hi,

I have been investing since couple of years and introduced to ValuePickr by one of my friend. Impressed with the amount of work that individuals are carrying in this forum. I am working currently in full time job and been semi active in the valuepickr discussions. I have been trying to build a strong portfolio for long term. Please go through below and share your suggestions.

I have setup SIPs for my financial goals and have been buying shares directly with whatever money left and the plan is to move to direct equity once I get to comfortable levels. Though I am not reducing the amount of money that I am putting in equity and keep it increasing every time there is an increment (so its like another SIP). I buy the shares every month with this amount and not been in with cash any of the time. During the demonetization I deployed some more capital to buy shares which I got as a bonus.

When I started I used to buy companies on some news and then sell it for a small amount of profit or book loss. Some of the companies where I made profit are Cadila (bought when it got FDI warning and sold after one year as results are not improving - should have been a long term hold), Vedanta, Hindalco (both being cyclical in nature bought at the bottom of the price but sold early as I am not in a stage to understand cyclical business) , Chamanlal(sold early due to not much information available publicly, may be a mistake), Bandhan Bank (sold on listing due to high valuations & Ujjivan is already been in PF), Caplin(should have kept this and sold Granules instead as valuations are too high for caplin), CMI(not happy with promoter actions), Finotex chemicals (no bad news but just price was not moving, again a mistake), Kaveri seeds(booked profit after came know about the land issues) .

Companies where I made losses are Welspun India(sold at 50% loss due to Egypt cotton issues forming a no trust on management), Suzlon Energy(one of the early shares I bought as it used to be highest volume trade at that time), National fittings (again not much info available public and bought at a price which doesn’t have margin of safety). Companies where I made neither loss nor profit are HMVL (not happy with the management in deploying the cash they have), Byke Hospitality (showing good growth but felt it might be able to sustain the competition from other online players), Waterbase( management not walking the talk but share price increased so much after I sold but no regrets), Take solutions (again good business but not happy that promoters are not able to divest scm business which they are saying they will since long time - may be I should have kept it more?)

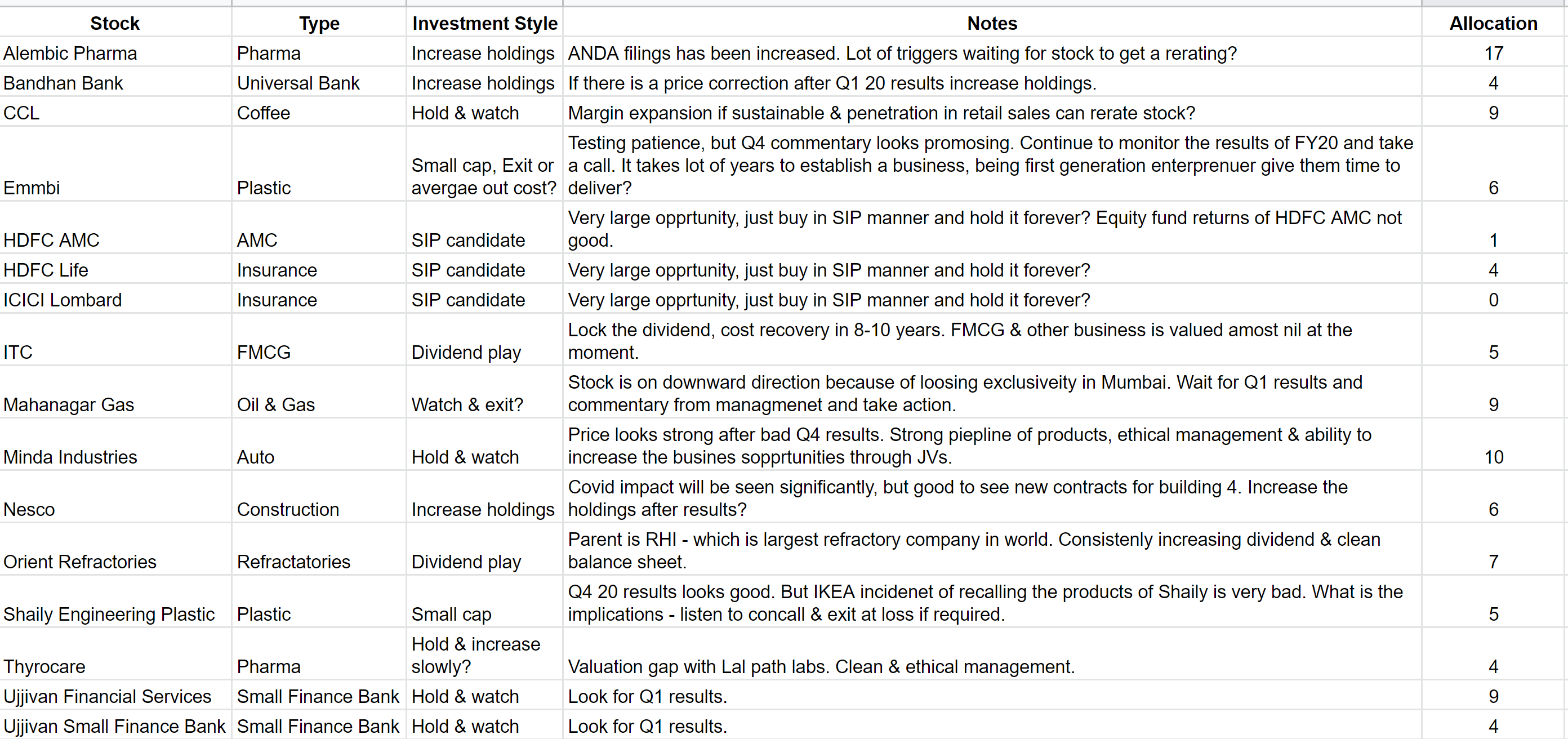

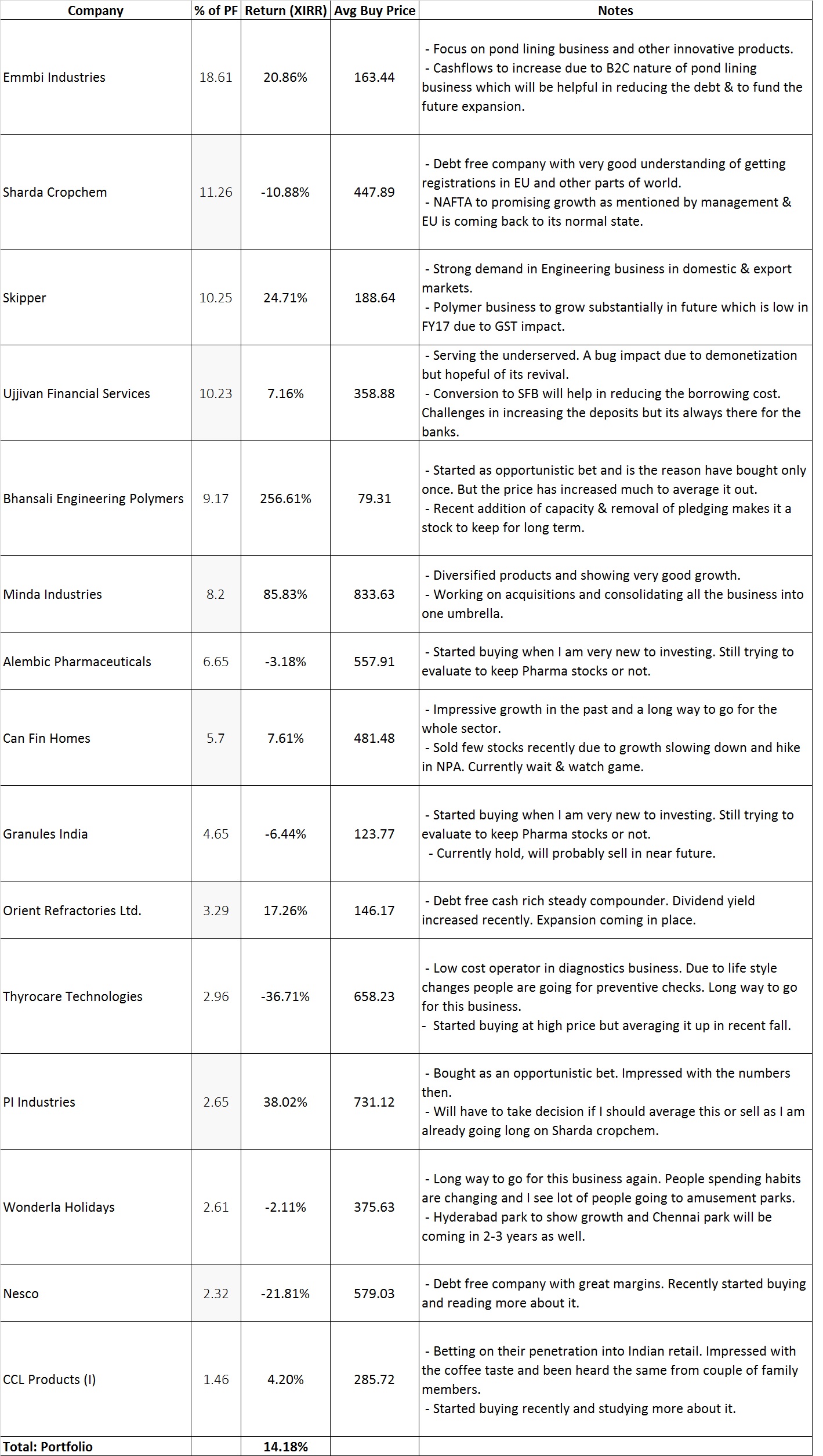

Below is the current portfolio. Preference is given to management quality which are growing consistently and have long way to go in the business.

Goal is to increase the holdings in companies like Thyrocare/Wonderla/Nesco/CCL etc. while reducing/completely sell Granules. I have to decide for PI/Alembic whether to hold for long term as they already proven business. Increase the holdings in Ujjivan/Skipper/Bhansali/Minda depending on their results and future plans. For Emmbi/Sharda I have to figure out if they are long term sustainability business and so take action depending on the outcome.

Please share your views on the portfolio, my approach to stock investing, what additional parameters I should be looking before taking a call etc.

I will update the thread with more details on what books I am currently reading and portfolio allocation strategy , what companies are in watch list etc. soon.