Stock Split Proposed

5 Likes

Result for Dec Qtr

Conclusion: Ok or Below expectation Results(QoQ)

Results are in line with the expectation… Company is running at 100% capacity and volume growth is not possible till March 2022. Company already said in the last concall that they are running out of capacity so no volume growth till March 22. New capacity of 20000MT is going to come in Thailand from March 22 only and we may see the effect from Jun 22 Qtr. Another capacity of 60000MT is also planned and that is going to come from next year onwards only.

Disc: Invested from lower level

5 Likes

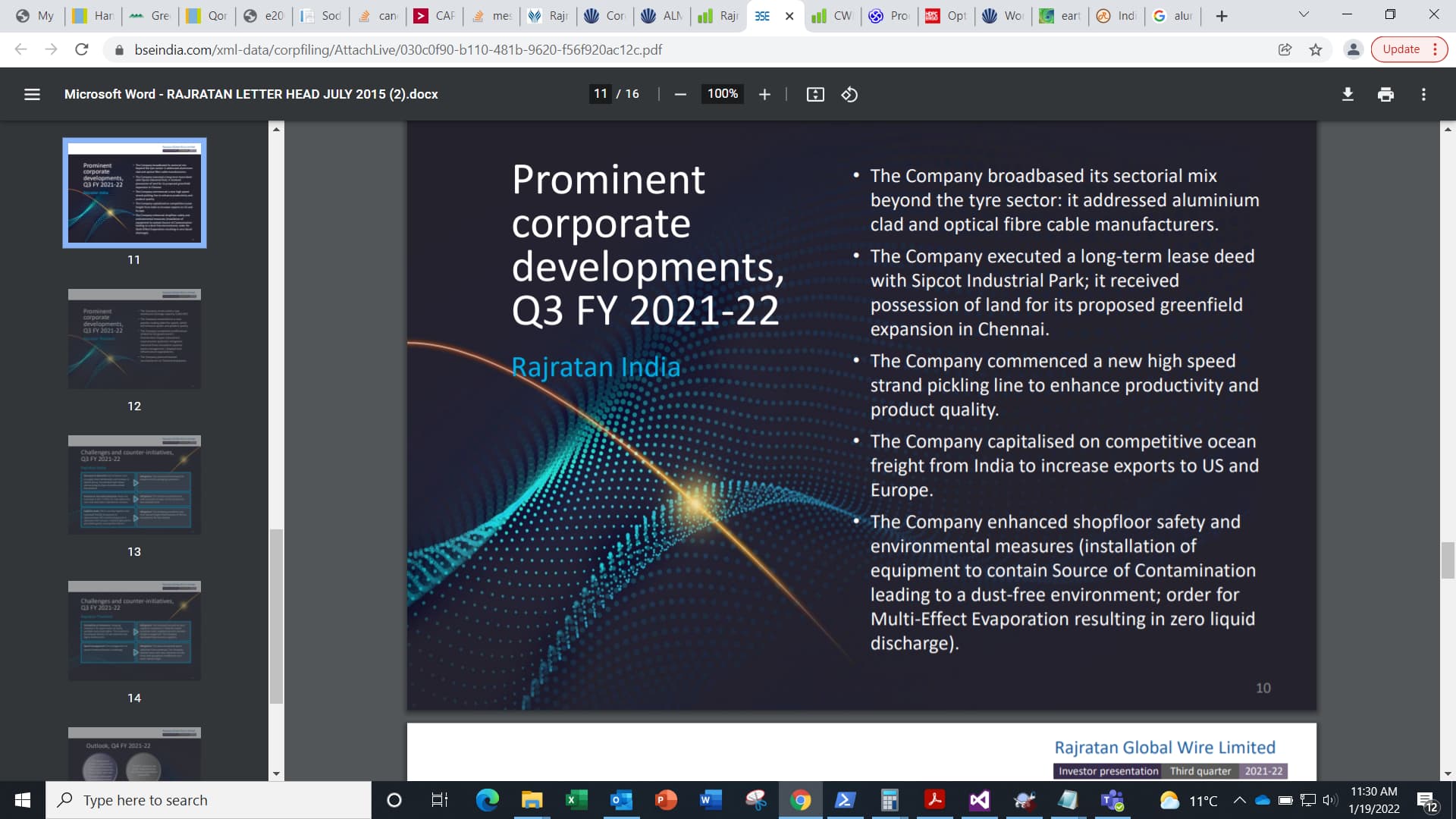

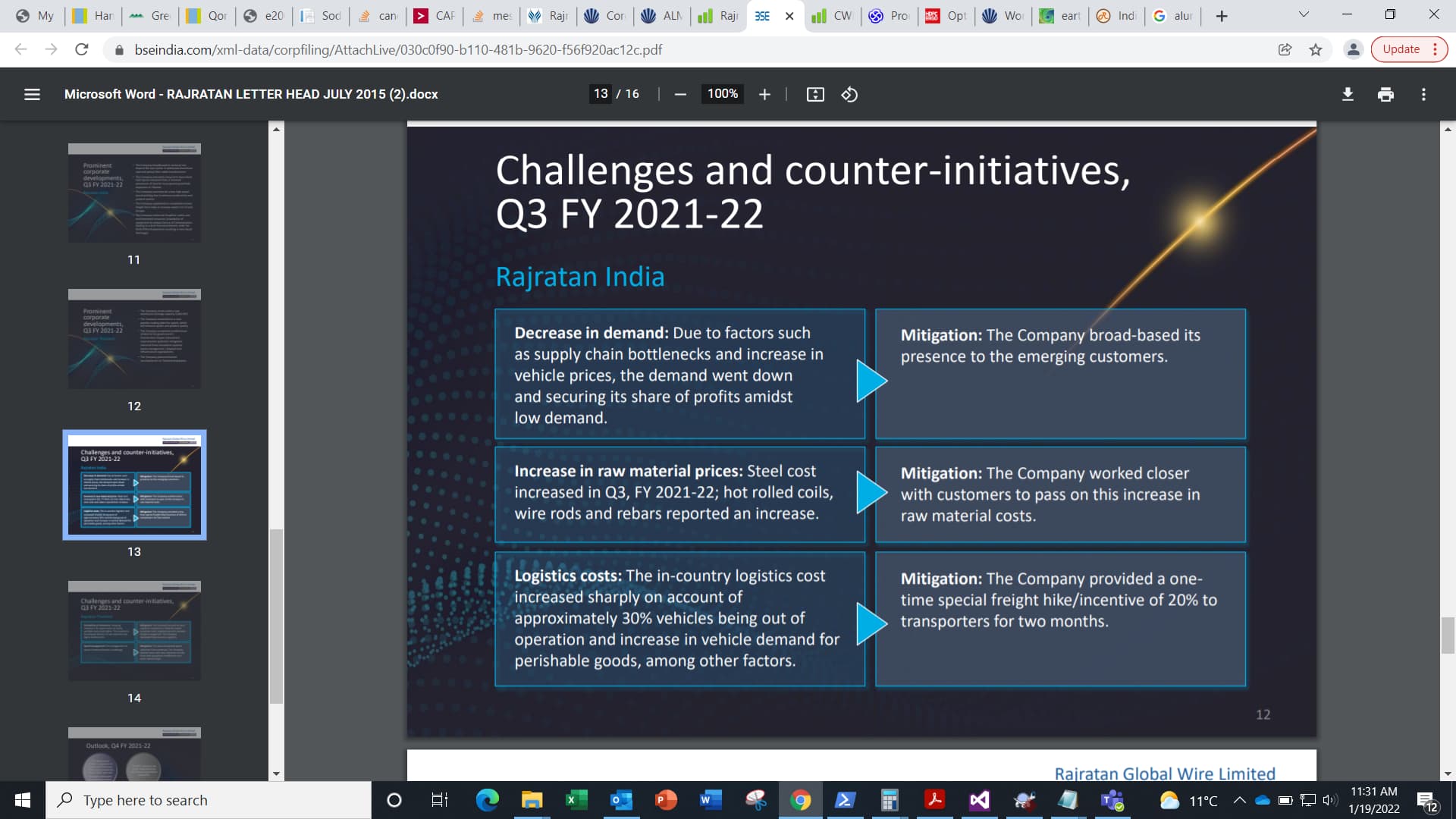

Important takeaways from recent Investor Presentation

Company is trying new sectors

This impacted the profits(small hit)

Source :https://www.bseindia.com/xml-data/corpfiling/AttachLive/030c0f90-b110-481b-9620-f56f920ac12c.pdf

2 Likes

Volume growth has slowed down a lot.They did only 6% growth in Q3 vs. a decent double-digit growth in preceding qtrs. while realisations have continued to be > 100k/MT.Given that tyre cos. did face some rubber related issues this low volume growth can be overlooked.Company continues to clock all-time high EBITDA/T and seems confident of maintaining it.They should have ~120,000 T usable capacity in FY23,mgt expects to sell 112,500 T.The major trigger will be commissioning of the Chennai plant which should happen early next year or end-CY22.Company will save on logisitics cost and will have the ports for their export scale up.

7 Likes

An interesting thing seen in the presentation is that company is looking beyong the tyre sector and now it is also addressing to Aluminium Clad and Optical Fibre cable manufacurer. It will be intresting to see the future plan of the company in these sectors. I think this the first time the company has mentioned these secotors.

10 Likes

It shows company isn’t able to sell. My view is that imports are not impacting company’s performance

1 Like

Loss declared by Ceat Tyres yesterday tell a story about state of affairs at Rajratan’s customers. It seems entire tyre industry is going through tough time and it would impact Rajratan for sure. Need to watch out tyre industry for next 2 quarters.

1 Like

There may be lot of reasons that CEAT posted loss yesterday but this does not indicates that demand for tyres is slowing down. Demand of tyres has to go up and up only. Be it new vehicle tyres or replacement tyres. Many companies are setting up new tyre plants in India. They are sure that there will be demand for tyres in the Indian market and Rajratan is going to be direct beneficiary of that.

Disc: Invested

10 Likes

7 Likes

Leading Indian tyre manufactures (MRF, Apollo Tyres, Bridgestone, Michelin, CEAT and JK Tyres) have committed to invest approximately Rs20,000 crore in greenfield and brownfield expansion facilities in India over the next three years.

Automotive Tyre Manufacturers’ Association

Rajratan going to be direct beneficiary of these expansion.

11 Likes

2 Likes

The amount of net IPA increased from 19.74 crs to 22.92 crs. This increases the yearly amount from 2.82 crs to 3.27 crs

Disc. - Invested

3 Likes

Decent results.

Company is able to maintain PAT QoQ in such inflationary environment shows company’s ability to pass on cost increases quickly.

Also added Mr Sood , Country Head - Aditya Birla Group, Thailand as a director, would be a big plus for their Thailand operation.

4 Likes

This was not a pass on of cost and infact efficiencies kicked in which saved the day. Pass on will help on the margin front even more. Good times here

3 Likes

Very good nos.Volume growth has recovered in Q4 vs. Q3 though most of it was led by Thailand subs.Lower tax rate buoyed PAT.The most amazing aspect about the annual results for me was the significantly improved cash conversion cycle.Company is now at CC days of 50 vs 80 yoy! This has led to a surge in OCF to 120 cr(vs 36 cr) for the full year.At this rate company should be able to fund it’s Chennai capex through internal accruals alone.Realisations in Thailand should improve in coming quarters leading to both revenue growth and some more margin expansion.Company continues to execute very well & improved WC cycle clears indicates a very strong market/competitive position.

8 Likes

I believe this is good company and keep tracking this. One thing I don’t understand is if there is still growth for long term in the market what stopes Tata Steal to expand with CAPEX? As TATA has already a small player in this space who is not expanding its CAPEX. This only explain to me that no big market to expanding or no big money to be made.

1 Like

Thailand part is a moat here for RajRatan

+

The cycle turned just recently when china +1 kicked in. Similar example would be Apl Apollo. Tata steel has never tried to go into Structured pipes. Tata steel is big but they had their own set of problems until recently when the steel commodity cycle turned. That is what stopped Tata Steel from doing more things like structural pipes and beadwire.

Who is stopping Zomato to open its own restaurant in every city they go into? They have all the know howand order history they need to excel. And mind u the food market is super huge and growing in india.

2 Likes

Concall notes

- Very competitive due to lowest cost of production. Feb and Mar cost increase absorbed, will pass on increase in current quarter

- 95% capacity utilization at Thailand. Some debottlenecking in Pithampur plant will help plant utilization (additional furnace), 66,000 tons in fy23

- Pithampur Plant - FY 22 - 50,000T - bead wire. 5,000T - black wire

-Plan for fy 23 - 55,000 tons of bead wire, 10-11,000 T black wire. Black wire capacity will be used post furnace installation - Will sale 20,000 to 25,000 tons more in FY23 as compared to FY22

- Chennai plant - civil work started in April. Machines ordered. Production to begin by March end 2023. 40% exports from Chennai

- Will take 2-3 years to achieve 60,000 Tons.

- Earlier only 20% market share in Thailand, it will go up to 35-40% post expansion. Only bead wire plant in Thailand

- Michelin - Bulk trials are going on . 6-8 months performance trials, destructive testing. Approval by end of FY 23

- Spread was earlier $250/ton, now gone upto $500/ton

- Total planned Capex - 15 cr - debottleneckin in fy22. 300 cr in chennai , 75-80 cr - thailand

- Capex - fy 23 - 25 cr - thailand, chennai - 125 cr

- Loan approved - 100 cr. Mainly will be used in fy23

- Through out the year, we were short of capacity. Hence confident to sell additional 20,000 tons in fy23

- RM mainly from JSW steel. JSW started new plant of 2 MTPA of wire rods

- Indian market size is 120,000 tons including cycle tyres. Rajratan has 45% market share in indian automobile market

- More stringent requirement for tyres of EV. Less noise, more load carrying (battery load), higher tensile strength, without joints

- Extra capacity of 20,000 at Thailand from July 22. Would need 25 additional operators. Operating leverage would help margin improvement

- Rajratan would be no. 2 player globally and would have 18-20% of global capacity post Chennai plant completion (180,000 MTPA capacity)

- Currently not able to supply to cycle tyre manufacturers due to capacity constraints and tyre bead wire is less value added

17 Likes

Chennai plant would be something that would be the next growth trigger. Management is going increase their share for sure. Passing on the cost is not a hassle due to frieght charges if client import from other places. Plus there is a 5-10% differential too.Good times.

3 Likes