Refex Industries

1) Business Snapshot & Strategy

What does Refex do?

Refex Industries has transformed itself from a refrigerant-gas company into a highly diversified clean-infra business across four key verticals: ash & coal handling, green mobility (EV), power trading, and renewable energy (wind + solar).

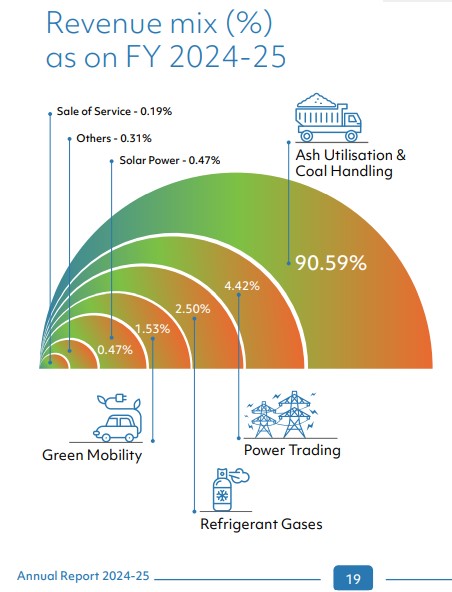

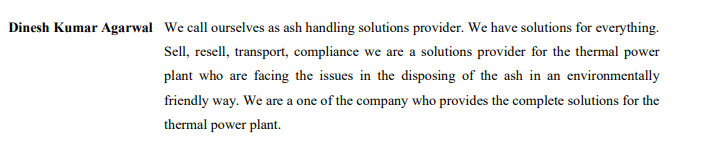

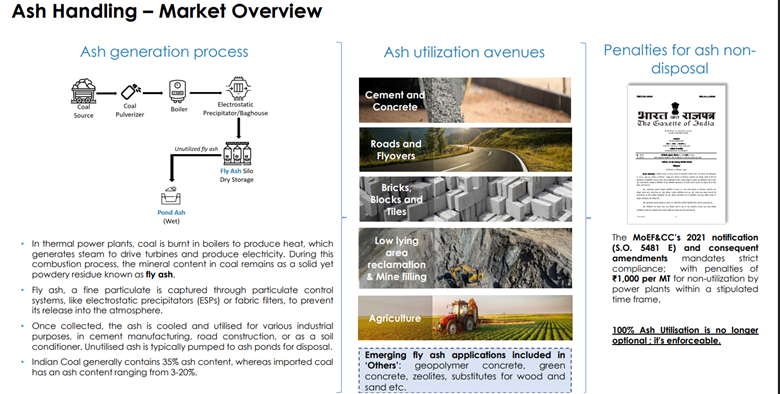

Ash & Coal Handling: The only organized player in the country and this is Refex’s scale engine. Ash & Coal Handling vertical is no longer just a high-capacity logistics business—it has evolved into a technology-driven, centrally coordinated operations platform.

The company manages end-to-end activities for thermal power plants, Cement factories including fly-ash evacuation, bottom-ash handling, coal yard management, and long-haul transportation. What differentiates Refex from traditional contractors is its deep digital integration across the entire logistics chain, enabling superior control, lower leakage, and higher asset productivity. Like Centralized Command Centre , Digital Work-Order System , Digital Fuel Management System, Live GPS Tracking, Operational Analytics Dashboard etc..With these digital layers, Refex is able to run a traditionally manpower-heavy business with industrial precision, reduced leakages, and high performance discipline

Transcript from Nov 2025–

About the market share and TAM(Transcript from April 2025)

Refrigerant Gas: The first Love of Refex Industries. Since inception, they have been dedicated to refilling refrigerant gases that serve as replacements for harmful chlorofluorocarbons, or CFCs, and hydrochlorofluorocarbons, or HCFCs. they have emerged as a leading supplier of environment-friendly hydrofluorocarbons or HFC refrigerant gases in India. These refrigerant gases are crucial in various applications, including refrigeration, air conditioning in residential, commercial and automobile sectors, flume blowing agents and aerosol propellants. They pioneered the introduction of refrigerants in a disposable can directly accessible to end-users branded as Refex cans. But as this is more like low margin commodity like business management considering to liquidate this business in near sort term or we can say already in process of liquidation as per the latest update from Q2 concall would like to aggressively focus on the opportunity in Coal and Ass handling segment

Green Mobility: Demerger On Radar

Refex Green Mobility Ltd has unveiled a major expansion plan with the launch of 100 new cars in Delhi, marking another milestone in its journey from 24 cars to 1,400. Now set to become an independent listed entity after merging with its parent group, the company is eyeing 10x fleet growth to 14,000 cars in the next five years. With a strong focus on the B2B and B2B2C corporate mobility segment, Refex sees a large addressable market in enterprise car rentals. Alongside its expansion, the company has launched a new app and dashboard for enterprise customers to ensure seamless, safe, and sustainable corporate mobility. Future growth could also include CNG and hybrid options, as Refex pushes for a cleaner and more efficient mobility ecosystem.

Power Trading: A closed chapter from upcoming quarter. They hold a CERC Category-I license, enabling large-scale interstate power trading. But due to very low margin business they had taken a conscious call to wind down the power trading operations, focusing instead on core business with higher strategic and financial alignment.

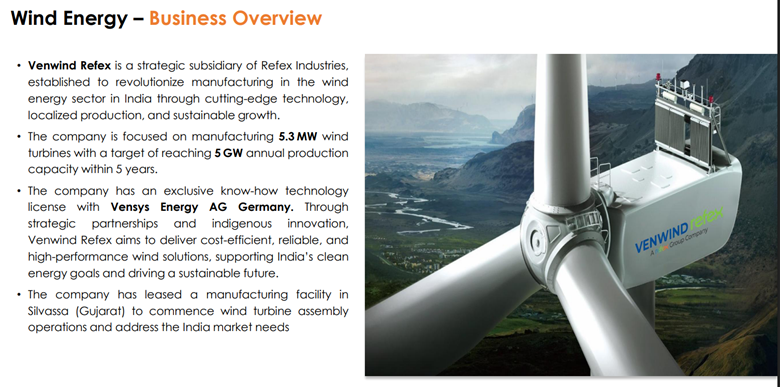

Wind Energy

Strategic Edge

A conglomerate built on sustainability: Rather than being a pure-play coal or EV company, Refex straddles the old and new economies.

In-house logistics: They’ve shifted from outsourcing haulage to operating their own ash-transport fleet. This reduces cost, gives control, and improves profitability.

First-mover in ash utilization: Not many organized players in India handle fly-ash at scale, and Refex has built strong relationships across thermal power plants.

Wind manufacturing ambition: The JV with Venwind could be transformative if they scale.

Strong ESG narrative: Ash-handling reduces environmental externalities from thermal plants.

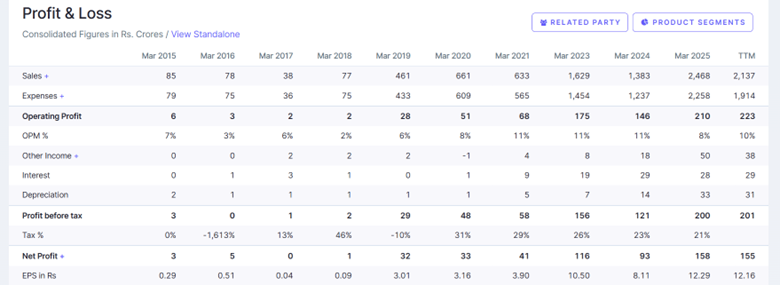

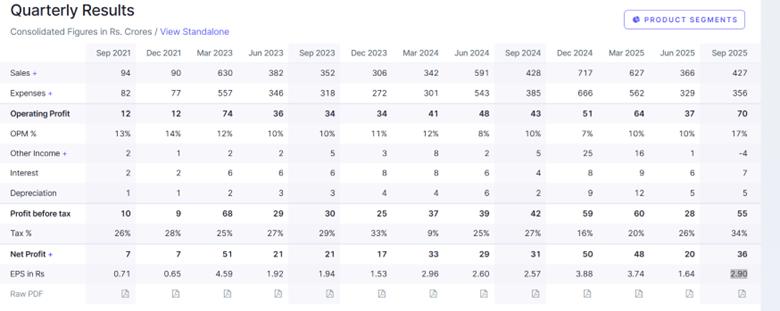

2) Financial Performance & Momentum

32x topline and 150x bottom line in 7 years and still growing in a higher peace

Recent Performance (FY26 / Q1,Q2)

Due to the early and intense monsoon-led disruptions in Q1 and the continued heavy rainfall in Q2

largely anticipated as part of the normal seasonal cycle—coal and ash-handling operations were temporarily impacted across several project sites. However, with monsoons now receding, activity levels are recovering steadily across locations, and the company expects normalized operations and stronger throughput from Q3 onward, supported by continued cost discipline and operational efficiency measures. Even now management are confident that they will able to archive the proposed guidance as the fleets count are going to increase from Q3 onwards

3) Growth Drivers / Investment Catalysts

- Ash Handling Expansion

- As regulatory pressure increases on thermal plants to handle and repurpose fly-ash, Refex is well positioned to win more contracts.

- Vertical integration (owning transport) gives cost advantage.

- Wind Turbine Manufacturing

- Through Venwind-Refex, they are localizing 5.3 MW wind turbines (licensed tech from Vensys).

- Recuring earnings for maintenance activities

- This could unlock high-margin engineering + manufacturing business over time.

- EV Mobility Scale-Up

- Their green mobility business is scaling fast:the fleet has grown significantly 24 to 1400

- A planned demerger on First qrt of FY27

4) Key Risks & Red Flags

However, it’s not all smooth sailing. Here are the main risk factors to watch out for:

- As they scale, debtor days could balloon. In their Q4 FY25 earnings call, management mentioned increased receivables (contract assets) hurting cash flow.

- Running a large haulage + EV fleet requires CAPEX, maintenance, and utilization discipline.

- Manufacturing wind turbines is a capital-intensive business with supply chain, project execution, and procurement risk.

- While ash handling is the cash cow, other verticals may suffer margin pressure if not scaled properly.

- Rapid growth + capex + working capital needs may stress liquidity; if cash flows don’t scale up, debt may become burdensome.

- High Promoter pledge need to watch carefully

- Heavy dependency on NTPC and govt psu contacts

- execution clarity on Refex Mobility (RML) listing, and its business metrics.

5) Valuation & Return Potential

- Recent Growth Justifies Premium: This is already a multibagger and still have potential to grow as a compounder if they are able to sustain the growth momentum If they execute on all fronts, Refex could be revalued as a clean-infra conglomerate rather than a small industrial company. But poor execution could lead to stretched cash flows and return compression.

- Embedded Optionality: The value of the wind JV (Venwind Refex), EV business (post-demerger).

My view: While most of the green-energy narrative today centers on solar, wind, and green hydrogen, it’s critical to recognize that coal remains deeply embedded in India’s energy and industrial landscape. Despite the clean-energy buzz, a significant portion of electricity continues to be generated from thermal power—Refex itself notes that coal-fired power plants still account for over 70% of India’s electricity generation.. That means ash generation also remains structurally high, creating a large, persistent addressable market for ash handling. Refex describes itself as the largest organized player in India’s ash-management space, already operating across 40+ power plants and handling up to ~70,000 tonnes of ash daily. If Refex can continue to outpace unorganized players, convert more ash-handling contracts to its organized platform, and leverage its digital and operational advantages, it has multi-fold growth potential — not just in volume, but in margins and long-duration, high-quality contracts. I like Dynamic and opportunity-driven mindset of the promoter, who has consistently demonstrated an ability to identify high-potential business segments, scale them rapidly, and exit or de-prioritise lower-margin, low-growth verticals with discipline. This sharp capital-allocation approach—combined with the promoter’s continued increase in shareholding—reinforces confidence in the long-term strategic vision and alignment.

Disclaimer: Invested and have recent transactions. I am a novice who is studying this sector and am bound to have made lot of erratic assumptions. Please do your own research.