RAMCO SYSTEM

HUGE BREAK THROUGH AND A KEY REVERSAL ON THE WAY . TECHNICALLY GETTING ENOUGH EVIDENCE OF TURNAROUND .

NEED SOME INSIGHT ON FUNDAMENTAL GROUNDS

RAMCO SYSTEM

HUGE BREAK THROUGH AND A KEY REVERSAL ON THE WAY . TECHNICALLY GETTING ENOUGH EVIDENCE OF TURNAROUND .

NEED SOME INSIGHT ON FUNDAMENTAL GROUNDS

Hi

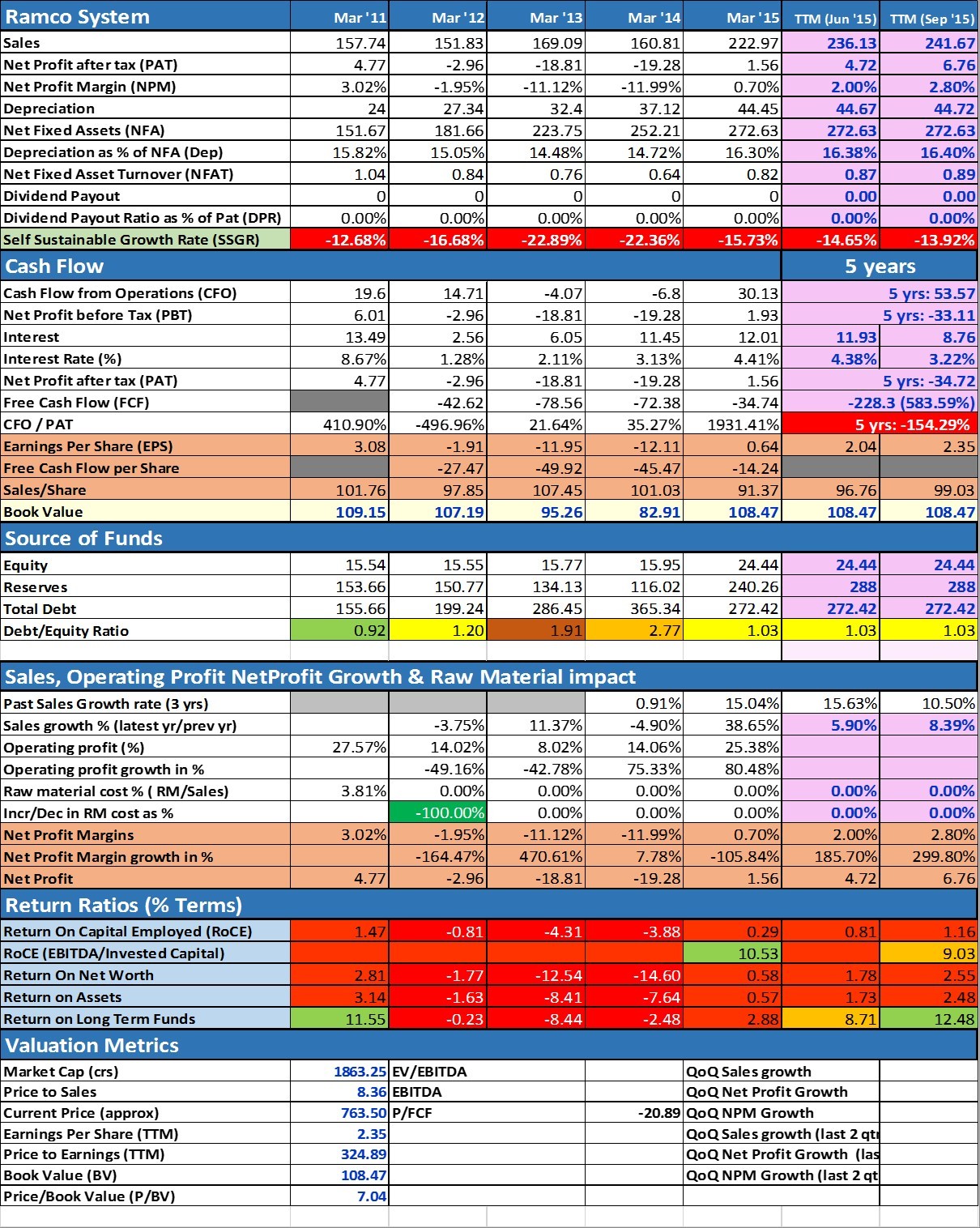

Find attached a report I made on ramco way back in June’14. I spotted the turnaround ahead of others and it’s been 3 x for me and I am holding on tight and will add below Rs. 550/-

Ramco-Systems.docx (28.8 KB)

@ varadharajan superb , recently i came across this stock and even at this juncture i find it is vale bet.

It will be helpful if any one can throw some light on its fundamentals and current valuations

@ varadharajan superb , recently i came across this stock and even at this juncture i find it is vale bet.

It will be helpful if any one can throw some light on its fundamentals and current valuations

Ramco is not only in HCM, its strong forte is its ERP which embeds deep IP a result of many years of R&D and product development.As a matter of fact the Ramco ERP was chosen over SAP for implementation in one very large listed PSU.Product development has always been strong point of Ramco what was missing was the marketing focus that the new CEO has brought to the company.Also with the rights issue so e time back the company is in financially much better shape and last quarter was the first quarter for which it posted decent profits.As this is a turnaround case I expect the momentum to carry through and expect the subsequent quarters also to be good.

Disclosure :invested and am not an analyst.This is not a buy or sell advice.

Technically one must book 10-15% here CMP 880

Or one can trail at 856

Loved every bit of it. Conviction held at 937 bucks too. We might have got what we were craving for. A 3X from hereon too . Isnt it possible ? Just awesome business model. Virendra Agarwal at helm & zero cost product can deliver a lot in coming tyms.Plez share your views.

Ramco systems has impressive list of resellers. I see the giants like Infosys, Dell in the list. In IT the lastest buzzword is “cloud”. Heavy applications (like ERP, Payroll, HCM, etc.,) that used to be run from private data centers are now running on third party / hosted environment and the client companies are just subscribing to the service.

Client companies thus don’t have to worry about maintaining the servers, data centers, security, patches, admins, and several other $$$. Also, companies can subscribe to just what needed and gradually upgrade the service as the company grows.

So, a client company is basically getting rid of Millions of dollars of data center CAPEX. Instead it incurs OPEX on a continuous basis to get all the needed software services. If you want the company to be asset light (looks like the latest requirement to get high PE), then it has to go to all these ready-made / hosted services.

Ramco’s cloud products have riped at the right time when all companies are willing to move towards using cloud services. 5 years back companies were scared of using third party hosted services for ERP, CRM, HCM, Payroll, etc., citing security reasons. But, industry has evolved big time and companies are moving towards using cloud services.

Adobe is making a big switch from Desktop installable Photoshop software to Creative Cloud (CC), the online photoshop which works on monthly/quarterly/yearly subscriptions. And, the client subscriptions numbers which Adobe is getting for CC is very impressive. Its growing at a nice pace.

Workday, Zenefits, Service Now are some of other successful cloud service providers handling company’s sensitive information on cloud.

I feel Ramco has a long way to go.

Disc: Invested in Ramco, and my views might be biased.

More orders flowing in for Ramco’s cloud based solutions:

NelsonHall’s NEAT report identifies Ramco as a Leader for Payroll Outsourcing – http://www.bseindia.com/corporates/anndet_new.aspx?newsid=B48D1F03-0179-41C6-BE87-F4139620CE92

I bought this shares in 2013 after tracking it from 2012, when new ceo is hired from HCL, the day he joined the Ramco, the very first task he did was he sent mail to all the sales team, only very few replied. Ceo sent mail to HR guy stating to firing of all the team who didn’t replied. That seriousness made me to buy this company. Also the group of people from Google, Singapore visited Ramco system and they are amazed by their products this again increased my confidence. CEO told that Ramco lazy work culture and lack of marketing dented the growth which is now visible of CEO walk the talk with series of orders won with New Ceo, Right issue was made @ 150 to retire part debt and use rest for marketing. The story has yet play long with operating leverage kicker

Happy investing to all investors.

Disc : invested since 2013 mid.

Mahesh

Yet another stellar results from Ramco Systems. More details in http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/1885F10E_478C_4EC3_A445_3EB72F8FBF9F_181825.pdf

Discl: invested

Interesting watch. Ramco CEO VA talking about FY16 Target in a HR Meet. Not sure if that was intentional. With Q2FY16 results just released, Half Year FY16 Revenue is USD 32.86 Mn. From his talk, FY16 Target looks like USD 89 Mn. Not sure if this doable by Fy16. But I believe his SAAS model can do wonders, and a nextgen IT company in making.

Some of the Company/HR policies he discussed is path breaking in Indian IT Industry. No wonder Ramco is getting good reviews on Glassdoor. And VA seems to have good flair on the latest technology.

Aah… what a coincidence. I was busy watching the video when i was compiling this post and you raced me in posting the same video

I hold ramco from 150 levels - the key determinant would be how well they do in the US market where they are up against the large guys in this industry - workday, oracle. while they have the advantage of a india developed product, the customer friendliness remains to be seen. Operating leverage is massive in this business and this can go to about 25 % EBITDA at a teen growth. So, if they can do about Rs. 400 Cr. by FY 17 and do a 25 % margin, EBITDA should be about Rs 100 Cr. - so at this level, it looks fairly valued.

Moving the contents to the existing thread:

A Preface before investing in such companies:

Firstly, a primer, I have prepared this notes a few months back while I want to get into the ‘next’ hot sector and see people are going gung ho about the next Infosys.

I have not yet invested in the company and may do so in future depending on relative opportunities available at that time as I cannot stay in cash even for over night after selling an investment. It’s the itch that I have now. This is not a recommendation to buy/sell the company. As indicated, no trades in the past 30 days and will be none in the next 7 days.

You need to be really be sure if you are investing a big part of your portfolio in IT sector, particular if it is thought to be hot. You need to drop it at the first notice of ‘something-is-not-quite-right’ feeling. However, if you get the pick right, you have fair chances of decent gains. Again, do not go overboard with the allocation. ‘Averaging up on management delivery’ might be a better idea. Getting into a stock to find a bigger fool is nothing but accepting that you are a fool in a first place.

Process:

I have started extensive googling and learned about cloud, what lies ahead and the broad direction just enough to get into companies.

Pick and read few companies Annual reports, see the tone of the management, are the targets aggressive, have they achieved it, how are their margins, management interviews, how the company fits into the larger picture etc.

Having done this, typically, a picture will evolve in my mind. I will generally invest based on this broader picture coupled with efficient or evolving financial ratios like better RoEs, margins etc. While metrics, number part a vital role, the qualitative assessment of industry (in my own small way) will finally seal the deal.

Ramco Systems is one company which I was able to focus on because of change in management and the turnaround of the company and the company being ‘product focussed’ but lacked someone at the top who could have a ‘marketing cap’ and drive the organisation. The new CEO Virender Aggarwal is from HCL and is sort of maverick.

Having made my notes, I did not invest because, there are companies which are providing me that earnings growth of 30% consistently and at good valuations, so chose to stick with compounders. “A hen in the hand is worth two in the bush”. I can latch onto these stories as and when such companies become mainstream because there would be still a long way to go and you also would have better probability in choosing a winner as most loser companies would have lost the race long before they enter mainstream. So, I’m ok with losing the initial kicker in returns. Enough of gyan, let’s get into the story.

SAP AG Market Cap: 100 Billion USD.

Now imagine SAP AG on ‘cloud’, whoever takes this market and become a leader can have real big market caps. Can the incumbents do it? Who is the new player who can do it? Can any of the Indian companies do it? The answer to this will require quite a lot of insight.

Simply speaking, SAP provides software product (ERP - Enterprise Resource Planning), basically, a suite of several software applications that cater to the needs to BIG corporations for their end to end business needs, like below, in layman terms:

HR (Payroll, Leave management and all other related functions like a directory of employees with various attributes like phone number, designation etc),

Logistics, Inventory management

Sales and distribution

Production (manufacturing sector) - very crucial for big automobile, industrials

and many more modules covering a gamut of business functions.

SAP AG has customised modules for each industry vertical like Aerospace, Automobile, Healthcare, FMCG, Banking and Insurance etc etc.

Typically medium to large companies go for SAP implementation while smaller companies can implement smaller applications developed by local IT companies who also maintain them.

SAP implementation will provide productive and efficiency benefits as company’s management can have birds eye view of what’s happening, inventory levels, have applications like BI (business intelligence) to get reports from SAP modules for weekly/daily senior management.

To implement SAP in a company is a major decision as it involves CAPEX (but SAP product, Unix, database servers), employee training and it take about 1year to implement in big companies.

SAP products are called “on premise” as companies need UNIX servers, database servers (Oracle etc.) to be PHYSICALLY present in company’s building and managed by dedicated or outsourced IT vendors.

Cloud:

Now, all this will become obsolete, though gradually. Companies will no longer have anything “on premise” but move everything to “cloud”. Simple way to understand cloud is your iPhone’s “cloud drive” for photos where the photos are available in all your connected devices as every photo taken on each device gets stored centrally in Apple servers in California and other global locations and pushed to every other linked device. Cloud is nothing more than this except that at enterprise level it involves complex applications, business processes etc. all done centrally from a single location often called as cloud.

So what now?:

SAP is a bit late in its cloud strategy, as expected (my personal opinion). Any big company will typically gloat in its success that it forgets to keep track of industry changes and also difficult to implement these changes even if it realises early. Just like IBMs of 1980s. Now, to make up to this SAP is buying cloud companies left and right. SAP HANA is answer to this I think and it is envisioned and brought live by Vishal Sikka during his last part of SAP tenure. Vishal Sikka is a visionary who is at a wrong place right now (in Infosys).

There is an Indian company which is in this game!!! “ERP on Cloud” - Ramco Systems. The company is lead by maverick CEO Virender Aggarwal who is recruited from HCL Tech. Ramco Systems is up against giants like SAP, Microsoft etc. but as far as I understand its product is on par. The investment phase is over, now its time to milk the products they have. The operational leverage is simply huge once product gets customer’s acceptance. Market size as you can imagine can be termed a infinite. How efficiently the company can milk the products through efficient marketing and sales is to be seen. The turnaround story, the employee culture within the company, what changes the CEO brought about and all that can be read by googling. The CEO holds 1% stake. Now, everything depends on this 1 guy, so risk of losing him is there. Ramco is particularly strong in HR module, Aviation vertical.

I think Ramco’s game plan would be to target MSME segment while the biggies concentrate on Fortune 100 companies. Ramco entered US market last year, US market is really huge and so is very competitive. IF, a BIG IF, Ramco can break the mould in US markets, then you have a winner at hand, SO, you need to closely track the US story in the quarterly results. Since the company entered recently, the sales expenses (SG&A) as IT companies term them as would be high as the company is in investment phase.

The market cap is around 2000 crore. You can term it as a small cap when compared to the available market opportunity. This has been a 3 bagger in 2 years and may rest here for a while and is current valued at 4 times sales. Typically it can go to 10 times to 20 times as per how its similar global peers trade. But, I think 5-6 times sales a good start if next few quarters show further improvement. I have not done the typical checks like moat, what differentiates Ramco product from others etc.

IoT: There are companies in this space and for me personally difficult to understand which companies will survive this phase and more over I’m finding it difficult to understand this IoT concept, but whoever is in IoT just cannot do away with “cloud” services. So, in a sense Ramco is a pre-requisite for IoT implementation. Just like “internet” and “network” is a pre-requisite for IoT as for things to talk to each other basic things like network, internet, cloud are needed.

I think, for IoT to be a success, a unified language is necessary. Just like Java was needed for “internet” to explode during the last 15 years. For different devices to talk to each other, all devices should be on similar language protocols. I don’t think we are there yet but we surely will be there.

I have tried to explain the story in lay man terms and also in terms of investment thesis, I hope, this might help some who are evaluating the story. Again, read the initial paragraphs of the story. I have read other companies as well but only Persistent Systems impressed me with its consistency and approach. I have not made any notes on this company though. Again, this is not a recommendation.

Happy investing!

The below is the post by @sumi00 carried over by me from the duplicate thread created on Ramco Systems to this existing thread:

thanks for the Great write-up! This one is clearly overvalued at the current market cap. It has been marketed aggressively by some blog sites after some marquee names entered during QIP last year.

One thing that concerns is that it is still investing heavily in products and capitalising the same. I look at annual product development costs that is being capitalised vs. depreciation/amortisation. This is important since these days intangible assets on software side rarely remain valuable more than 5 yrs while Ramco amortises over 10 yrs. This inflates income statement in the near term. It’s own history suggests that previous investments in supply chain turned non-value adding recently. I will be proven wrong if they crack US market big time. Still threat remains that SAP/Oracle can come out with a market leading mini-suite for MSME segment.