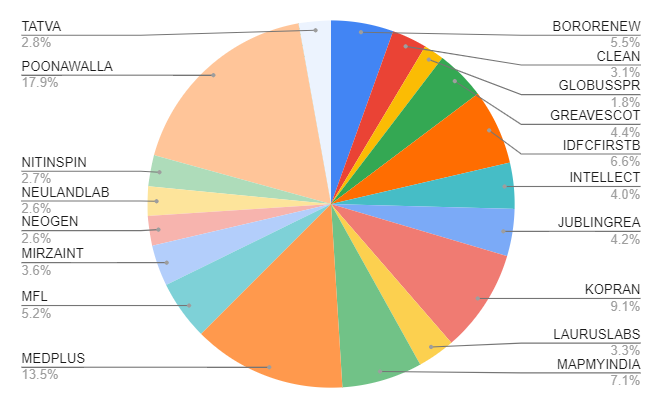

Hi VP community,

Sharing my portfolio below, let me know your thoughts on the overall PF allocation and zoomed out thematic views

| Instrument | Sector | Rationale | Investment % | Current Value % | P&L % |

|---|---|---|---|---|---|

| CREATIVE-BE | Licensing | Honeywell brand licensing would have 2x current EBITDA margins and share of brand licensing slated to go upto 25% in next 2 years. More brand licensing arrangements / extended Honeywell agreement a possibility post successful execution of Honeywell arrangement | 7.30% | 14.02% | 159.59% |

| MASTEK | IT | Evosys / Mastek integration and x-sell resulting in increased ticket size of deals and greater deal momentum; New CEO bringing new direction and energy for US business and overall a massive digitisation investment by companies and governments across the world | 7.25% | 8.97% | 67.29% |

| BORORENEW | Rnewables | Only listed solar glass manufacturer in India. Doing a 4x capacity expansion and may announce further capex in coming times. Possibility of RIL strategic acquisition. Strong R&D capability demonstrated in antimony free glasses, fully tempered 2mm glass. Strong strong focus on solar to meet 50% renewable goals by 2030. China plus one | 7.54% | 6.72% | 20.48% |

| MFL | Chemicals | Got as part of demerger. See it as a co trying to emulate Deepak Nitrite. Current commodity but moving quickly into value added products. Low cost producer due to huge land parcel, leading to lower cost of capex -->higher asset turns —> higher ROCE. New generation wants to prove itself. R&D center announced. Official revenue guidance of 30% CAGR until 2025 | 6.31% | 6.61% | 41.55% |

| IDFCFIRSTB | Banking | Banking on V Vaidyanathan. Strong execution in last 2 years in terms of cleaning up the wholesale book, raising CASA to 50%, QIP at 2.5x book value. Well placed to ride the retail wave. Strong tieup with startups to enhance distribution. Voda is near / medium term risk. | 9.20% | 6.44% | -5.34% |

| ACRYSIL | Real Estate | Beneficiary of global / Indian RE boom. Announced 2x capex in last 1 year. Went from 500k sink capacity to 1.2mn by Q2FY23. Plan to expand into adjacent products. Well placed to cater to rising premium demand in India and low cost contract mfg for global giants. | 5.78% | 6.40% | 49.60% |

| PRINCEPIPE | Real Estate | Beneficiary of Jal Jeewan Mission and increased RE activity. Aggressive management. Only 2nd tie up of Flowguard in India. Near Pan India presence. | 6.60% | 5.12% | 4.94% |

| GLOBUSSPR | Consumption | Premiumisation. Ethanol contracts. Significant capacity. | 2.88% | 4.77% | 124.20% |

| INTELLECT | IT | IT products play. Platform company. Relatively immune from wage pressures as highlighted by management. Attractive valuations to global peer Temanos. Large opportunity size as banks have least IT penetration across the world. Also sticky customers once you sell the product. | 6.51% | 4.49% | -6.76% |

| CLEAN | Chemicals | Process research focussed co exemplified in 70% consistent gross margins and 50% OPM. Current annualised PAT of 200crs. Spending 300crs on capex in next 2 years. Asset turn guidance of roughly 2.5 to 3x with similar margin profile. Peak annualised profits can more than double from here. Co focussed on clean science, targets higher wallet share and market leadership. One of the few cos exporting to China | 4.96% | 4.44% | 20.99% |

| NEOGEN | Chemicals | Speciality in lithium chemistry. Potential EV play. Large capex (3x) on the organic side has come on steam and CSM contracts revenue may come on steam in future. R&D driven co. | 4.21% | 4.02% | 29.29% |

| ESCORTS | Automotive | Beneficiary of agri growth. Special situation candidate with Kubota taking in majority stake. | 0.20% | 3.94% | 2537.36% |

| EASEMYTRIP-BE | Aviation | Proxy to Aviation growth. Low cost model allowing the co to remain profitable. Profits to show a higher CAGR compared to sales due to relative fixed nature of costs. Has narrowed the gap to MMT (market leader) in recent years. Buy price is at attractive valuations. | 5.75% | 3.63% | -14.73% |

| SSWL | Automotive | Attractive valuations. Benefitting from China plus one diversification of vendor base. Capex in past 2/3 years coming on steam and op leverage kicking in. Further 60% increase in capacity via NCLT acquisition. Has the potential to double profits in FY23 from FY22 base, which is already high. Has pass through contracts so no RM inflation risk. | 4.37% | 3.56% | 10.13% |

| JUBLINGREA | Chemicals | Attractive valuations. Focus on moving up the value chain into more downstream value added products (Diketes, etc.). Cumulative capex to double revenue to around 2.5bn USD by FY25 from current levels. | 5.42% | 3.49% | -12.93% |

| TATVA | Chemicals | Similar to clean science. Focus on niche products and dominating market share in them. PTC used in supercapacitors may benefit from the larger green energy push as battery storage becomes more and more common. Q2 commentary indicated that future capex would be on products that could generate 50% ROCEs. | 4.54% | 3.26% | -2.95% |

| LAURUSLABS | Pharma | Typical RIL story of pharma. Make money from commodity (ARV APIs) to enter into new age businesses (CDMO, Fermentation Science, Diabetes and other therapies, etc.). Potential to offer multiple demergers in future. Good momentum in CDMO. | 3.28% | 2.76% | 13.51% |

| NEULANDLAB | Pharma | Focus on complex molecules. Innovator CDMO. Growing CMS molecule pipeline. Unit 3 was commissioned in Q3FY21, to fully operationalise yet. Growing Teva prescriptions and CMS momentum has been strong. Commercial revenues may flow in H2FY22. | 2.75% | 2.45% | 20.49% |

| BSOFT | IT | Beneficiary of IT supercycle. Diversifying away from Mastek. | 1.21% | 1.65% | 84.19% |

| HEROMOTOCO | Automotive | Rationale hasn’t played out yet (growing focus on exports) due to semiconductor shortage and Hero’s entry level segment being targetted by EV players. Might exit this soon and consolidate into one of the other holdings. | 2.22% | 1.19% | -27.86% |

| SBIN | Banking | Might consolidate soon. Old holding. | 0.43% | 0.99% | 210.23% |

| SHREDIGCEM | Cement | Tracking Position | 0.68% | 0.80% | 58.29% |

| UJJIVANSFB | Banking | Tracking Position | 0.54% | 0.20% | -49.34% |

| KOPRAN | Pharma | Tracking Position | 0.05% | 0.05% | 54.42% |

| SEQUENT | Pharma | Tracking Position | 0.03% | 0.02% | -7.41% |

From a thematic / sectoral point of view - the construction is as under:-

| Theme | Investment | CMP% |

|---|---|---|

| Automotive | 7% | 9% |

| Aviation | 6% | 4% |

| Banking | 10% | 8% |

| Cement | 1% | 1% |

| Chemicals | 25% | 22% |

| Consumption | 3% | 5% |

| IT | 15% | 15% |

| Licensing / Consumption | 7% | 14% |

| Pharma | 6% | 5% |

| Real Estate | 12% | 12% |

| Rnewables | 8% | 7% |

Feedback welcome. Since i’m not yet 30, the goal is obviously to create a long term alpha, beating indices and getting financial freedom