as against management’s guidance of 100%+ kind of growth rates, the stock is still reasonable; and if they actually manage to achieve higher growth rates, it could be icing on the cake

Reliance capital still owns around 50% of the company and could help the company with growth equity in the future if they have difficulty raising funds from the market due to adverse market conditions. RNAM generates a lot of cash and can help fund RHFL and other Reliance capital subsidiaries

The company is still not fully leveraged which will help EPS growth without dilution in the next couple of years

Some qualitative information regarding the quality of their customers and ease of getting loans/ underwriting could help clarify how the future NPA picture will look like which is critical

They seem to be following a high NIM, higher commercial book strategy similar to Indiabulls housing which would lead to higher profitability and return rations similar to Indiabulls provided they can keep their asset quality in check.

Ayush, I had a quick question regarding EPS growth - although PNB housing and RHFL are growing very aggressively, PNB housing is diluting capital at about 3 times book on pre-dilution basis, which means even though its growth rate may be lower that RHFL, its EPS growth will be higher which is eventually what counts for share price appreciation. I am slightly confused on this issue and would really appreciate some insight from your end. Thanks

One of the main problem with is stock is that it belongs to the part of ADAG group. The whole group stocks drags down with bad news so I doubt that growth in the numbers of RHFL will reflect ever in RHFL stock price as problem of Reliance communication is not going to solve in near future.

I do not see any connection of RCom and RHFL from the financial point of view (they have not given any loans to them). If you have anything concrete to point at apart from the same promoter group then let us know.

My point is that one bad news and the whole ADAG pack comes under pressure and in the past few months NEWS regarding RCom is extremely bad and it is also dragging stocks like Reliance capital down which fundamentaly quite ok Company. I am not saying that RHFL has given loan to RCOM

If RHFL trades at 1.5 times book value, it will need to issue more shares than PNB housing (3.5 times book value) for further growth capital from investors to maintain its capital adequacy (equity) and hence EPS growth will be lower since number of shares will be very high but I need more clarity on this point myself on how this dynamic works.

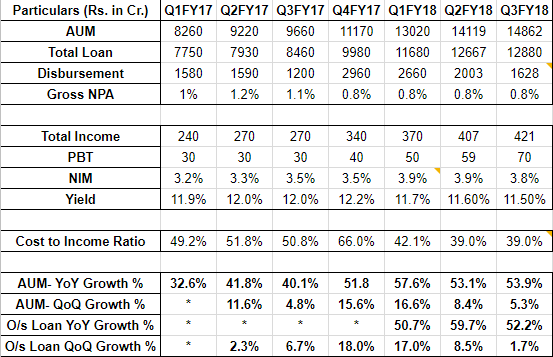

Yes, very strong results indeed. A quarterly profit of Rs 57Cr implies annualized PE of 14. A stock growing sales And profit at 50% available at 14PE is a steal. GNPA is in check at 0.8% and trump card here will be cost to sales reduced to 38% from 55% which could easily further reduce to less than 20%.

While the loan book is not seasoned, I believe at this price, all risks are priced in.

YOY quarterly growth in revenue is only 20% which is well below guided range. GNPA ratio being stable is good and profitability growth is impressive. Difficult to fathom why the growth is down for the company when they have aggressively expanded their outreach locations. Valuation front still looks cheap to reasonable.

Revenue from operations grew by 33% and other income got reduced. I do not know what other income is, but I guess revenue from operations is what matters.

Prior to the company’s listing in Sep 2017, Reliance Home Finance was 100% owned by Reliance Capital. Was anybody able to figure out how much Reliance Capital got paid for listing Reliance Home Finance?

In 2016 RHFL had 6.58 Cr shares

In March 2017 they had 11.58 Cr shares

Some questions I was thinking about…

Why was the increase of 5 Cr shares necessary? These were issued to the promoter at 40 bucks a share, so that works out to 200 Crs.

What did the capital structure look like after the IPO?

How many shares did the promoter sell during the IPO?

How much did they get paid for it?

Why did they list it in Sep 2017? Why not sooner or later? Maybe high market levels were a reason for this.

I have tried looking up multiple docs including the IPO document, quarterly results for Reliance Capital, RHFL 2017 AR, etc but not much success in figuring the puzzle out. Moreover Reliance Capital’s shareholding is a maze. So getting to the bottom of it is quite complex.

Reliance Capital’s 2018 AR should be out in a couple of months and that might give some visibility. In the meanwhile, is there any other way of figuring this out?

so you have to compromise on quality.

so you have to compromise on quality.