RBL Bank is one of India’s fastest growing private sector banks with an expanding presence across the country. The Bank offers specialised services under six business verticals, namely: Corporate & Institutional Banking (CIB), Commercial Banking (CB), Branch & Business Banking, Retail Assets, Development Banking and Financial Inclusion (DB&FI) and Treasury & Financial Markets Operations. It currently services over 65 Lakh customers through a network of 324 bank branches and 993 business correspondent outlets spread across 28 Indian States and Union Territories.

Despite the challenging landscape, we remained undeterred on our path, delivering strong financial performance and solid growth. Being an agile and committed Bank, we have consistently evolved to serve our customers better through the rapidly changing business ecosystem.

FY 2018 – 19: A CHALLENGING YEAR FOR THE INDIAN BANKING AND FINANCIAL SERVICES SECTOR The Banking sector witnessed a tough year with many banks challenged by deterioration in asset quality, stricter provisions as well as governance issues. Both the Government as well as the RBI continued to make efforts to improve the health of the sector: RBI, through prescriptions on liquidity and regulatory interventions, while the government, through capital infusion in public sector banks.

The year, however, was also marked by turnaround in some underlying trends for the industry. After growing in single digits for the past three consecutive years, bank credit growth reverted to double digits. Lending to industry picked up after remaining muted for the past five years. Asset quality on banks’ books has now started to show improvement.

Our advances grew 35% over FY 2017-18 to ` 54,308 crore. Strong growth across all business segments fuelled this performance. Within advances our wholesale advances grew 25% while our non-wholesale advances grew 49%

Our asset quality remained on solid turf this year and the key ratios witnessed improvement over the preceding year. Our net NPA, for instance, stood at 0.69% in FY 2018-19 versus 0.78% in FY 2017-18.

In order to keep a good eye on the road ahead, a rear view is important too. The financial year gone by marks the ninth year of an extraordinary journey for RBL Bank which started in late 2010 under a new management team. I am proud and honoured to have led this transformation through which we have managed to create a vibrant and competitive institution of scale and substance.

Over the last nine years, the bank has consistently delivered on almost every key business and financial parameter by growing approx. 40 times in size and over 50 times in profit. Our customer base has grown from about 1.5 Lakh customers in FY 2010 to over 65 Lakh customers by FY 2019 and we are now present across 28 Indian states and union territories through a network of 324 branches & 993 Business Correspondent Outlets.

Our Corporate Banking Business has now started yielding rich dividends. We have spent the last nine years building scale (including capital strength) and enhancing our capabilities in terms of acquiring & deepening client relationship and expanded our range of products and services. Our strategy of attracting talent specialising in this domain and of making requisite investments in technology, risk and governance has helped in building a prominent competitive position in the industry and emerge as a ‘go-to bank’ for a wide array of corporate banking & transaction banking solutions.

With the addition of 59 branches during the year (taking the total of number branches to 324), we have accelerated the pace of our physical network expansion.

Our employee strength has grown almost 8 times over the last 9 years and CREATING they continue to remain the driving force behind our growth.

We have a robust risk governance framework that encompasses good underwriting standards, internal controls, monitoring systems and independent audit function. Efficiency of the framework is overseen by numerous internal committees and by the Board. This framework is supported by comprehensive risk policies that are reviewed periodically.

Over the last one year, our credit card customer base has more than doubled, taking the total count of our cards customers to over 17 Lakh.

We acquired the credit cards portfolio of Royal Bank of Scotland back in 2014. From then until today, the business has seen its fair share of success, always emerging to only do better than before. Our business is the fifth largest in the country in terms of retail spends per account and is adding new customers every month.

In the last year, we added scale to our financial inclusion business by ramping up stake in our microfinance subsidiary, RBL Finserve to 100%.

Although India continued to be one of the world’s fastest growing major economies in FY2018-19, domestic economic activities remained sluggish in the second half of the year. Just when the economy began recovering from the twin impacts of demonetisation and Goods and Services Tax (GST) related transition, the crisis related to the performance of Non-Banking Financial Companies (NBFC) cast its shadow on consumption demand and market sentiments, putting economic growth off track.

There are ample signs that asset quality concerns for the banking sector are peaking. As we entered 2019, NPA formation has slowed significantly across sectors and recoveries from recent NPAs are streaming in. Lower incremental slippages to NPAs and drop in special mention accounts reflect significant reduction in the quantum of potential stressed assets.

As the economy recovers and the capex cycle begins to move upwards, corporate lending will pick up as well, particularly for infrastructure, commodities and consumption companies.

In July 2018, the division issued its 1 Millionth credit card. The card count currently stands at 1.7 Million for the entire cards portfolio, with over 1.1 Million cards sourced in FY 2018-19 alone.

The Bajaj Finserv RBL Bank Cards became the first co-branded Credit Cards in the Indian market to cross the 1 Million milestone, with 8,00,000+ cards sourced in FY 2018-19.

As the industry continues to go digital, there has been a significant behavioural change in the retail banking experience. The Bank is making greater use of technology to further reduce account opening time. Digital acquisition now accounts for 45% of all the sourcing for RBL Bank proprietary credit cards, leading to a 26% reduction in acquisition cost.

The comment in the annual report is with respect to credit growth of overall banking industry as a while where after multiple years of lull n NPA issues, now things seen to be bottoming out in terms of NPAs n credit growth shows early signs of revival from single digit to double digit. You will usually get the consolidated data on RBIs site in case want to get in banking sector credit data details

Details around “other expenditure” under “operating expenses” that is almost 50% of overall operating expenses is not known. What could this be?

The bank seems to offer services around trading in derivatives while significant portion of its own assets/liabilities is hedged through derivative contracts.Is there a bifurcation of income earned through this service or is it all clubbed under other income?

Have generally seen foreign banks having significant exposure to derivatives especially investment banks such as Deutsche bank. Is this something picking up now in the Indian banking industry?

Any insights/pointers around these would be helpful. Thanks

Investment Case Summary:

Low market share for assets and liabilities: 0.6% market share in credit and less than 0.5% share in deposits. Low market share on credit means that it is well placed for a 30% loan CAGR over next 3 years.

Credit Business growing strongly and now clocking RoA above the blended average - Despite being a late entrant has been able to build a base of 1.7mn card. Bank targeting to double its base in next 18 months. RoA in this business at that scale could reach 3.5+%. Card growth continues to be one of the highest in the industry primarily due to BAF partnership and its strong distribution advantage. A risk here is how that RBL is not an exclusive partner for BAF and BAF is looking for an additional partner. Even if this risk materializes growth should be high as RBL targets top 25% of BAF sizeable customer base.

CASA ratio has gained from 22% in FY17 end to 25% now. Bank remains very confident of 70-100bps improvement in CASA ratio per year. In comparison many other banks have CASA ratio in excess of 40%. So even though there is high competition of CASA, RBL should be able to grow its CASA due to low base, expanding branch base and higher branding efforts. Its payments initiative should allow it to capture CASA from merchant acquisition.

Cost to Income ratio can come down in next 2-3 years. C-I ratio at 51.3% is quite high as bank has been in investment phase and many of its branches are new and not profitable yet. Bank has indicated that ratio would remain at 50-52% for next few quarters as well but this could start coming down from FY21 as many of the branches will start breaking even and there should be moderation in branch expansion.

Good asset quality to sustain - Asset quality has held up well so far and especially when many of the other banks have been involved in contentious exposure to some of the corporates in FY19 and FY20E. Recently the stock price came off from ~INR700 to INR610 on some concerns related to potential exposure to Mcleod Russel as the liquidity position of that business (and group companies) has significantly deteriorated. My understanding is that its highest corporate exposure to a group is around INR500cr which is one of the top group. Working with a 3 digit exposure INR100-200cr, this exposure is less than 0.3% of FY19 loan book. Portfolio held up well despite a shock to micro finance portfolio during demonetization. Within corporate lending, focus is more on working capital loans. RBL can continue with low credit losses for some time. I think it is fair to work with slippages close to 1.8%.

Core fee income growth higher than advances growth with rising share of retail adn higher fee contribution from credit card business.

Management - one of the most comforting thing for me. It seems that management understands its weakness and challenges and has been able to find a way to work around those. Its strategy to rely on partnership models when RBL brand is on weaker footing is a case in point. Bank has been able to get attract high quality capital (investment from CDC Group, HDFC Life, Steadview, Multiples PE in earlier rounds) and a well respected board has been able to balance interest of stakeholders.

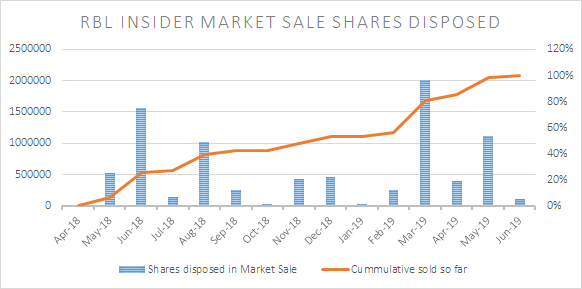

What is bothering me: Noticing some insider selling for past several weeks. Not sure about what could be the reasons behind this. Would be grateful for any thoughts here.

I observed this as a screener alert and decided to look into it a few days ago. Aside I manually checked names of people (insiders) selling and looked them up on linkedin, most mid to senior managers. I don’t think this should be a red flag from a trend point of view. Given below.

Any other opinions from boarders welcome.

On the other side I had checked market disposal numbers for YES bank last calendar year end and could conclude on the trend differences.

Thanks @varun86arora for detailed analysis. One observation is that RBL’s financing profit is consistently negative over the last 8 quarters (based on screener.in data). Is that something to be worried about?

Thanks, Deepak. The chart is helpful. I had picked up that Vincent Valladares, Head – Commercial Banking and Ramnath Krishnan, Chief Risk Officer were selling sometime back but held on to investment because the selling has not been coming from people further up in the hierarchy and also because of some other positives mentioned in my previous post.

@newrb - I believe by financing profit (not a term that I commonly use), you are refering to PAT ex the impact of other income. If that is the case, yes you are right but I dont think this is something to be worried about (in fact this is where the opportunity lies). Keep in mind that RBL is still in early phase of expansion and has been expanding branches at a rapid phase and putting investments on technology. Many of these branches are not profitable (reason why cost to income is high) and will only become profitable from FY21 onwards. Also I will exclude other income only if it has a big component of trading. In case of RBL, that is not the case and core fee income is the main driver of other income. Credit card business which is one of the key business for RBL has been driving core fee. So I wont be worried because of this. Hope this helps.

“The funding will enable greater financial inclusion in these states which are the poorest states in the country with significantly low penetration of financial services. In addition, by supporting climate smart financing, the project will encourage sustainability," IFC said.

One point which @rupeshtatiya had raised on Other Operating Expenditure (schedule 16 of all bank reports). If anyone has got a reply from the bank or knows please could you share. Would want to know where this is originating from.

Other banks make some form of notes for this line item but not able to figure out for RBL.

HDFC: Includes professional fees, commission to sales agents, card and merchant acquiring expenses and system management fees.

KMBL: Total Exposure to top four NPA accounts: 638.15 Crs.

ICICI: Net of recoveries from group companies towards shared services.

From FY18 to FY19 other op expense has seen a comparative rise too ~500bps (as a % of total op expense).

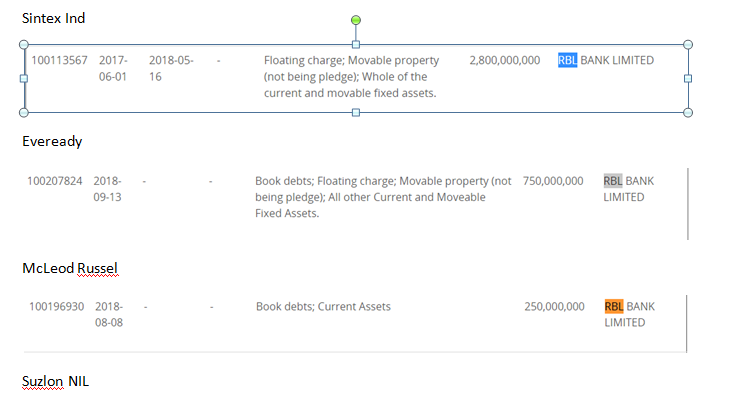

Has anybody idea about how much exposure RBL Bank has to Mcleod Russel group? In the last rating of McLeod it was around 80cr. Is there any other exposure to stressed assets?

Top 20 exposure of the corporate book make up ~11.5%. The concentration has been declining. It was above 12% at the end of FY18. Top 20 exposures make up for ~INR35bn. Avg size of the top 20 exposure: INR1.74bn. It is unlikely that Mcleod would be part of top 20. Even if it is the exposure may be between 100cr-200cr which is ~0.3% of the total loan book. Don’t think Mcleod alone will have any major role in determining what happens with RBL’s asset quality. However, if you have large number of accounts similar to Mcleod, then it can affect. Another name that I heard is Sintex where the exposure might be quite low. I think the point is that bank is unlikely to take a large exposure to any one corporate account but given the liquidity issues and very weak economy, we may have issues with many small accounts. Exposure to sectors like Infra inc power (7.4%; Power 3.4%), NBFCs (3.9%) and CRE (6.6%). When I met the management in March, it indicated that RBL’s RE book is mainly to top notch developers and the yield on the RE book is ~10%, which is low for the sector only because it has been lending top developers. Having said the management acknowledged that the RE industry is facing lot of issues especially developers in Noida, Gurgaon and part of Mumbai.

Net NPA ratio was 0.65 percent against 0.69 percent in the previous quarter.

Provisions for bad loans increased 6.6 percent sequentially to Rs 213.2 crore, but provision coverage ratio improved to 69.13 percent in Q1FY20 against 65.30 percent in Q4FY19.

Slippages remained high at Rs 225 crore at the end of June quarter against Rs 206 crore in Q4FY19.

Even write-offs were higher at Rs 147 crore in the quarter gone by, against Rs 91 crore in the previous quarter.

“The bank has had a good quarter of strong performance and has continued to maintain its growth momentum and improvement in operating metrics. However, given the difficult environment, we do expect to face some challenges on some of our exposures in the near term,” Vishwavir Ahuja, MD & CEO, RBL Bank said in a BSE filing.

While addressing a press conference, he said the bank sees a slight deterioration in corporate exposures in the next 2-3 quarters. “Tight liquidity and volatile equity market are impacting the liquidity of some of the clients.”

“We could incur additional 35-40 bps credit cost owing to additional provisioning requirements. Gross NPAs could rise to 2.25-2.50 percent over the course of the year, but capital position continues to be comfortable,” he said, adding issue is specific to certain corporates, not related to realty and energy.

RBL Bank reports advances growth of 35% in Q1 FY20, Operating profit increase of 43% and Net Profit increase

of 41% at 267.1 crore on a YoY basis

Key financial highlights:

Q1 FY20 Net Profit up by 41% to 267.1 crore

Advances (Net) at 56,836.7 crore and Deposits at 60,810.9 crore both increased up by 35% on Year on

Year (YoY) basis

Net Interest Income (NII) up by 48% to 817.3 crore

Other Income up by 48% to 481.2 crore

Core fee income up by 42% to 411.1 crore

NIM improves to 4.31% up from 4.04% in Q1 FY19. Cost to income ratio is at 52.35%

Gross NPA ratio at 1.38% (1.40% in Q1 FY19); Net NPA ratio at 0.65% (0.75% in Q1 FY19); Provision

coverage ratio increases to 69.13% (60.41% in Q1 FY19)

Return on Assets at 1.31% up from 1.26% in Q1 FY19;

Management guided cost of capital to increase by 40 bps and also in next 6-9 months NPA would increased to 2.5%. This has spooked the market. Market is latching onto deterioration in asset quality hence sharp sell off. Though RBL is correcting since last 1 week or so, maybe someone with knowledge knew about the result.

In an interview today MD said the bank may face worsening asset quality in few high quality large corporate. He is expecting these stress to play out in next 7-8 months.

Important question here is who are these large high quality corporate? Are these new additions to the list of already stressed companies?

Hi Gaurav, do we have transcript of mangement available.

I was looking at there investor relationship page and was able to find out only Investor presentation or out come of board meeting. In these only thing mentioned is :

Commenting on the performance Mr. Vishwavir Ahuja, MD & CEO, RBL Bank said “The Bank has had a good

quarter of strong performance and has continued to maintain its growth momentum and improvement in

operating metrics. However, given the difficult environment we do expect to face some challenges on some of our

exposures in the near term. At the same time, given the strong momentum in our businesses, we do expect to

maintain a healthy profitable growth over the coming quarters”

I am just trying to figure out which all “high corporates” are expected to default.

Being a newbie pardon me if I have missed something.