First of all thank you to this amazing community, more importantly those honest human beings who are helping newbie’s like me.

I am an mechanical engineer by profession and always interested in financial markets. I made small money in market in last 4-5 years mainly because my bets are always small. I got scared during Covid fall and sold out my entire portfolio. I am on the sidelines for entire 2021 and watching multiple stocks becoming 2X, 5X and some even 10X. This is the biggest lesson of my life. I have leant my lesson now and planning to hold for long term (~10 years) and exit only when there is steady Y-o-Y/Q-o-Q sales/profits decline. For cyclical companies Y-o-Y may be good yard stick where as for others Q-o-Q may be able to tell the story. I am also planning to add as and when I have some surplus money that too on declines.

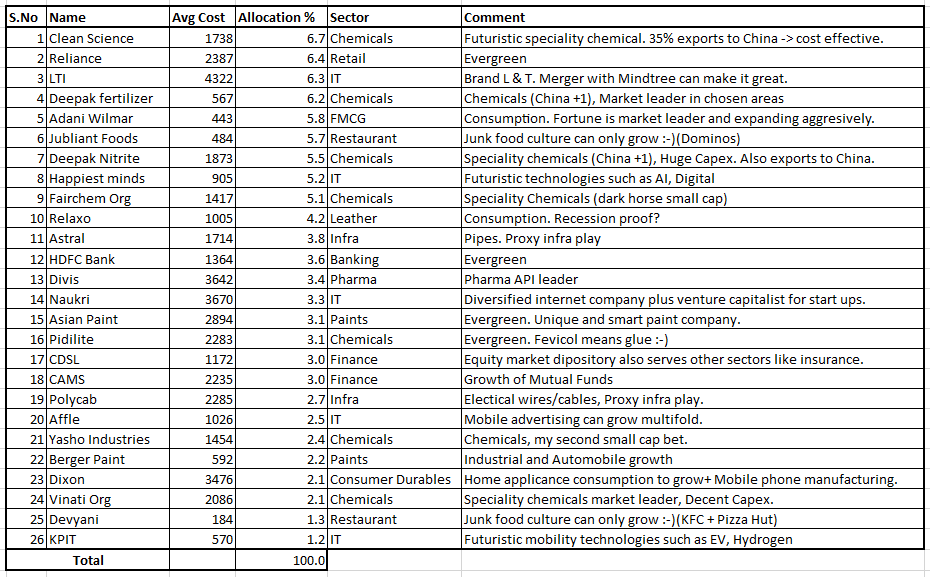

Coming to present scenario, I started buying seriously since start of Ukraine conflict. By July mid I am left with only 10% cash. Here is my portfolio as on 26th August 2022.

I had added quick comments for the stocks and very shortly I shall share my thoughts on why I bought these stocks. Today my Portfolio is with ~15% profit, as usual only top 10 stocks are contributing the most. Below are some details of my portfolio

I have a total of 26 companies as of now.

Chemicals have over weightage of ~30%, followed by IT ~20% and Financials ~10%.

Top 10 holdings had weightage of 57% of total invested value and remaining 16 holdings form the remaining 43%.

Clean science, Fairchem and Yasho are my dark horse bets. I might have taken huge risk here, but have conviction for now to hold on to them

I am an poor orator and excuse if I have any typos. Here are some details about my risky three bets, I shall share my rationale in coming days.

Fairchem Organics

Manufacturer of Oleo chemicals (98%) and Nutraceuticals (2%).

Catering to diversified industries Paints, inks, Soaps, FMCG, Animal feed, Cosmetics, Pharma etc.

Few marquee customers Asian Paints, Huber, Arkema, Cargill, ADM etc.

Continuously expanding capacity hence expected to see jump in revenue & profit.

ROC & ROE are quite healthy 37 & 33.

Healthy OPM of 15-20%.

Debt to Equity is 0.27.

Equity Holding: Promotors 59%, FII 6%, DII 6% and Public 39%

This is one of my dark horse bet, let’s hope this plays out

Clean Science & Technology

A fine and specialty chemical manufacturer. Performance chemicals (70%), Pharma & Agro intermediaries (17%), FMCG chemicals (12%).

Revenue split: China (35%), India (30%), EU (15%), EU (14%) and RoW (6%).

ROC & ROE are quite healthy 46 & 35.

Debt free company.

Equity Holding: Promotors 78.5%, FII 4.5%, DII 4.5% and Public 12.5%

High PE of 77 is biggest negative point but it’s uniqueness compelled me to take my largest bet of my portfolio.

Huge R&D spending and technical edge along with >40% OPM makes it special.

Agree.

Q-o-Q for some companies especially cyclicals may not be a good yard stick. More over I am not going to exit just because one bad quarter. There may some some economic tailwinds which may affect one or two quarters. I could have said "monitor Q-o-Q and Y-o-Y performance regularly and exit where the situation is becoming bad to worse for consecutive Quarters/Years.

Congrats, it is good that you were able to write in 1 line for each stock. It would be good if you can write 1 line as exit condition for each. This will give you clarity.

Just a suggestion, ideally you should have not disclosed exact amount and exact number of shares in each holding. Just % allocation would have been sufficent

I feel, many investors feel some compulsory need to reduce the number of stocks in the portfolio to 10-15-20 instead of 25-30 companies. The most repeated reason given is difficult to track. But in todays world, i think , tracking 30 companies is not a great deal. You need to read 30 annual reports in one year. Initially you may require time but over a period of time, you will know which parts of annual report you need to read, which you can ignore. Quarterly concalls around 30 hours in one quarter and google alerts will make it easy and corporate announcements can be tracked on screener and other news on valuepickr.com, if threads of those companies are available.

Agree with most of your comments.

The reason I was hinting to reduce the number of companies is to get the right % of allocation. Most of the time my portfolio gain/loss is very similar to mid cap index.

I think I should focus on increasing % of allocation where I have relatively more conviction.

True. My self observed lot of HNIs having more than 50+ shares in their portfolio, few i saw 100 where there networth is more than 400cr+, myself when in learning phase had 60 stocks and had 100% profit in 3 yrs including 3stocka with 70%+loss, i think everyone should follow their own style investment and intelligence with patience and controlled emotiona for sure market works for all that don’t make bias until we are patient and less emotional

It’s mostly my gut feeling jokes apart

The Portfolio has a good combination of Large cap heavy weights + Growing Mid Cap (DN ,Vinati,DF, Devyani) & a small caps like fairchem,yasho. Thing to note here is almost 1/3 of the PF is relying on chemicals.

These are some super picks. Would add more financials both Pvt Banks and NBFC, ERD players and retail to this list, though you have covered to a larger extent. I would suggest to focus on quantity goals now and re-read annual reports and attend each calls (both quarterly and publically available ones) of these cos. Good Luck.

Thank you fellow members for comments. Here are my personal learnings and observations in recent times

I am always struggling to hold on to cash. Somehow I get tempted to buy (my watch list stocks) at the very first decline. I guess this is what called FOMO

I am failing to practice “Waiting for the right opportunity” to buy only on considerable declines and key support levels. I know basics of technical analysis and trying to learn more.

I may have to sell companies with less conviction to buy high conviction companies in case of decent correction.

Fortunately I have a habit of deploying cash in small trenches.

Financial companies (NBFC, Housing finance etc.) are harder to understand than manufacturing companies, hence less weightage in my portfolio.

I am sharing my notes for three more companies below. I know this information is available in public domain but helps me reinforce my thoughts/opinion on these companies.

Deepak Fertilizers and Petrochemicals:

A well-diversified leader in Industrial and crop nutrition chemicals.

Largest manufacturer of Nitric Acid and Bentonite Sulphur in India.

ROC & ROE are ~20.

OPM is improving progressively and currently stands at 24%.

Debt to equity is 0.69 which is not bad.

Promotors 47.5%, FII 16%, DII 1.7% and Public 34.8%. FII’s have increased their stakes over last few quarters.

China+1 theme along with Europe gas crisis should create more demand hence higher revenue.

Devyani international Limited:

A quick service restaurant player which operates KFC, Pizza Hut, Costa Coffee and few less known brands such as Vaango and The food street.

Ravi Jaipuria (promoter group) also owns Varun beverages. This is the reason why you find Pepsi (only?) in KFC and Pizza Hut.

ROC & ROE are 16 and 42 which are quite healthy.

OPM is pretty stable and currently stands at 23%.

Debt to equity is 1.83 which is high but this is understandable with aggressive growth plan.

Promotors 63%, FII 7%, DII 6% and Public 24%.

Happiest Minds Technologies:

An IT company works on disruptive technologies such as artificial intelligence, block chain, cloud, digital, internet of things, robotics/drones etc.

Founder Ashok Soota is an inspiration for many leaders in IT industry who severed Mindtree and Wipro in various roles.

Both ROC and ROE are standing at healthy 31.

OPM is pretty stable and currently stands at 25%.

Debt to equity is 0.37. Cash reserves are at healthy ~600 crores and consistently growing.

Promotors 53%, FII 4%, DII 1.5% and Public and others 41%.

Both FII and DII’s have reduce their stakes in recent quarters, is this due to high PE (~77) compared with its peers? However both sales and profit in increasing consistently hence decided to hold on.

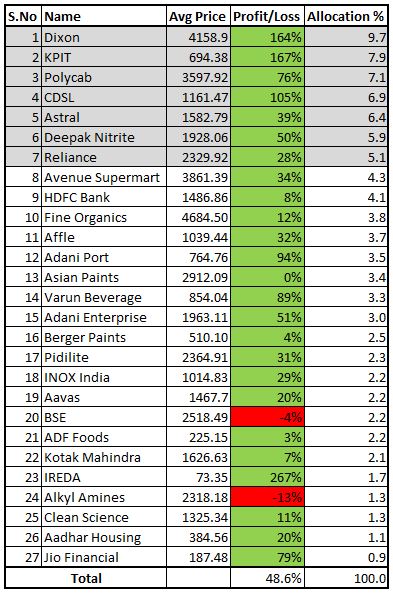

It’s been a good ~10 months since I have updated/commented on my portfolio. I have few quick remarks before I describe my current portfolio.

Hold on to stocks for >1 year need real conviction else very difficult to hold on to your picks, even more so in bear/flattish market.

It’s pain to see your profit erase, especially when this is >70% profit. I have experienced this in Adani Wilmar, Deepak Fertilisers, Fairchem etc. I have hold on to most of my picks despite profit erosion. Let’s hope will be rewarded in the long term.

It’s very difficult to hold on to cyclicals, riding the down wave is the most painful.

I have made few changes to my protfolio including weightage of some holdings.

Exit: Relaxo, CAMS, Vinati, Naukri, Fairchem

Entry: DMART, Adani Enterprises, Adani Ports, Fine Organics, VBL

Here is my latest portfolio

Clean Science 1537(Avg. Cost) 7.0 (% allocation)

Deepak Nitrite 1913 6.3

KPIT 588 5.9

Reliance 2398 5.9

Astral 1354 5.1

Adani Wilmar 429 4.7

Avenue Supermart 3871 4.5

Jubliant Foods 503 4.5

Dixon 3227 4.2

Happiest minds 878 4.2

Affle 1029 4.1

Deepak fertilizer 659 4.1

CDSL 1040 4.0

Fine Organics 4741 3.9

Divis 3470 3.8

Devyani 172 3.7

Polycab 2342 3.7

Asian Paint 2863 3.5

HDFC Bank 1428 3.4

Berger Paint 593 2.6

LTI 4476 2.5

Adani Enterprise 1598 2.4

Pidilite 2294 2.3

Adani Ports 624 1.5

Yasho Industries 1536 1.2

Varun Beverage 560 1.0

At present my top 20 stocks consists of 90% of total value. I am quite comfortable with the no. of stocks. I am regularly following the Qly results, Annual reports and News updates.

From now onwards I shall try to be regular on this thread. Any comments/questions welcome.

you recently added Varun Beverages, are you confortable with its high valuations (high PE)?

FMCG stocks like HUL, Nestle Marico etc are missing. I also dont have them, but since FMCG is a prominent sector in our economy, i wish to add it in my portfolio, what are your views?

What are yoir views about Uno Minda, auto ancillary?

Yes, I have also notice we have quite few companies in common. That gives little extra comfort

Varun Beverages PE is slightly higher, but it’s recently ventured into snacks (chips and other junk foods), which is not so much cyclical like cool drinks. This reduced cyclicality, made me to buy into. I am planning to add if there is any decent correction.

Agree, FMCG to grow with country’s economy but same also applicable for Retail, QSR, Infra, Auto etc. I honestly don’t feel the need to invest in every sector.

I am a mechanical engineer and have started my career with Tata Motors and currently working with Aviation industry. This may be a coincidence that I am not invested in both these sectors. Auto ancillary is going to prosper for sure with economic growth of the country, same applies for other sectors as well.

Here are some notes related to specialty chemical industry trends (from 2023 Annual Report of Clean Science and Technology)

The global specialty chemicals market is projected to register a CAGR of 5.1% during the period of 2023 to 2030.

The Asia-Pacific region has emerged as the dominant market for specialty chemicals, representing the largest proportion of revenue with a share of 48.5% in 2022. Major contributors are China and India.

There is a growing trend in the chemical industry to shift towards ‘green’ or sustainable chemistry, which is expected to register a CAGR of 11.6% from 2022 to 2029.

The Indian specialty chemicals market is expanding rapidly and is estimated to attain a value of ~US$ 64 billion by 2025 (which was ~32 USD in 2020).

With increasing urbanization and growth in the number of middle-income households in the country are further fueling specialty chemicals demand in India.

New entries: Inox india, Aavas, BSE, ADF Foods, Kotak Mahindra Bank, IREDA, Alkyl Amines, Aadhar Housing, Jio Financial

Some highlights:

Now I am able to add/average up in stocks that I have conviction, earlier this was extremely difficult for me.

All my long term holdings (upto S.No:17) have profit in double digits, except Asian Paints, Berger and HDFC Bank.

My Top 7 holdings put together ~50% of my total portfolio.

All my new entrants have weightage ~2%, I can add as I increase my conviction.

Still chemicals have significant portion of my portfolio and the sector as such not out of the woods yet, I decided to wait for recovery.