Hi all forum members

I have been following VP for almost a year now, and this forum has been helpful in improving my investment process.

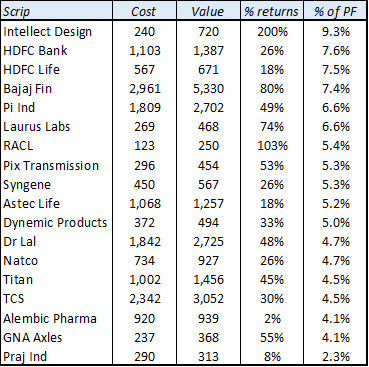

Below is my portfolio along with the rationale for selecting my picks.

-

Alembic Pharma

Buy price - 954, Current price - 935, 4.5%

Solid compounder with a portfolio of complex generics in the US and an exposure to India market. -

Astec Life

Buy price - 1092, Current price - 1058, 4.7%

Agro-chemical company specialising in fungicides. Has the potential to build on its CSM base and become a midcap over the decade -

Bajaj Finance

Buy price - 2750, Current price - 5476, 7.7%

Exposure to consumer retail including durables, auto and mortgage lending. Excellent promoter quality. -

Dynemic products

Buy price - 368, Current price - 365, 4%

Manufacturer of dyes, especially food colours, so finds application in steady FMCG and Pharma businesses. CWIP block of 3x the current block is a trigger for a huge boost in fundamentals, especially as competitor Vidhi is also putting capex (meaning tailwinds are across sector). Dynemic is ahead of Vidhi by at least 1.5 odd years in terms of realising revenue from capex. -

GNA Axles

Buy price - 231, Current price - 367, 4.5%

Auto ancillary catering to tractors and commercial vehicles. Value play with market tailwinds as commercial vehicles on the export side are picking up. Reasonable exposure to domestic+export markets makes it less prone to cyclical shocks -

HDFC Bank

Buy price - 1047, Current price - 1584, 8.5%

Proven compounder in the banking space. Best risk management in the sector. -

HDFC Life

Buy price - 553, Current price - 719, 8%

Market leader in private sector life insurance space; potential to gradually eat away LIC’s share -

Intellect Design Arena

Buy price - 240, Current price - 447, 6.5%

Polaris spin off, one of the leading firms in transaction banking software space. Margin expansion play. -

Lal Pathlab

Buy price - 1831, Current price - 2391, 4.5%

Leading player in diagnostic sector. Potential to become a large cap over a decade. -

Laurus Labs

Buy price - 266, Current price - 359, 5.7%

Phenomenal growth story from being an ARV API player to a broad based FDF+API player. Excellent execution by the promoter so far. -

Natco Pharma

Buy price - 723, Current price - 888, 4.9%

Unique proposition of focussing on really complex molecules in the US market. Clean corporate governance. -

PI Industries

Buy price - 1809, Current price - 2228, 6.2%

Steady longer term compounder to become a large cap over the decade. -

Pix transmissions

Buy price - 270, Current price - 375, 4%

Growth in cement, steel and industrial sector should help Pix in the medium term. Further, company has been expanding into export market into non-cyclical segments such as washing machines. -

RACL Geartech

Buy price - 119, Current price - 234, 5.5%

Auto ancillary company making high quality gears for tractors and 2W (premium range). Customer relationships are sticky due to quality. -

Syngene

Buy price - 439, Current price - 574, 5.7%

Contract research and manufacturing is expected to grow over the decades and Syngene is in a prime position to win in this market. Promoter group (Biocon) is honest. -

TCS

Buy price - 2236, Current price - 3213, 5%

Large cap IT compounder to offer steady returns with dividends. -

Titan

Buy price - 991, Current price - 1563, 5.4%

Excellent consumer franchise which can compound returns over the long run. -

Transpek

Buy price - 1599, Current price - 1570, 4.5%

Small cap chemical company which has secured contract with Dupont, the largest chemical company in the world. Potential to develop further large customer relationships.

Overall portfolio has exposure to large caps (41%), midcaps (25%), small caps (20%) and microcaps (13%).

Objective is to generate Nifty + 3-5% returns p.a. over the next 5 years. Please let me know your thoughts.