Mar 22 results Investor presentation

and link to audio recording of concall (uploaded at 9.15pm yesterday  )

)

Mar 22 results Investor presentation

and link to audio recording of concall (uploaded at 9.15pm yesterday )

Can someone help me with this please…

Or may be I am trying the wrong url. Does someone know what is the correct one?

They have kept a redirect of Thailand website to India website. There may not be a separate website for Thailand.

Yes right. I wrote to the company and they have replied that they do not have a separate website for Thailand.

Results on expected lines. Great on YoY basis but bit lower on QoQ basis. 39% increase in Sales as 58% increase in PAT (YoY). On QoQ basis, sales up 2% whereas PAT dropped 7%. (20% drop if you consider exchange rate impact also)

Commentary of Mr. Sunil Chordia on the results:

"“We have continued from where we left off in FY2022 and have continued to focus on outperforming on

previous benchmarks across all our production, sales, productivity, customer service and performance metrices. 3 key levers namely our recent debottlenecking at our Pithampur plant, our Thailand plant expansion and our upcoming Greenfield capacity at Chennai will also help us to grow at our targeted 20-25% CAGR (in volume terms) over the next 3 to 5 years. We have also taken up digitisation efforts at our Pithampur (India) plant, which will also be replicated for our up coming Chennai plant, this will help our production processes and systems become more efficient and smarter. Our rejection rates have continued to be below 0.02% in India which showcases our commitment to quality. Overall our entire team at Rajratan is geared up to “Outperform” on what we have already achieved”.

The sales volume has decreased Q on Q, but revenue and EBITDA both have increased. I believe this is because of higher realizations (higher RM prices). With softness in the RM prices, we may see impact on revenue and EBITDA. Company has indicated some demand softening in the business of tyre companies because of lower demands from US & Europe. Thus can we see pressure on volume and value in the next quarter?

volume growth will happen because of market share gain. they maintain the ebitda margin. But if steel price softens the topline bottomline will reduce. in q4fy22 concall mgmt told they are sure of 20% volume growth but don’t know about price

https://twitter.com/i/status/1567404147531718662

Rajratan has received Michelin approval. That is the reason for 11% move today.

No disclosure by company to exchange?

They are disclosing directly on TV.

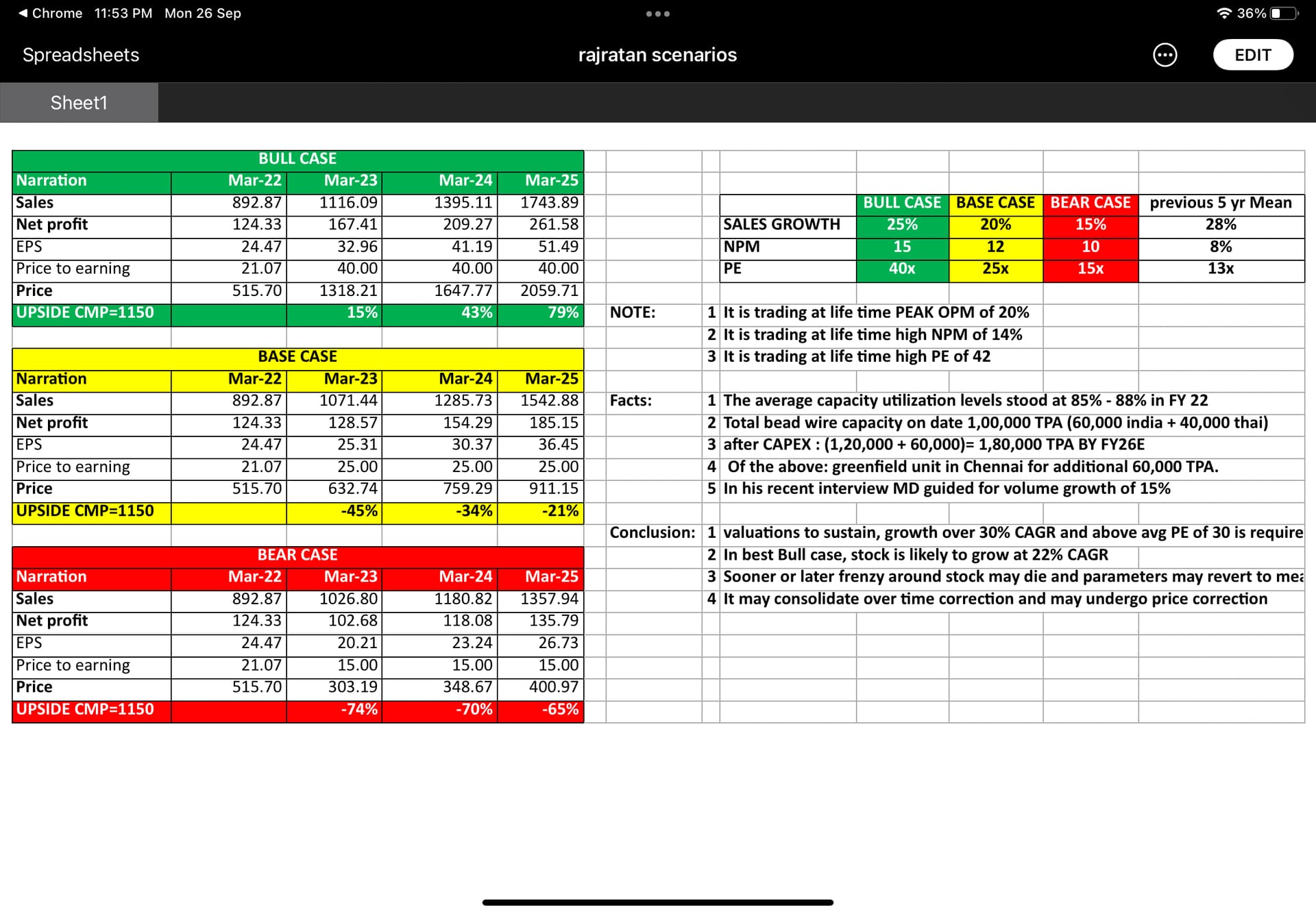

At this point it is trading at PEAK MARGINS, PEAK VALUATIONS. Bull, Base and Bear scenario for perspective is as under

I totally agree with your assessment. However,the Chennai plant will have much better EBITDA/T vs. the MP plant simply due to much lower logistic costs. That needs to be built in. The other source of upside will be export markets especially developed countries like EU/US where shipments will be sent via the port in Chennai. Michelin,etc. are already customers so penetration shouldn’t be very tough.

One other key risk acc to me is realisations. Steel prices most likely won’t sustain at these levels till Fy26 and surely realisations for RR will also fall. Thus,even if there is volume growth the revenue growth will near zero and so will the EBITDA/PAT growth.

Markets have their own ways though. 2 years back people didn’t want to pay even 12-15x for RR,now there is solid strength in the stock even at 42x ttm earnings.

Disc.: sold some months back.

If the volume growth is expected to be 20 to 25 percent, what is the expected revenue growth to be considered if steel prices are falling

Bad results. Sales and profits are down QoQ and YoY. Margin for the quarter impacted mainly due to higher raw material prices. Hope pass through would happen next quarter

Not a correct observation… Cost of input materials (also total cost) are lower compared to both last Qtr & same Qtr last year. Reduction of sales contributed the same in bottom line. I think this is not surprising seeing global economic scenario where company exports to those economies going in tougher time. Hence better result to be expected only when demand rise in the exported economies.

Please consider change in investory as well in your calculation of Margin,

On September 20th , the management told revenue growth to be 15% and was surprised to see de growth in revenue

I think they told about volume growth not about revenue

Conf-call notes.