Hi

Caution: Another long post. Apologies.

Well I am guilty of showing only one side of the coin in my earlier post on the disruptions in retail banking. As pointed out I should shed some light into what matters for us as an investor in banking. I am sure most of us know how a bank functions and how it makes money. I will try to answer how these disruptions ‘could’ add value to banks and some pointers on how we value such companies.

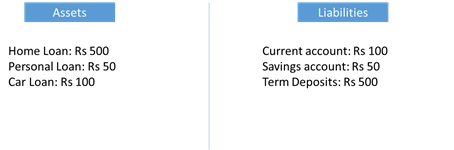

Liability vs Assets in Banks

Banks take deposits from their customers in the form of current accounts, savings accounts, fixed deposits and recurring deposits. This deposit base is ‘given’ out to the borrowers. So in a very simplistic fashion we can say the ‘debt’ or ‘liability’ which the bank has taken on its books by accepting deposit is invested by giving out loans to customers. The differential rate is the income which the bank makes. So the traditional language of debt in a banking parlance is the deposits base or the liabilities it takes on. The investment of this liability is in loans which are assets for the banks which earn a higher interest rate. A modified balance sheet (leaving equity aside) of a bank will look like:

Income Generation in Banks

From where all and what type of income does a bank have? Banks earn two types of income – interest income and non-interest income also called fee income. A bank when it takes deposits from customers receives float. This float after appropriate adherence to reserve ratios earn an income for the bank. This is called float income. For instance the bank is paying 4% interest to its savings account holder, this is a cost to the company. Basis this it can have a portion of its capital earn money in money market or basis this deposit base the bank lend to a consumer at say 12%. The difference in interests is the Net Interest Income at a high level. The bank has to match duration of its assets to its liabilities so that there is no asset liability mismatch. This is usually done by a team in treasury usually called the Balance Sheet Management Group. For overnight requirements or short term requirements many avenues are present to the banks.

The bank makes interest income from all forms of loans (which are assets to a bank eg home loan, car loan, personal loan, overdraft, education loan, the notorious corporate loans etc). Also from credit cards it makes interest income in case of revolving accounts or default accounts. Do read about revolving accounts.

On the fee income side the bank makes fee on transactions of all sorts whether its cheque issuance, cash collection, remittances, merchant payment acceptance etc. To get a glimpse have a look at the schedule of statement here for YES Bank. You will see both a fee income and an interest income component.

The wholesale side of banking is perhaps the most steady income generator for a bank, investment banking earns a lot of fee income, treasury income is also steady and last the retail side just manages to make money for small banks. But without having retail the wholesale side loses balance. Without retail banking ie deposit base you can’t grow as a bank.

The above section was to just give a background. Pardon me.

Let’s take each FinTech item and see what they can do at an overall level to the income of the bank.

Payments by wallets

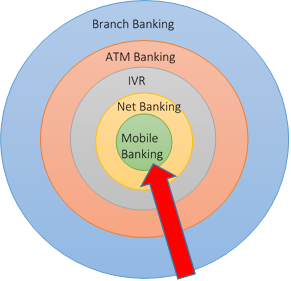

If you notice my last post I pointed out that banks prefer to be in the payment processing and escrow services fee business. Why? Escrow gives them a huge float income. For instance Paytm maintains say 500 crores with its escrow banker. By payment processing I mean that say when a consumer decides to use his wallet to send money to another bank account then IMPS service for money transfer gets used. For providing this IMPS service the bank charges the wallet operator. Another thing which I referred to is that banks do BIN sponsorship. Say a wallet issuer like Itzcash has an RBL BIN sponsored card. Whenever the card gets swiped Itzcash earns 1.1% of the transaction value and the BIN sponsorship agreement will say that 20% of this income will be that of the BIN sponsor bank. So in essence by virtue of being a bank it gets both fee income and float income by just entering into a BIN sponsorship. Look at RBL they have the most! Likewise banks earn from these fintech payment partnerships. Now coming to the fact of floating a bank wallet like say ICICI Pockets or an HDFC PayZapp (with due respect though Mr Aditya Puri has written off wallets but HDFC has two wallets Payzapp and has investment in Chillr I believe). The advantage these own wallets for banks give is 100% share of the fee income on transactions, they are akin to spends on credit cards. So more the users use their own wallets the better it is for banks. Again let me ask why? The more the user uses the more balances he keeps thus more float income. One more – why should he use the wallet to transact why not withdraw from an ATM and purchase with cash? Leave aside inconvenience, the banks always want customers to use their phones without contacting them to transact. The below diagram shows what the banks are trying to do that is to shift the customer to transact on their own using their handsets. Again why? Because of negligible costs in doing so. Our bank hates it when we walk into their branches!

Also when we talk about payment banks we should not write them off. I was part of the team in Airtel Money which got the license for the Airtel Payments Bank (the first one to get). Payments bank can earn fee income and have potential for cross sell. I believe telcos have an upper hand here as they have the distribution reach which is a huge asset to them in this payment banking space. Also please understand payment banks were created with the aim of financial inclusion. Financial inclusion is a very thin margin business. Thus size matters to a great extent. I am not aware how P2P lending is trying to make money but have some idea.

Now we have asked why we can’t use PE ratio to value banks. I purposely gave the above background on how banks make money. I would earnestly recommend you read Prof Damodaran’s 75 pager on how to value financial companies. I have attached the document but anyways quoting excerpts from it.

When we talk about capital for non-financial service firms, we tend to talk about both debt and equity. A firm raises funds from both equity investor and bondholders (and banks) and uses these funds to make its investments. When we value the firm, we value the value of the assets owned by the firm, rather than just the value of its equity. With a financial service firm, debt seems to take on a different connotation. Rather than view debt as a source of capital, most financial service firms seem to view it as a raw material. In other words, debt is to a bank what steel is to General Motors, something to be molded into other financial products which can then be sold at a higher price and yield a profit. Consequently, capital at financial service firms seems to be more narrowly defined as including only equity capital. This definition of capital is reinforced by the regulatory authorities who evaluate the equity capital ratios of banks and insurance firms. The definition of what comprises debt also seems to be murkier with a financial service firm than it is with a non-financial service firm. For instance, should deposits made by customers into their checking accounts at a bank be treated as debt by that bank? Especially on interest-bearing checking accounts, there is little distinction between a deposit and debt issued by the bank. If we do categorize this as debt, the operating income for a bank should be measured prior to interest paid to depositors, which would be problematic since interest expenses are usually the biggest single expense item for a bank.

The price to book value ratio for a financial service firm is the ratio of the price per share to the book value of equity per share. This definition determined by variables– the expected growth rate in earnings per share, the dividend payout ratio, the cost of equity and the return on equity. Other thing remaining equal, higher growth rates in earnings, higher payout ratios, lower costs of equity and higher returns on equity should all result in higher price to book ratios. Of these four variable, the return on equity has the biggest impact on the price to book ratio, leading us to identify it as the companion variable for the ratio. If anything, the strength of the relationship between price to book ratios and returns on equity should be stronger for financial service firms than for other firms, because the book value of equity is much more likely to track the market value of equity invested in existing assets. Similarly, the return on equity is less likely to be affected by accounting decisions.

Thus while quickly evaluating banks we must look at

- Deposit and advances

- Quality of assets

- NIM

- P/B and ROE

Other pointers:

I diligently do not follow NBFCs. I used to hold Capital First but have exited it due to certain uncomfortable reasons. Not that it is not worth holding onto. Bajaj Finance I believe has entered into a partnership with Mobikwik. There you go. I see people like Angel Broking and Motilal Oswal going into something like robo advisory where the algo recommends investments/trades/capital allocation. Haven’t seen it up close though. On bank side like I said all private sector banks are doing well in the fintech space. Do not expect them to turn the tables in a year! We Indians love slow, extremely slow and steady pace ![]()

Sir I envy you having been an investor in HDFC for 15 years! An awesome investment it would have been.

Hope this quickly written out post made some sense.

Regards

Deepak

Valuing Financial Firms_Damodaran.pdf (103.6 KB)

Suggestions on Valuation Books: McKinsey on Valuation and Damodaran on Valuation.