Been studying this company for last many days. Here are my findings:

Business description

They are a plastic manufacturing company. Create plastic sheets with extrusion then use some of it captively and thermoform the rest into packaging material and products (like plates) for FMCG/QSR/Food delivery and similar industries. They have marquee FMCG clients. Work closely to co-design products. Have 4 manufacturing units in Daman. Machines are imported from Switzerland (more on that later). Their key products are dairy products packaging the kind you find for 500ML curd cups or ice cream cups. They also create recyclable plastic packaging and biodegradable plastic packaging.

Growth

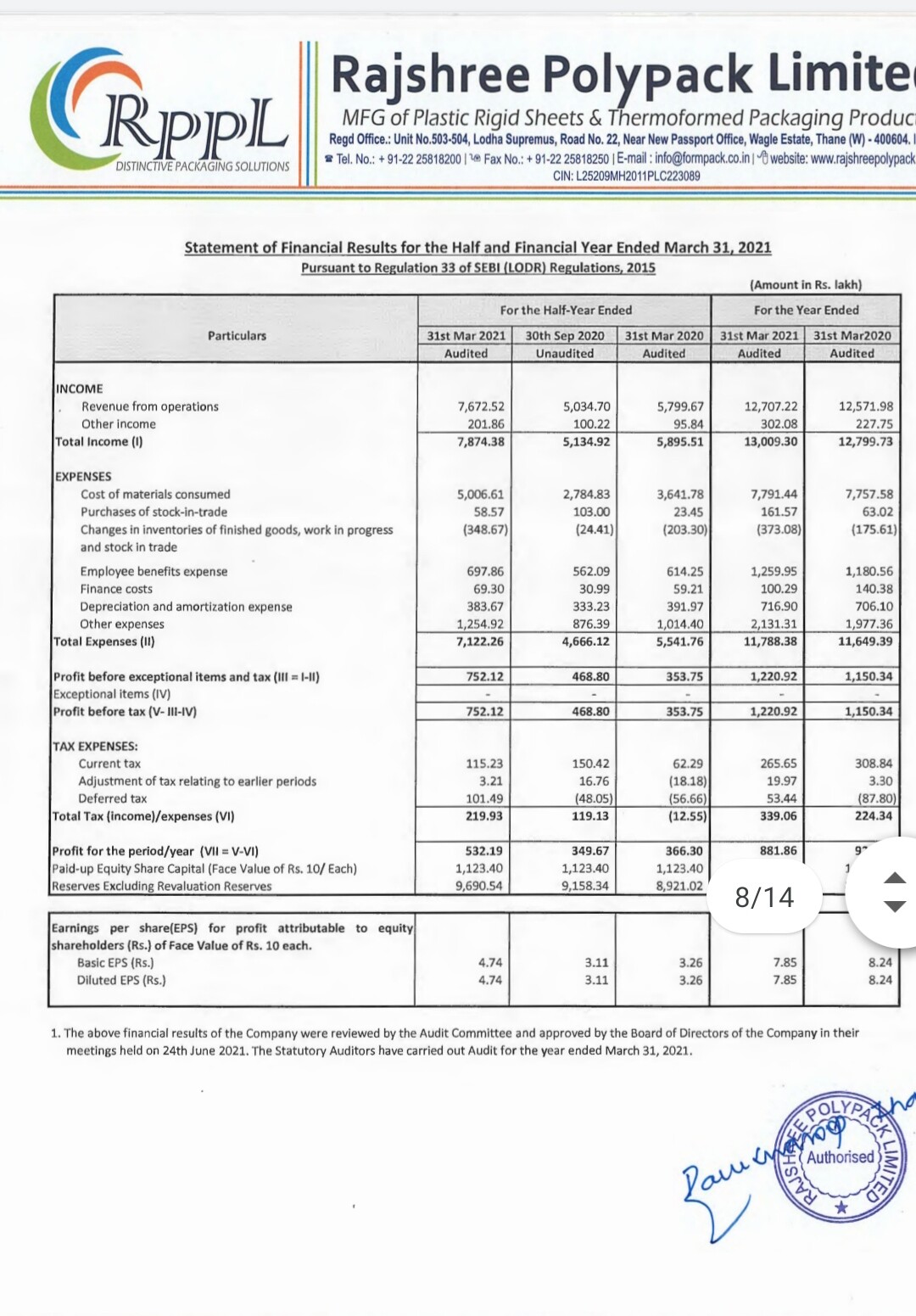

Rajshree grew well between 2015 and 2018 based on previous capacity expansions. They were planning to utilize the IPO proceeds to construct unit 4 roughly by November 2019 end. Then, covid struck and they have been unable to productionize Unit 4 until now (June 9 2021 to be precise). Given that Large (and growing) part of their revenues come from FMCG packaging, it wouldn’t be unreasonable to expect some ramp up in revenues in FY22 and beyond. Key growth drivers would be:

- Capacity utilization ramp up: They were already in talks with several clients to book these capacities since 2018 so i dont think capacity ramp up should be a problem. Also from what I know, capacity ramp up would be reasonably fast once it starts.

- More value added products: They are working on several value added products such as tubes (example: lotions used in cosmetic sector). They are also working on better extrusion machines in order to cater to other sectors (they haven’t mentioned these, although from the DRHP i suspect this might be pharmaceutical packaging).

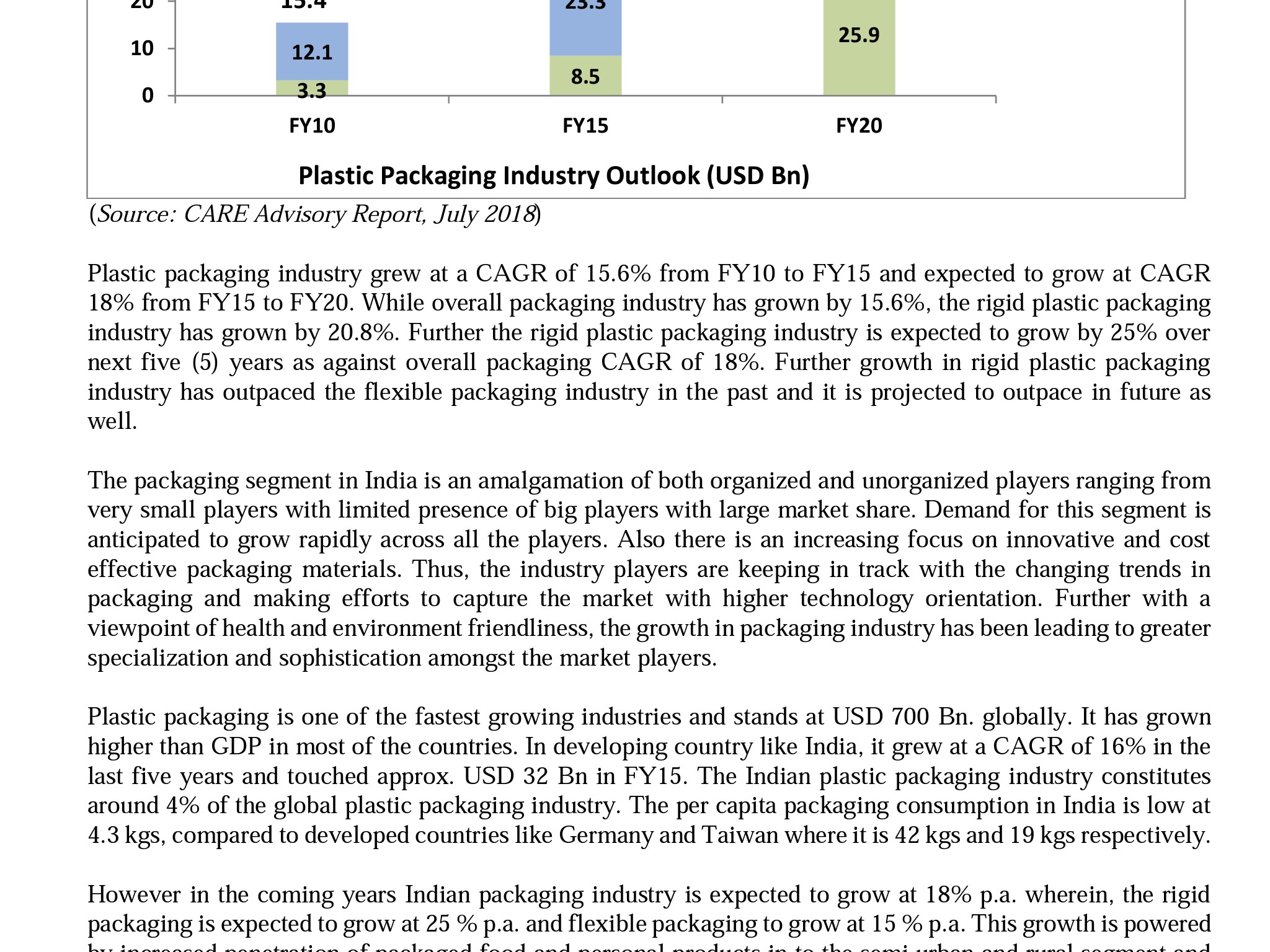

- Industry growth & trends: Rigid packaging industry is growing at 20-25% in India. When industry grows this fast, lot of wealth is generally created, by multiple players. Also, this seems to be a very fragmented industry with not many large indigenous companies. Listening to Mold tek concall, there is a clear focus on hygienic packaging from even SME FMCG players, which would drive demand for organized players like mold tek and rajshree. As industry gets to be dominated by organized players, rajshree can grow faster than industry.

- Barrier packaging: Company is also working on another innovative product called barrier packaging. This sort of packaging enables food to remain fresh and hygienic for longer, enabling indian FMCGs to export to the world packaged foods such as our sweets. Reason i call this innovative is that these cannot be made even on the older swiss machines they had, had to buy a new one to make them.

- Exports: Exports fell during last year as covid hit, shipping costs went up and supply chains were disrupted. However, management wants to focus on exports and wants to penetrate US and UK markets. I dont yet understand how easy or difficult this would prove to be to penetrate these markets but if shipping costs prove to be low (which might very well be the case since plastic is light and can be stacked and packed easily) this might be an optionality which has higher chances of playing out than not.

Profitability

- Scale will drive profitability. 2 years ago, EBITDA/ton in rigid packaging was 30,000/ton and now it is 33,000/ton. Operating leverage will play out as capacities are ramped up.

- The newer products are higher value add and have higher profitability. For example, the tubes for cosmetic segment have 45,000 to 50,000/ton profitability compared to 33,000 for current FMCG products.

- Operating efficiencies would also drive efficiency. Management actively thinks about this. They intend to consolidate Unit 1 and 3 and thus save on labor costs and other fixed costs.

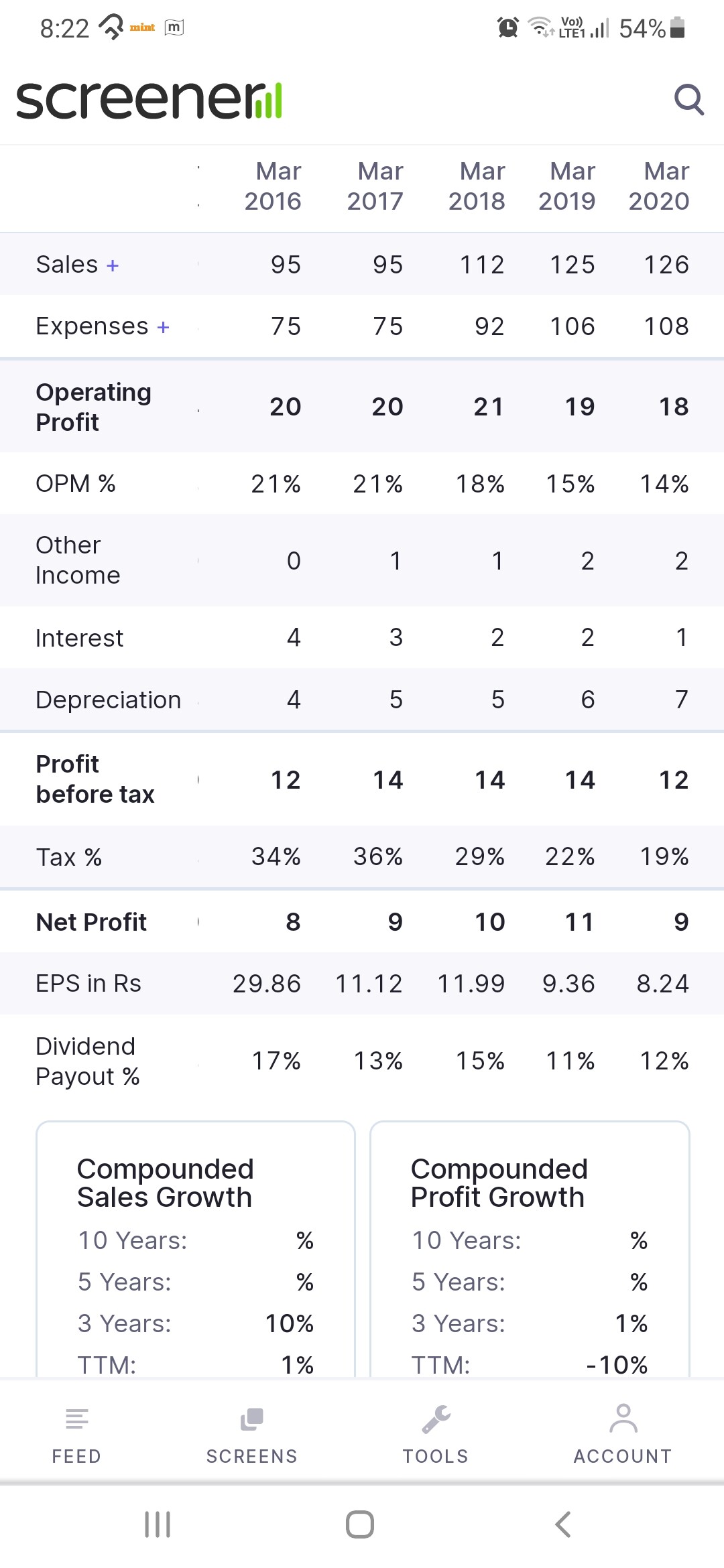

- Key risk here is raw material volatility. They are able to pass on RM prices to customers to some extent, but not fully. My guess is that the extruded plastic sheets might be harder to pass on RM price deltas (but haven’t verified it). Last 3 years, Gross Margins have been in the 38% to 43% range. The interesting thing is that mold tek says in their concalls that they are able to pass on RM increases 100% (although this varies from Q to Q). When mold tek was near rajshree’s scale, their GM were much lower (around 28%) but have been on a steady up trend. This also shows us value-added nature of rajshree’s products. Moldtek’s GM’s are 43% now, and they are 4x larger.

- Unit economics looks healthy and co is able to make 25% ROCE when capacities are ramped up. In general they expect payback period of 3.5 to 4 years for investments.

Key sources of durable competitive advantages

- Clients: it is Difficult to enter supply chains of these FMCG giants like the ones shown:

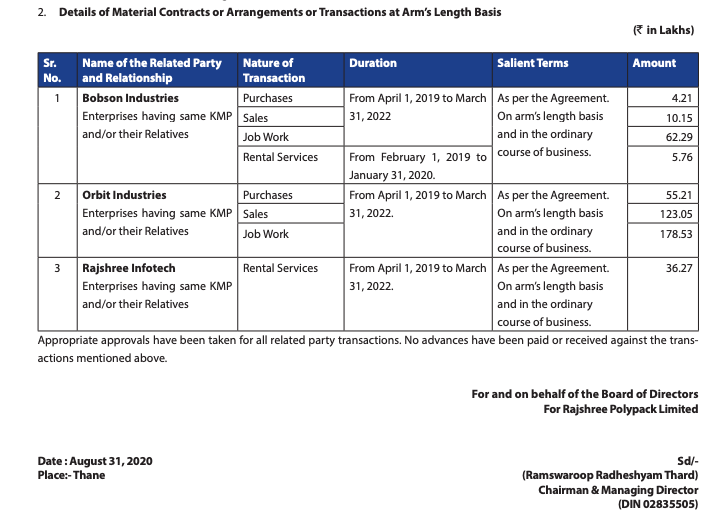

They are very stringent on quality checks and it takes many years to enter these supply chains. Their largest customer has been their customer since 2014. They haven’t lost any major client in last 10 years. These are sticky client relationships. FMCGs are very picky about feel and branding of a product, would not switch for saving on costs (compromising of quality, hygiene) which are negligible wrt end product. Having said that, we should note that these are only 1 quarter contracts with clients, but that seems to be industry norm. However, relationships are far longer and durable.

- Company only uses best quality machines. Their machines are imported from switzerland. They have a very interesting relationship with their swiss machine supplier Wifag‐Polytype who own 20% of the company. This means that wifag is invested in the financial success of Rajshree.

- Company seems eager to innovate. They are ready with biodegradable products (made from corn) and can supply whenever their clients want to move. This will prove to be a very interesting trend. Has already played out in USA. The PLA products are much costliers, and thus would be higher gross margins for rajshree. But the key point is that they are innovative, ahead of the curve: biodegradable packaging, recyclable packaging, barrier packaging, tubes packaging.

Comparison with moldtek

Mold tek is another listed player which is into similar line of business. Mold tek sells packaging for FMCG products which require sturdier packaging (eg: solid boxes) and paint buckets (asian paints) and lubes.

Can one disrupt the other?: Rajshree replies on thermoforming (TF) which is essentially creating sheets of plastic then bending them with heat into desired shape versus mold tek which uses Injection molding (IM) which is about taking small pellets of plastic then injecting them into the mold at high temperature. This para from rajshree drhp makes it seem like TF is superior to IM:

A more neutral sounding comparison makes it seem like both processes have their own pros and cons https://www.thomasnet.com/insights/injection-molding-vs-thermoforming-what-s-the-difference/#:~:text=Injection%20molding%20involves%20injecting%20molten,them%20to%20a%20mold’s%20surface.

The point is, both cos use processes and machines which are very different from each other and have spent years perfecting their processes and gaining experience. Changing tracks and disrupting each other might not be easy. In fact mold tek mentions in their concall that Zomato and swiggy look for flimsy products which they are not providing, and this is exactly where rajshree comes in. I put low probability on the event of mold tek or rajshree stepping on each other’s toes even when they supply to same company. As an example consider baskin robins: the larger sturdier ice cream buckets are supplied by mold tek, the smaller flimsier ice cream cups by rajshree.

Valuations: Mold tek is much higher valued than rajshree and rightly so, they have a much larger track record of execution, have larger scale, more “seen” and thus more widely owned. But my biased opinion at this point is rajshree has equal quality if not more, comparing to mold tek. Besides, as i have explained market is very fragmented (Indian Rigid packaging is a 26B$ market. Global one is 250B$) both can continue to grow for a very long time to come, with direct competition being low probability event in medium term at least.

Quality of business: Rajshree’s client’s business is a higher annuity business (you eat curd every day and ice cream every week) and thus slightly higher quality than mold tek who get largest part of revenue from paints segment, and one only paints their homes once in 5-10 years. On the other hand, mold tek is able to do in mold labelling using robots, which enables them to do interesting things like creating QR codes as a part of manufacturing process. Robots would also result in lower opex. On this front, mold tek is better. On quality of clients, both seem to be tied to me, both have very large established client base.

Another company worth comparing to is EPL if one wants to.

Risks

- Contracts are not long term. Clients can leave whenever they want to, although this is a low probability event given how FMCG supply chains work and given the amount of time and effort both invest into building relationships.

- Company has repeatedly stated that their products are of a much higher thickness than the ones which government has seeked to ban. However, there is always some risk of regulators becoming more aggressive. However, given the deep FMCG supply chain penetration, i expect such regulatory action to be resolved via discussions and product upgradation (higher thickness plastic) rather than loss of revenue.

- All their factories are in Daman. Geographical concentration risk.

- Microcap on SME board. Liquidity risk. Position sizing risk.

A few sample Sources

https://rajshreepolypack.com/wp-content/uploads/customize-upload/H1FY2020-2021.pdf

https://www.rajshreepolypack.com/wp-content/uploads/2018/09/Rajshree-Polypack-Limited_Prospectus.pdf

https://www.rajshreepolypack.com/wp-content/uploads/2018/03/Rajshree-Polypack-Limited-AR-2019-2020.pdf

Disc: Own a small position, might scale up.