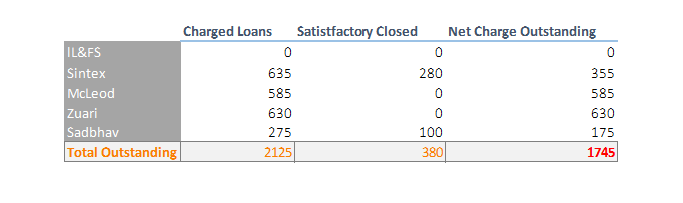

So this would be 380 cr total exposure which the management said would go bad.

These are not high quality names. These names are mostly known to the market and if I remember correctly they have already defaulted.

PFA, list of highly leveraged companies. I have feeling we are looking at 2-3 new entrants in next 2-3 quarters.

List of Heavy Debt Companies.pdf (671.5 KB)

1 Like

Hi all

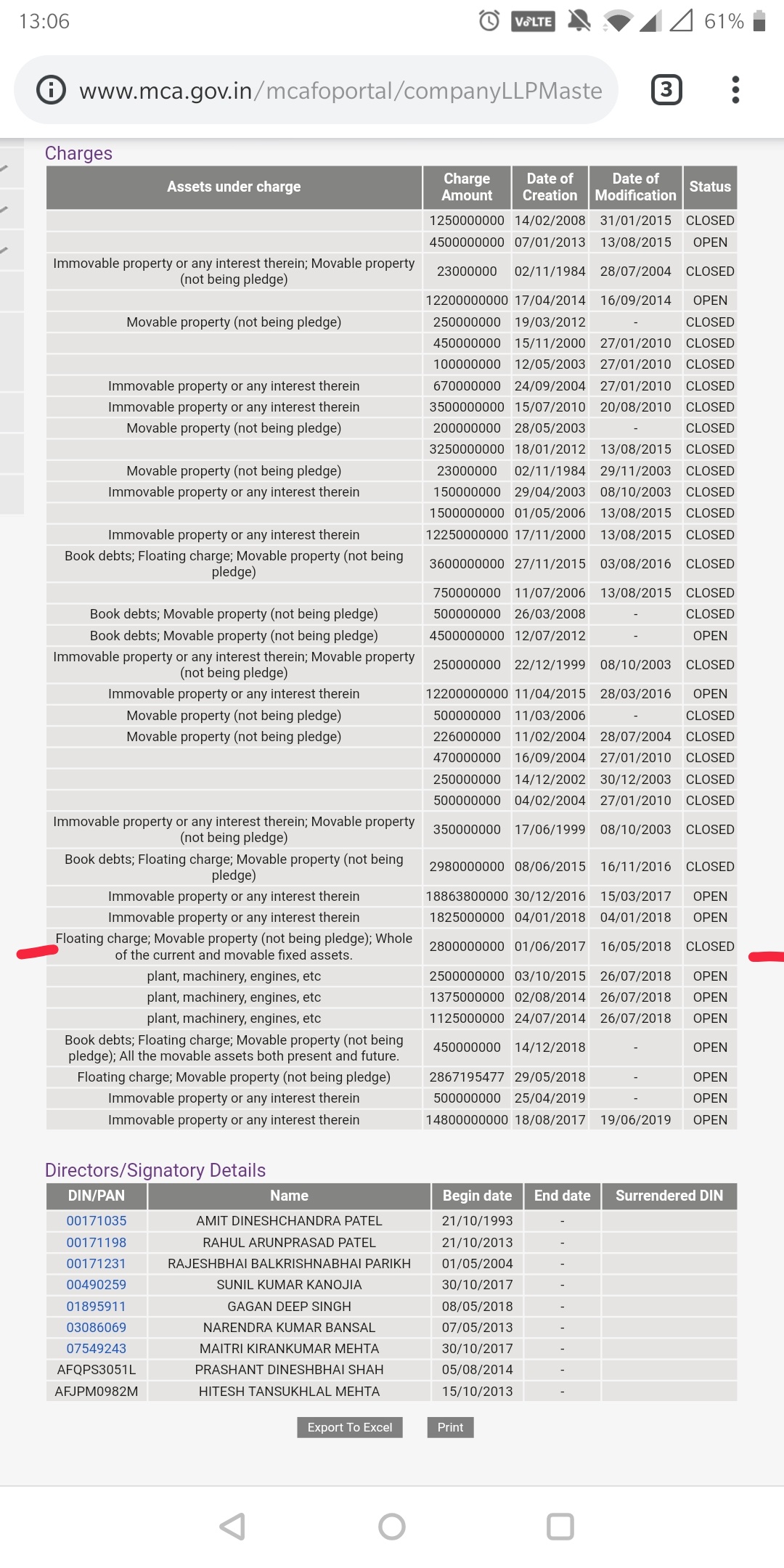

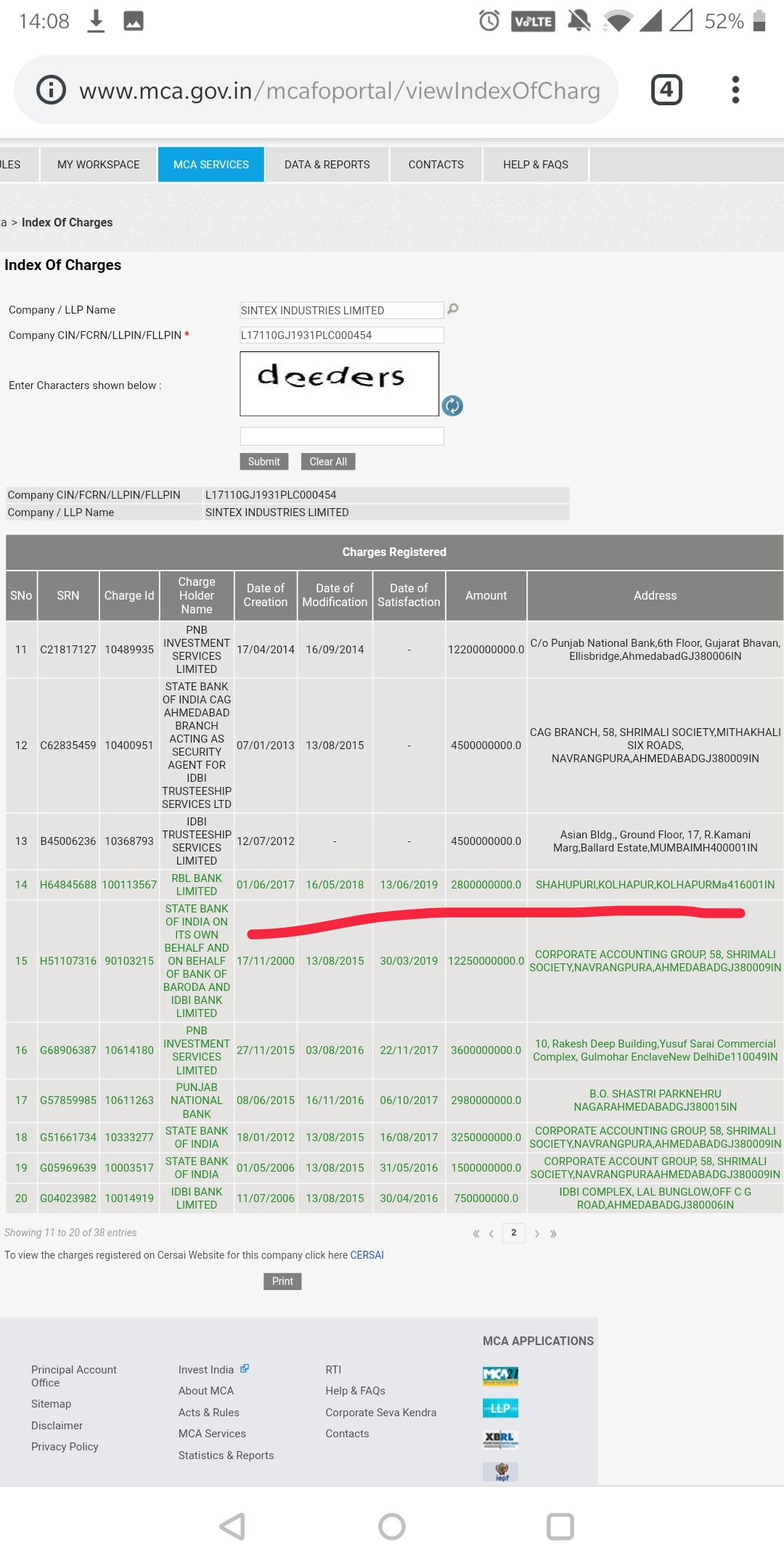

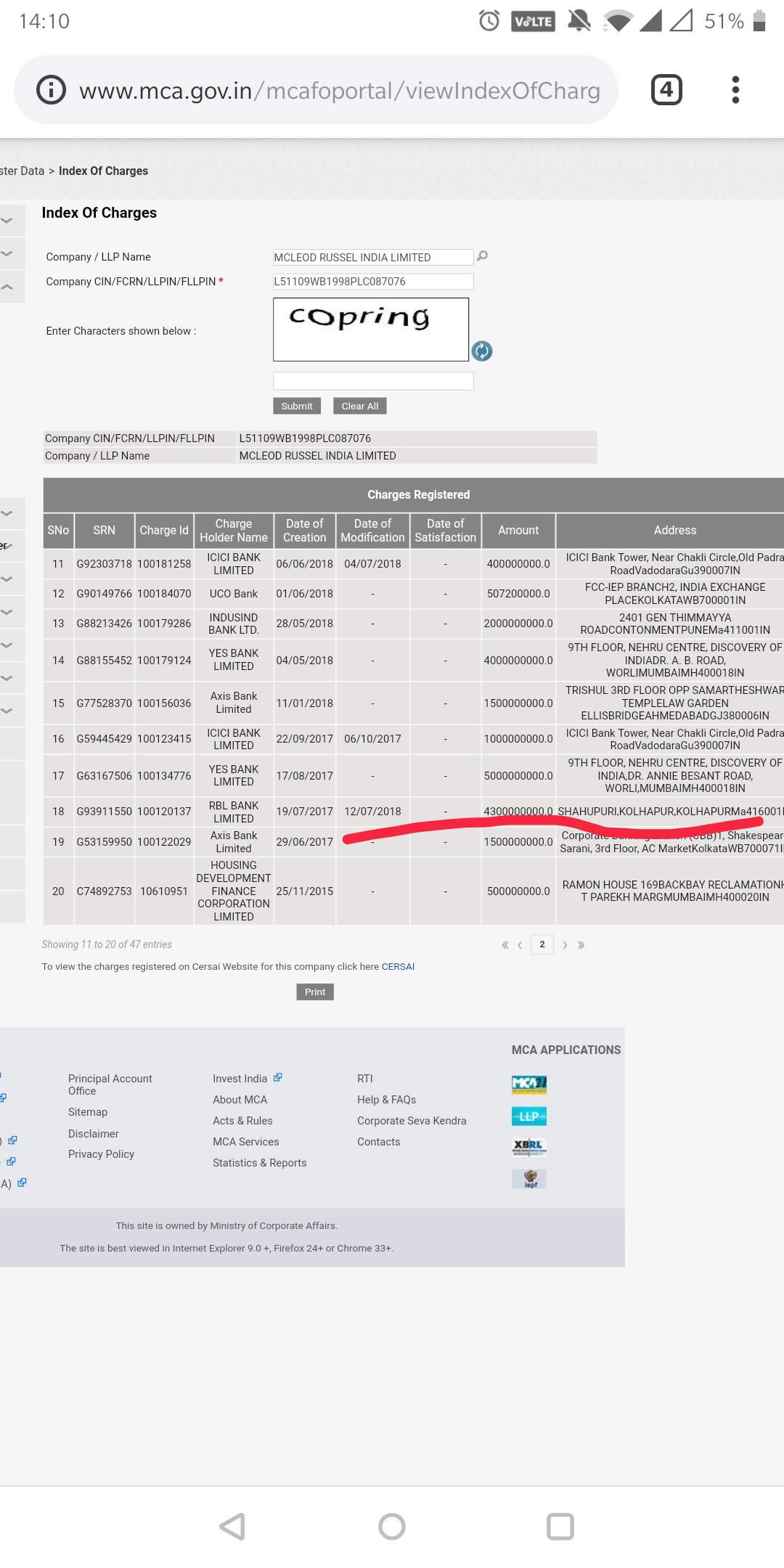

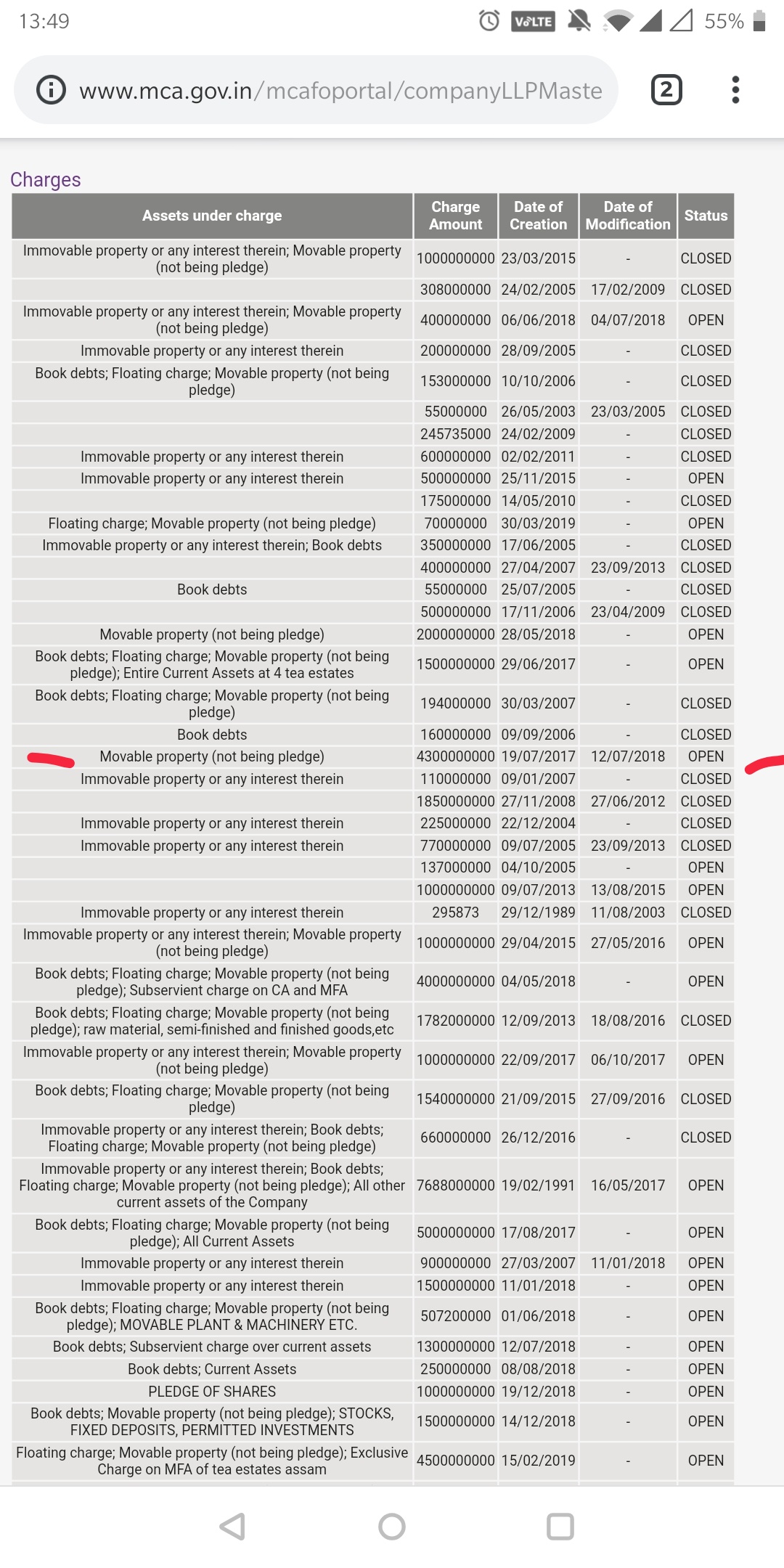

Would request if we are sharing the charges raised on MCA then proper statuses also be shared as it can mislead. For instance the charge against Sintex Industry is closed and satisfaction of charges is also mentioned whereas McLeod is open. For further details please see MCA website. This is public data as per companies act I believe.

Just my suggestion. This is my limited understanding. If a CS can give his or her views it would be great.

If we want we can easily make a spreadsheet of bank wise charges against the list @Gaurav_Agarwal has mentioned. I think it will be super useful!

Python scripters please raise your hands ![]()

Rgds

Disc: views biased as I hold RBL in active portfolio

2 Likes

The total amount of so called watch list was around Rs 1000 cr thus , there could be more names or exposure higher than the amount of charge created over the security.

Disclaimer : This answer was first posted as a thread on Twitter. Views are my personal opinions only. I do not hold a stake in RBL Bank.

Fall in Share Price

RBL Bank posted a steep fall in its share price on 19–07–2019, after the publication on the Q1 results for 2019–20:

A History Lesson

Before getting to my view on why this happened, let’s turn the dial back a little. Ever since 1943, Ratnakar Bank was always a ‘traditional’ bank in most senses of the word, or at least ‘traditional+’ in a way of saying. Even in the 5 years leading up to 2013, the bank was deriving most of its Operating Profits from the financing business:

Then something changed it 2013–14. The bank was rebranded. ‘Ratnakar’ became ‘RBL’. Under the vibrant Mr. Ahuja as the CEO, a lot of re-juggling happened in the top management too. But perhaps the most impacting move was the purchase of the Credit Card business from RBS. In an old article, Mr. Ahuja is quoted saying:

“We want to be a mass-banking institution rather than an urban-centric bank.”

Almost immediately from the next year, the business strategy took a turn. This is evident from the stark topsy-turvy in the bank’s financing profit’s (Should I say, loss?) contribution to the bottomline:

From 2013–14 to this day, ‘Other Income’ has contributed to almost all of the company’s Operating Profits.

Sneak Peek

Now that that’s agreed, what does RBL Bank’s ‘Other Income’ consist? Here’s a sneak peek from their 2018–19 Annual Report:

If you do a little more digging around, you will realize that the following activities became the bread-winner at RBL Bank:

- Investment/Trading in Securities

- Deposits with the RBI

- Forex Transactions

- Derivatives Trading

- Precious Metals Bullion Wholesale

There’s nothing wrong with a change in strategy. In fact, I am all for experimentation by companies. But it’s only a question of how much resources are being committed based on how successful it is.

“Vision 2020″

The whole switch-up scenario in the bank’s activities was further aggravated by the “Vision 2020”. Here’s a snippet from when RBL Bank’s ‘Vision 2020’ was first ‘envisioned’ in the 2014–15 Annual Report:

“ It is now the beginning of the next phase of our journey aimed at achieving leadership in our target segments and geographies. This is both exciting and challenging. While we believe that we have strengthened our capabilities and our expectation for the future remain high however, the macroeconomic environment still has a lot of uncertainties, which may prove to be a challenge in the medium-term. Our strategic roadmap will revolve around a strong capital base, cutting edge technology architecture and getting on board the right people to build a highly customer-centric service and delivery organisation. And that is what our ‘Vision 2020’ strategy entails. ”

‘Vision 2020’, which started out in 2015 as a vague promise ‘to be better’, was suddenly given numerical targets in the 2018–19 Annual Report. Just a year later, in the latest Annual Report, the bank claimed that it had achieved these ad-hoc targets ‘all along’:

Notwithstanding this… whatever this is, if you happen to read in detail about what the bank plans to achieve going forward, you will realize that they want to:

- Grow their CASA/Fee income (Traditional financing)

- Maintain the current ratio ‘Other Income’ (Non-traditional activities) to Total Income

- Grow their MFI lending channels via Swadhhar Finserv (Micro financing)

- Make in-roads into FinTech

Those are some steep targets spread across a variety of landscapes. But they look like they have lived up to the expectations and also claim, very confidently, that they will too in the future. But, something’s gotta give, right?

Here Comes the Money

What the ‘Vision 2020’ probably didn’t mention (At least explicitly) that this will burn a LOT of money. In 2016–17, the bank went for a Rs. 1212.97 Crore IPO (Then, a whooping ~40% of their Equity, Reserves and Surplus).

Fast forward to 2019. In Axis Capital’s 2019 Investment Conference, RBL Bank’s Mr. Rajeev Ahuja (Head - Strategy, Retail & Financial Inclusion) and Mr. Ramesh Ramanathan (VP - Finance & IR) presented about their bank. They claimed that the bank will be raising new equity capital of Rs. 3,500 Crores in 2020 (Now, about ~45% of their Equity, Reserves and Surplus) and ‘does not expect to raise equity for the next 2 years if growth rates stay a 30-35%’ (Emphasis on if ).

Equity dilution is usually an accepted activity for most banks. But dilutions of almost ~50% in a single go, twice, and possibly more, is not very common. We all know how diluting the Equity base can adversely impact shareholder value.

Knock Knock

So, it is no surprise that the cookie crumbled when the bank delivered two adverse news items along with its Q1 results. Quoting directly from the ET article:

- Provisions and contingencies jumped 51.89 per cent YoY to Rs 213.18 crore in Q1FY20 over Rs 140.35 crore in Q1FY19.

- According to RBL Bank, possible slippages in corporate accounts may spike credit cost by 35-40 basis points. The bank is cautious on some corporate accounts slipping into the NPA category in the next nine months.

In other words, the ‘traditional’ business (Also perhaps the MFI business too) is seeing strong headwinds since the shift in strategy. When the current strategy (Despite what the “Vision 2020” says) is to generate profits from allied activities and expend it on the core financing business, it begs the question of what would happen when the core financing business take a turn for the worse.

Conclusion

I have tried to fit this and more of theoretical discussion about RBL Bank into a Valuation model in my blog post, RBL Bank Valuation: Bank or Banker? or a Quora answer, Dinesh Sairam (தினேஷ் சாய்ராம்)'s answer to Is it the right time to invest in RBL Bank for the long term? if you’d prefer that instead.

In the end, as they say, when you’re buying a bank, you are actually buying the banker. If you believe Mr. Ahuja and his team can actually deliver on their massive Vision, while also maintaining shareholder value, I am not going to argue with you. But given the circumstances discussed above, I would be conservative in that estimate.

16 Likes

However, Ahuja said the disclosure was just a prudent measure and will not derail the bank’s growth trajectory.

“We have come out with disclosures in the past, like after demonetisation. The real impact was actually lower than what we projected. In the same spirit and to remain on the side of caution, we felt we should indicate before there is excessive build-up or speculation. This is linked to the macro situation and it is best to do a thorough assessment, which we have done. It is no …

Hi- with due respect, your rather long winded analysis is flawed in key respects. quick summary:

-

Other income is high so something is fishy- the other income is mostly fee income ( comprising 35-40% of total income) from their cards business which has been growing very fast, other major contributors are treasury income as bond yields fell and general fee income from their cash management business and FX brokerage. All of this is perfectly legit, all banks strive to increase this component as it does not require capital, Indian banks hardly do any prop/derivatives trading. The volatility in fee income is mainly from MTM gains/losses on Government bonds.

-

They frequently need capital- true, so does Bajaj Finance, this is a function of their high growth rates, dilution depends on the book premium/discount at which capital is raised, this is an inherent risk in banking that needs to be factored in valuations.

The structural weakness of RBL lies in its rather weak liability profile ( 25% CASA) vs large banks and recent reliance on unsecured lending through credit cards and MFIs to drive growth rates.

Share price fall is due to a nervous market pricing in a readjustment to book value based on increasing credit costs and potential of further stress in the book. Unsecured lending has higher LGD vs secured loans making the market even more nervous.

Disclosure- no holding

4 Likes

Motilal report on result

HDFC Sec Report

RBK ticked most boxes in 1QFY20, but guidance on asset quality (potential corporate slippages of Rs 10bn) is seriously disconcerting at the very least… Sensitivity to asset quality outcomes is high.

For RBK to meet its growth guidance (~30%), it would need to raise funds in the near future. Recent developments on asset quality dampen its prospects.

1 Like

At one point of time RBL was my largest position over 25%+ in my portfolio. These were bought before IPO and post IPO in a year or so it generated huge wealth for me. My understanding at that point of time was this:

a) The bank emerged from the shadows of Ratnakar bank and it was growing at a breathtaking pace, V Ahuja and the team that he had were doing a fabulous job on growth/risk management/asset quality and digital infra.

b) The NPAs had all but vanished.

c) There were marquee investors who had invested in the bank including IFC, Faering Capital and a lot of others who participated in multiple dilutions before bank got listed.

d) Mr V Ahuja had put his entire capital and energy in the bank.

As I read more I realized my lack of understanding of how financial institutions should work and how they do. One of the most defining books I read and also presented in VP Annual meet was ‘A blueprint for better banking’ by Niels Kroner. In this book Niels Kroner describes about ‘Svenska Handelsbanken’ a Swedish bank and how it approaches banking. You can look for it here:

Neils Kroner also described the ‘The Seven Deadly Sins of Banking’ in that book as follows:

- Imprudent asset-liability mismatches on the balance sheet

- Supporting asset-liability mismatches by clients

- Lending to “Can’t Pay, Won’t Pay” types (for extra basis points)

- Reaching for growth in unfamiliar areas

- Engaging in off-balance sheet lending

- Getting sucked into virtuous/vicious cycle dynamics (growth is an outcome of credit which is an outcome of growth until it isn’t)

- Relying on the rear-view mirror

Anyone who wants to have a better understanding of banking should go through Neils Kroner’s book. In my mind the above sins would play along with the following

- When a bank/financial grows faster than the underlying segment one really needs to be cautious.

- Growth/Degrowth in financials is an outcome and shouldn’t be made a target.

- Own your underwriting. Dont buy loans from the market and don’t lend to lenders. This will avoid any system wide liquidity hazard.

The above ideas made me re-think my investments in financials and RBL. I slowly exited my position in RBL (and felt like a fool for sometime) and also could avoid the growth toppers and growth guides like Yes/DHFL/IndiaBulls/Reliance Cap/Reliance Home/PNB HFC/ and a whole lot. I did dabble into a fast growing mcap but exited quite early.

How do I see RBL now: RBL’s business model has some fundamental flaws and these flaws were all hidden by the stupendous growth fueled by continuous capital raise. Most people believed the story and paid a premium for the growth. A few things that got ignored and were pointed out by @rupeshtatiya and other folks over time:

a) NIMs to RoA: With NIMs of 4.3% the bank still only manages around 1.2% RoA. This implies that bank is operations heavy. One could really question if the bank made any money from its lending and with the current provisions it could very well be they have lost some.

b) The ESOP strategy: Also the amount of ESOPs issued is mind boggling. One look at FY19 AR the bank allotted nearly 70 lac ESOPs at Rs 143. The bank also had 3.05 crores of ESOPs at an exercisable price of 438.

c) The branch strategy: Corporate lending is easy. Retail branch opening is tough, expensive and costs a lot in the initial years. I am very certain the decision to open fewer branches was a clear outcome of Vision 2020 with 15% RoE and other matrix.

d) The bank has significant exposure to MFI segment. Direct MFI lending can have NIMs in excess of 8%. Despite this the RoA remained sub par.

e) A question that was asked in the conf. call and was brushed under the carpet was the book size when these bad loans appeared. Assuming that these loans appeared around 2/3 years back when these loans by themselves would have been 30% to 50% of bank’s net worth.

f) Finally, RBL bank had a halo: a halo of being a different corporate bank with proper risk management, conservative and prudent underwriting and a great team. The halo is now lost. In some of the documents from MCA or other sources the kind of loans that the bank gave were pointed out. The sintex loan is telling, the loan was closed but the real question is why was it given? I know the answer: for a few basis points more.

Disclosure: No investment in RBL. Have investments in other fianncials.

35 Likes

Please point to the place in my entire post where I used the word ‘fishy’ or ‘suspicious’. I simply pointed out that the bank’s targets are ambitious. I even concluded by saying that if the investor believes the targets can be met without considerable shareholder value dilution, then I am not going to argue with that anymore.

Equity Dilution is not uncommon in Banking companies. So, it’s not a question of ‘Why?’, rather a question of ‘How much?’

Again, this ties back to my previous observation. I am simply quoting the company’s own employees saying how much capital they would require. If all that dilution makes sense for you as an investor, then more power to you.

1 Like

Good analysis. U were prescient with Edelweiss as well when entire world was gung ho on it n itnwas reaching new ATH. Kudos. Keep up the good work.

Dinesh - thanks for your note. A few points here. The Vision 2020 wasn’t something invented now. They have had it in their presentations in quantified format (30-35% Cagr etc) since Q2 FY17. See here: https://ir.rblbank.com/pdfs/financial-highlights/Investor_Presentation_Q2_FY17.pdf

Second, This concept of financing profit is incorrect, IMHO. (there’s no concept of EBIDTA in a bank - you have to take out interest, but anyhow) For instance 2016 was other income of 491 cr. (correct) but where did the 477 cr. number come from? It might be that you are considering that all costs for the bank relate to only the financing business- which is not true. From trading, to fees, to card costs etc. there are substantial costs related to fee income only, which therefore should not be conflated with the financing costs (even part of branch costs are fee income related).

Third, income from investments is required to be noted as interest income. You as a bank are reuqired to put 20% of your deposits in govt bonds. This generates income from investments. If you remove that, you should remove the 20% of interest paid on deposits as well, which is not really the right thing to do. The interbank and RBI interest isn’t much - just 70 cr.

Fourth, you don’t look at a fund raise as % of equity or reserves. You look at it as primarily about how much it will dilute the bank’s equity, and how much it will change the basel capital ratios and for how long. The dilution is not 50% or anywhere close to it. If anything, it might be 10%, and yes, it will substantially reduce RoE until they get to use the capital properly.

Q1 provisions are higher, perhaps and that’s good - the point is to provide high enough to cover for NPAs, or even higher. (Also note that income is up 50%, PBT is up 50% and so on - so it’s not unusual to see a provisioning also go up at the same rate)

It’s useless to defend a bank’s numbers. They can invent what they want. HDFC doesn’t generate a 20% profit growth yoy every single quarter without some kind of change they have power to do. In the end, like you said, it’s about your trust in bank management. But I would like to debunk any mentions that seem incorrect in my opinion, even if it may not change anyone’s view on the stock or the bank.

23 Likes

I only have one thing to say. High growth in lending business shouldnt be looked at negative always even if others are not growing at that pace. Even HDFC bank grew 100%+ in initial years when sector underperformed. Its good to gain knowledge from books but finally price action makes opinions as in this case.

Most of the corporate are facing liquidity issue due to tough economic conditions and if you see the corporate exposures most of the banks have exposure to these troubled corporate even the so called good banks with superior underwriting skills.

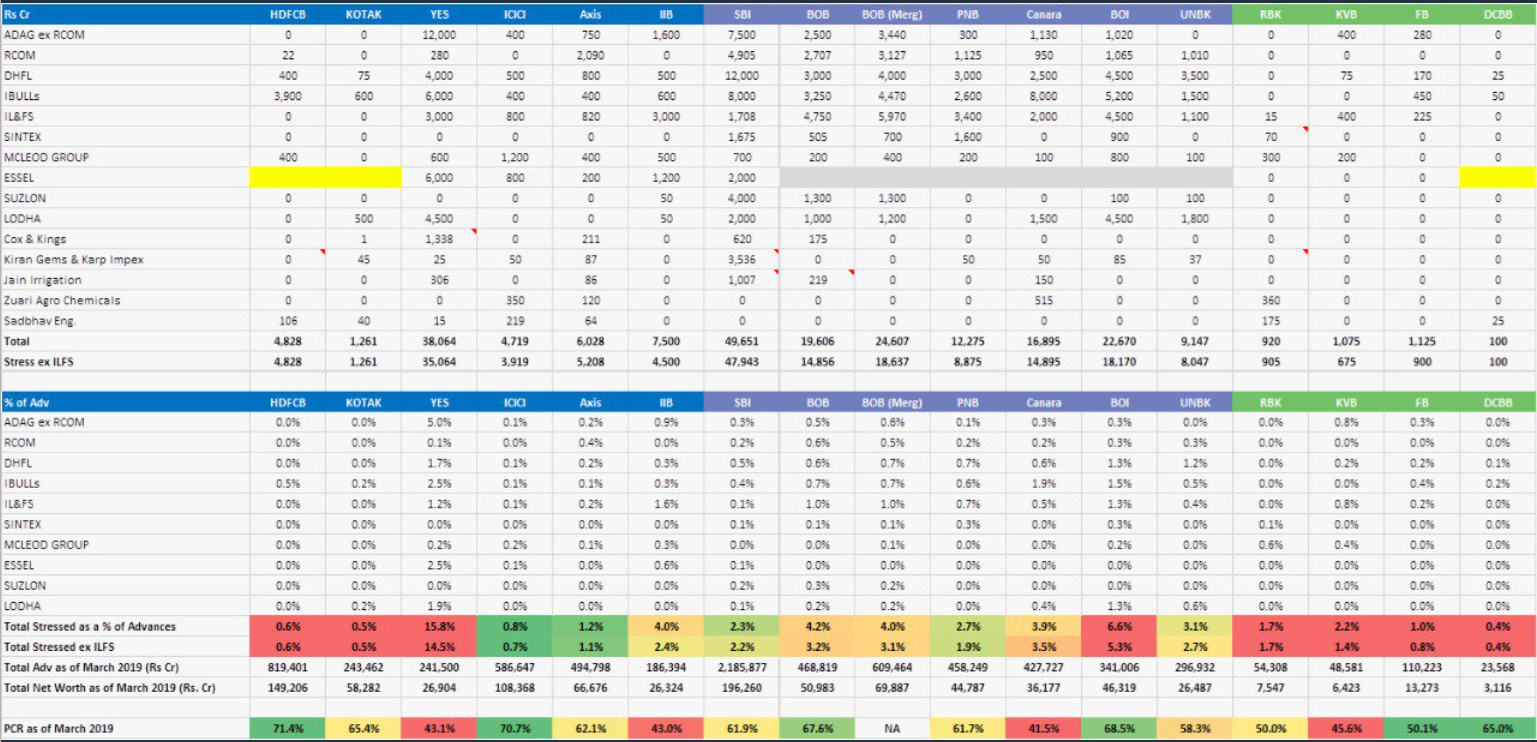

Here is the list of stress account exposure to banks shared by virendra bansal.

3 Likes

Completely agreed on the expenses part. There’s no way to dice and arrange them neatly.

Also, I did mention that “Vision 2020” was created in 2015. But the “targets” were only assigned mid-way. And claiming to have achieved the targets just a year after deciding them feels a little odd to me. But that may just be my bias, hence the warning that the entire post was just an opinion, not an iron-clad case study.

If I still didn’t come across correctly to anyone, let me try to summarize:

- I think the bank’s goals are tall and spread across a range of landscapes. So I hold the opinion that some focus is in order.

- If the investor believes that the bank is going to achieve all the targets anyway, the question of how much shareholder value dilution is going to happen in the process also needs to be considered.

- If the shareholder is also ready to put up with the dilution, then I have nothing more to say.

4 Likes

Hi

Thanks for this. I had one difference when I saw this yesterday. In my knowledge RBL has a larger exposure than what is given here. I think this is ending FY19.

The companies which in this table to whom RBL has given loans to is what I have checked manually. I have gone through all their subsidiaries and related party companies as per latest report. Off-course I could have made manual errors or missed something but below are my findings.

Number of companies whose charges studied

As of today what is the status

This is just under double the number quoted in the table.

There will be more companies where RBL has lent to e.g. Eveready Ind which doesn’t figure in this table.

Aside from this I am a tad surprised that these outstanding numbers are in public domain but before the price collapse it appeared a screaming buy at <500 levels with ~100% confidence levels as per valuations and now we are finding reasons to say why ‘I told you so’.

Reminds me of Mark Twain’s quote - It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so

The kind of analysis @rupeshtatiya bhai has proactively done and shared on this was really good. He asked a good set of questions and we don’t have answers yet. This was done right at the peak of the price when most of us didn’t bother to dig around.

Rgds

Deepak

disc: invested but reduced position due to stop loss

9 Likes

@deevee Thank you for good analysis and matter of fact view on change of mood of the street and I am also very surprised on the change of discourse. It started much before results supposedly as rumors. That would mean many knew what kind of warning signals going to come.

With these stressed loans and provisions overall the situation is better than few other banks trading in similar P/B valuations. So what goes in such a strong reaction in market? Is it possibility of more cockroaches coming out in the open over the time?

What strategies you use to determine stop loss? Is it is fixed % from the top or do you use technicals to determine one or another way to protect from loss ensuring a percentage profit. Would like to know.

Disc: about 4% of PF, added some at 500 levels

On the “Vision 2020” part. The stock was listed in 2016, and the FIRST EVER presentation released had the quantification of the vision 2020. It was not invented later as per the accusation above. They did not achieve it a year later, they are still in the process of getting there (haven’t yet got there). I think saying that they put the figures in later is not correct, and unfairly accuses the management of what is considering wrong. I understand your post was an opinion, but I’m going to provide facts.

Here’s my opinion further:

- The banks goals ARE tall, but every bank in the country has to have tall and widespread. This is not about focus - it’s about the economies of scale in banking being achieved only through a widespread approach. People approach banks with financial problems - investments, credit and payments. You have to have solutions to offer and that’s what reduces your cost to income ratio in the long term.

- Dilution as I mentioned, is at equity levels. You have to look only at how many more shares they will issue. At 10% or 20% levels over the next six years is a given, considering capital requirements. This should help them get to some part of their goals if not all of them. If the contention is that they will need to dilute 100% and raise 20,000 cr. in equity (that’s the current market cap) then I don’t really have anything more to say.

5 Likes

RBL Bank expects to grow by up to 20% this fiscal: Rajeev Ahuja.

1 Like