Hi

Thanks for this. I had one difference when I saw this yesterday. In my knowledge RBL has a larger exposure than what is given here. I think this is ending FY19.

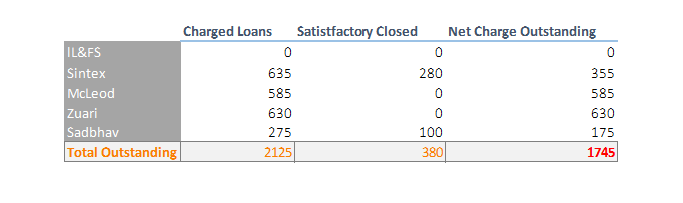

The companies which in this table to whom RBL has given loans to is what I have checked manually. I have gone through all their subsidiaries and related party companies as per latest report. Off-course I could have made manual errors or missed something but below are my findings.

Number of companies whose charges studied

As of today what is the status

This is just under double the number quoted in the table.

There will be more companies where RBL has lent to e.g. Eveready Ind which doesn’t figure in this table.

Aside from this I am a tad surprised that these outstanding numbers are in public domain but before the price collapse it appeared a screaming buy at <500 levels with ~100% confidence levels as per valuations and now we are finding reasons to say why ‘I told you so’.

Reminds me of Mark Twain’s quote - It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so

The kind of analysis @rupeshtatiya bhai has proactively done and shared on this was really good. He asked a good set of questions and we don’t have answers yet. This was done right at the peak of the price when most of us didn’t bother to dig around.

Rgds

Deepak

disc: invested but reduced position due to stop loss