Hi all,

I am a new registered user of the ValuePickr forum, but have been going through the various discussion threads for quite some time. I must say this has been a life-changing experience and my whole concept about stock investing has changed ever since I started following ValuePickr.

I had been guilty of picking up the stocks at the exorbitant price (fearing that I might miss the bus) or selling the winners too early in the past. Also to play safe I would keep on adding a large number of stocks to my portfolio with small allocation to each script, which hardly made any impact to the overall portfolio. But after going through the great books recommended by the senior ValuePickr members and also by visiting many threads on the forum, I have been able to instil some discipline in my investments. I have since trimmed down on number of stocks too, bringing it to a manageable level. I would still like to prune the number of stocks even further.

After spending a lot of time I have been able to devise a method that works for me. I have now divided my holdings in to two portfolios:

a) Core portfolio

b) Satellite portfolio

The Core portfolio consists of high quality stocks with proven track record. The investment in these stocks is from long-term perspective (5 years or more). The alteration in portfolio is done only when the fundamentals of a company have undergone some change.

Satellite portfolio mostly consists of the midcap / smallcap stocks which don’t have a proven record but are opportunistic bets.

The allocation of the funds is in the ratio of 70:30. And under no circumstance the Satellite portfolio will have more than 30% investment.

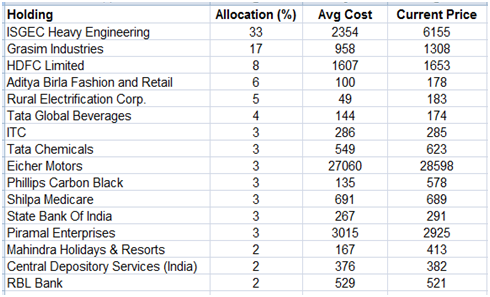

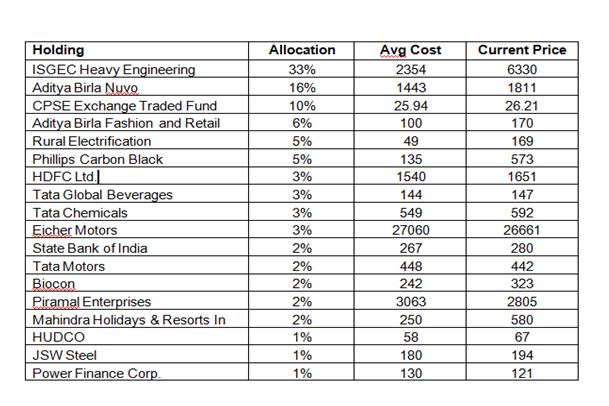

I am giving details of my core portfolio here-under and would request the feedback from the senior members. My rationale for picking up these stocks is also attached. Ideally I would like to restrict myself to 10 stocks, but I am not sure which stocks I should say good-bye to. As mentioned earlier, I have a time horizon of 5 years or more. So, I am not in any kind of hurry. I am comfortable in making regular investment to this portfolio. At the same time I have no problem in putting in lump-sum amount if the opportunity arises.

ISGEC

The company is in to the manufacturing of pressure vessels, heat exchangers and boilers. During the last 10 years the company has shown almost 10x growth in the top-line with very impressive ROCE, which is rarity in the sector. The company has JV with leading players across different segments like Hitachi, ABB, Bosch etc. The company is consistently upgrading its technology and expending its manufacturing facilities to meet the ever-growing order-book. Its newest plant at Rattangarh in Haryana gives ISGEC the capability to manufacture boilers of 100-1000 MW capacity. The company is sitting on a huge pile of free cash. The sugar division had been a drag for last many years, but now slowly that business has also started showing improvement. All in all, ISGEC has been a wealth-creator for me.

Aditya Birla Nuvo

A diversified business with a huge potential of value unlocking. The market value of the investment is more than company’s market cap. The company has got the license for the payment bank which can be the game-changer for them.

CPSE Exchange Traded Fund

The idea was to have the quality PSU stocks in the portfolio to give stability to the portfolio and get rich dividend without having to keep a track of 10 individual stocks. I would like to hear the views of masters whether this strategy is right.

Aditya Birla Fashion and Retail

ABFRL hosts India’s largest fashion network with over 7,000 points of sale across 375 cities and towns, which include more than 2,000 exclusive ABFRL brand outlets. The company has now made an entry into men’s innerwear and multi-purpose wear - a market that is growing at 13-14 per cent a year.

Van Heusen multipurpose collection, including vests, tees, shorts, track pants, joggers and travel pants, is also attractively priced and comes with smart tech features such as quick dry, stain release, anti-stat, colour fresh, soft smoothness, all-day fresh; making the crossover between fitness and fashion. Also the fact that the innerwear range will be made available across leading departmental stores and e-commerce site should give ABFRL a real boost.

Indian Toners & Developers

The company is in to the manufacturing of toner and printer cartridges along with the toner powder. A debt-free company that has a ROCE of 30% for last 10 years. The company has now shifted the focus from exports to the domestic market, which should boost both top-line and bottom-line growths.

Rural Electrification Corporation

Invested in REC since its IPO and the stock has been a star performer over the years with regular dividend. The 1:1 bonus last year was just icing on the cake. I would continue to hold and add to the stock as an alternative to putting the money in the fixed deposit.

Biocon

Biocon is a global provider of innovative biopharma products and engages itself in all phases of the product cycle, from discovering to development and then commercialising the same drugs. The company is poised for global impact with biosimilar insulins and antibodies target of $1 billion in sales by FY19.The company is expecting to roll out its first ever biosimilar in US market in FY19, which will be a game-changer.

Phillips Carbon Black

The company is in to the manufacturing of Carbon Black domestically. Carbon black is a major reinforcing filler used in tyres and other rubber products.

Carbon black can be manufactured using two different processes, which either use coal tar or crude derivative i.e. carbon black feedstock (CBFS) as a raw material. Post a decline in crude prices, manufacturing of carbon black using CBFS has gained traction, which benefits Indian players. To safe-guard the interest of domestic players, GOI has imposed an anti dumping duty on imports of carbon black from China into India till 2020. PCBL stands to gain substantially as it is the leading player among a small set of domestic players. The stock has given more than 375% return in last one year.

HDFC Ltd.

Market leader HDFC has been delivering healthy growth in retail loans, steady margins, and very low delinquencies despite the slowing property demand. The pace of loan growth for HDFC has slowed in the last two years, in line with the overall trend in the sector, but it has still managed to outpace the industry. In the last five years, HDFC’s retail loan book has grown at a rate at least 5 percentage points above banks’ growth in this segment. The company’s leadership position in the housing finance market, a predominantly first-home buyer and salaried class target segment, negligible exposure to the riskier loan against property (LAP) segment and sound fundamentals should continue to hold it in good stead.

The merger of Max Life and HDFC Life is on the cards. Any future unlocking from HDFC’s other insurance subsidiaries will also be a trigger for the stock.

Tata Global Beverages

For long TGB has been a laggard often testing the patience, but the stock is finally making some positive moves. The management is working aggressively in making Tetley a billion-dollar brand in next three years. The company had recently launched a few premium tea (mostly herbal and functional) and has garnered one percent of total tea market in the UK and about 5% of tea market in Canada… It has also entered large tea-drinking markets such as China via the e-commerce route in partnership with Alibaba. The management is also taking steps to cut-down on underperforming assets; the China JV that has been struggling for a few years is in the process of being sold. Starbucks performance reflects good growth with lower losses due to better instore performance and higher number of stores.

Tata Chemicals

Tata Chemicals, another Tata group company, is engaged in manufacturing of chemicals, salt and fertilisers. It also sells pulses and spices under Tata Sampann brand. The firm is also into water purifier business. Tata Chemicals is the world’s second largest producer of soda ash — with footprints in the US, Africa, the UK and India, through its subsidiaries.

Tata Chemicals has also been working on its nutritional and dietary supplements or neutraceuticals business to boost growth. It has launched a low calorie sweetener named Tata Nx.

Tata Chemicals will see most of its growth from three areas– specialty silica, consumer business (including neutraceuticals), and the agri-inputs subsidiary Rallis India Limited.

The sale of the urea business indicates that the management wishes to reduce dependence on commoditised businesses where the pricing power is low while growing the share of value-added products such as speciality chemicals.

Tata Motors

Tata Motors owns iconic brands Jaguar and Land Rover, while offering a broad product line of motor vehicles including micro-compact cars, sport utility vehicles, luxury passenger vehicles and large semi trucks. It holds the largest market share of commercial vehicles in India. It should gain from an upswing in government spending on infrastructure and the long-term growth potential for light commercial vehicles.

Going forward, Tata Motors should do well as JLR profitability will improve on the back of:

-Strong product cycle. Land Rover will recover in FY18 with the launch of new Discovery & Velar

-Long term benefit of modular strategy - more models on fewer platforms (from 11 models on six platforms to 17 models on four platforms) will reduce cost

-Ramp up in China JV

-New production capacity in Slovakia. The company will launch its electric vehicle I-Pace in CY18.

State Bank of India

Largest lender of the country, SBI will see the stock getting re-rated once SBI Life is listed. Also the new insolvency and bankruptcy code gives them teeth to deal with the NPA more efficiently.

Piramal Enterprises

Betting on Mr Ajay Piramal’s business acumen that has established PEL as one of the largest, reputed and profitable NBFCs. 54% of PEL’s revenue came from Healthcare and 46% from financial services in 2016-17. However, going further the financial services business should do better. Slowly but surely PEL has opened a huge space for it where it is funding the entire chain of operations from land purchase to construction to leasing commercial properties while banks are busy in dealing with NPAs.

Mahindra Holidays & Resorts

The concept of vacation ownership has taken a while, but MHRIL is finally on track after years of sideways movements. Riding on a strong brand name and expected pick-up in the economy, MHRIL should do well going forward. Membership additions in India have been healthy and profit has grown at a strong pace. Also, the planned additions to the room inventory and integration with the foreign subsidiary should boost prospects.

Eicher Motors

With a PE of 47 the stock looks expensive, but Eicher has a knack of springing surprises year after year. The company has a consistent profit growth of 48% for last 5 years, while average ROCE for last 10 years is 47%. The company has built a moat around the brand, which is unlikely to go away anytime soon.

HUDCO

Got a small allotment in the IPO. Haven’t gone in to much details.

JSW steels

A very small portion of the portfolio allocated to the metals. May add more if the stock goes down by 20%

Power Finance Corp.

Have added the stock just a few days back. The stock has lost around 20% from the highs of 160 mostly on the NPA concerns.

.Shall get out once I see it retracting from these levels.

.Shall get out once I see it retracting from these levels.