Thank you so much @rajeesh_jegadeesan for such a detail responce. But duopoly is a real threat in this industry. Are you aware about Jio renting or leasing towers from Indus towers or they have their own or any other players. Like Bharti airtel have their own I guess.

You’re welcome @Chirayu_Shah

Reliance Jio employs a mixed strategy for its tower infrastructure, utilizing both leased and owned towers.

Tower Leasing Agreements

- Indus Towers: Jio has signed significant leasing agreements with Indus Towers, which is one of the largest telecom tower companies in India. As per recent reports, Jio is leasing around 14,000 towers from Indus, benefiting from discounts based on its tenancy status

- GTL Infrastructure: Jio is leasing around 6,000 towers from GTL without any special discounts

- ATC (American Tower Corporation): Approximately 5,000 towers are leased from ATC, where Jio receives a 12.5% rebate due to occupying vacant slots

Bharti Airtel: Airtel has its own tower assets and also leases from Indus Towers. Airtel holds a significant stake in Indus and continues to expand its infrastructure independently, while also benefiting from shared resources

Jio’s strategy of leasing towers allows for rapid expansion without the need for extensive capital investment in infrastructure. This approach contrasts with Airtel’s model, which includes a larger focus on owning assets. Overall, Jio’s reliance on both leased and owned towers positions it effectively within the competitive landscape of Indian telecommunications

Its not Nifty , Its Gold which has become the best performing asset from last Diwali to this Diwali

If you take into account of physical gold, 1 tola of 24k physical gold was 63316, now its climbing up to 81290

So the physical gold gives a return of 35% returns beats Nifty handsomely YoY.

The RBI is also racking up gold like crazy, something is fishy.

1 Like

Sold off Trent and Infosys and added Motilal Oswal Financial services and KPIT Tech.

Motilal Oswal - Rationale - In a Sweetspot to take advantage of boom in wealthy indians and Broking as stock demat accounts reach sky high. It caters to the investment rationale of taking advantage of K shaped recovery in India

KPIT Tech -Rationale- It caters to the investment rationale of taking advantage of falling rupee and booming EV ecosystem across the world. It has a stronger project pipeline than Infosys. Pretty much it has given a huge run up but just now got a chance to offload a giant like Infosys and switch to KPIT as it has recently facing brunt of demand slowdown due to Chinese players entry and off shoring in Europe. However, it seems to be minor blip even the management has not reduced its guidance. It has gone to post 17th consecutive quarter on quarter growth. Better to be part of the journey on a longer term

2 Likes

Taking singles and doubles in the market now, not sure with market’s direction with multiple important events on the line for this week, I dont want to jump the gun and go invest right away. Though my SIP day is on 15th…

Bought 1 share of KPIT @ 1418 and 1 share of Tata motors @ 833

Bought on the second rationale - Taking advantage of falling rupee.

Tata motors juicy portion of business comes from Jaguar Landrover and it has become debt free and with the type of distress multiple automobile players are going through, Tata motors has the sweet spot to have all the components of what makes an EV. They have Steel player in Tata steel, Software player in TCS and Tata tech & Tata Elxsi, Automobile plants, Access Wide brand name and market, Debt free balance sheet and cash reserves.

Singles and doubles day

Bought 10 shares of Manappuram Finance at 153 and 1 share of Tata motors @ 829

Unsure what market is trying to do here, Manappuram have taken adequate steps to mitigate the Microfinance Debacle. Even with that their Q2 results are indeed impressive at an AuM of Rs.45600 Cr and estimates beating results, the scrip is still going down. May be the SEBI ban needs to be lifted I suppose for their Ashirvad subsidiary. And Gold prices are going down with Trump’s victory, good time to accumulate Manappuram

Similar Singles and Doubles day

Bought 1 share of Manappuram @ 153

1 share of LT foods

2 shares of ITC

2 shares of Tata Motors

And Proudly Announcing the switch which i made worked out like a charm. I sold off Trent and Entered Motilal Oswal. Trent is on a downward trajectory and Motilal is up 7%. Very well!!!

This thread is going to be very boring as I’m just doubling down on convicted picks and known not so hidden value stocks with not more than 2k per day for investing instead of going All in one go

Same Case Today too. Bought,

2 Shares of Tata motors

1 Share Dr Reddy’s

I kind of know that Tata motors is going to go down further but no one knows how much and I pretty much see value in it at this rate. So With conviction I’m placing my bet on Tata motors. This makes my tally to 75!!!

I am also very very bullish on rupee devaluation and Dr Reddy’s being Export driven company gets more Earnings on Dollar. And Indian Inflation is as per Govt. is 5.81% but overall actual inflation is more than 12% and Medical Inflation is so elastic which makes Dr Reddy’s very highly valuable in India as well. And I dont know how people are neglecting it. For a 1 lakh crore Mcap company, Its growing at a breaking neck speed.

This is the Basic EPS of Dr.Reddy’s (Latest in first). I feel it being Very Very attractive, Its oversold, historically PE is near lowest!!!

Closely watching Musk’s actions on Starlink introduction in India based on which I will take a call on Indus Towers and Bharti Airtel. But bit confused as Birla is thinking of infusing fresh capital into Vodafone Idea, which is like an indicator on Telecom market is here to stay and I dont want to jump the gun.

And I’m excited to get 100 more shares of NMDC from my Naked Trader Satellite portfolio!! Taken by Bit of a surprise

Bought 3 shares Tata motors at 784!!!

And officially my Portfolio entered into Red zone after holding the FII onslaught for Oct & Nov till date.

Still sticking to the same strategy, bought couple of shares Tata motors, Natco Pharma and Manappuram!!!

Keep a close eye on Manappuram, the business might picked up by Coup through Bain Capital. They’re eyeing majority stake through PE and OFS. If it happens and when they sort out the issues in Ashirvad Microfinance, it is going to blast when the market reverses.

Still sticking to same investment rationale, Investing on companies which can benefit out of falling rupee and eye on long term dollar earning businesses. Which has a converse rationale that will impact gold as an asset as well.

This is my current PF situation, Not in deep red but still, some of the holdings like Bharti Airtel, Indus towers, Zomato, United spirits, Dr Reddys, Zaggle, Samhi hotels, Natco Pharma, LT Foods are showing incredible resistance to the fall and these are the stocks which is acting as a decent hedge so far!!!

Wonder what is going to hold up in future ![]()

![]() (Below screenshot Just to show that I’m not bluffing, 10 1/2 months into the year, 10 1/2 lakhs in investment)

(Below screenshot Just to show that I’m not bluffing, 10 1/2 months into the year, 10 1/2 lakhs in investment)

1 Like

Following up for Dec month:

Let’s plan

Dec is a FII’s off day - for the year (assuming they’re from western world). So the selling pressures are historically lower and with inflowing SIPs, markets will go higher is my educated guess

So, using this opportunity I’m planning to offload some stocks from my satellite portfolio and core portfolio (Not necessarily multiple, just the indus towers, I’m really weighing my options here)

Happy about my portfolio’s resiliency though I’m just about matching the Nifty.

Now, what am I investing for the month…

6 month gym membership for 7k

1 certification on CSM ( Just broadening my skillsets)

60k for MF ( 1 flexicap, contra, small cap and gold)

45 k on GARP strategy.

Wrt GARP strategy, I am planning to rebalance my satellite portfolio MoM based on the famous GARP methodology but just focusing on making it a Indian version with help of Trendlyne

A fundamental screener was available, I was just tweaking it and playing with it

So these are the metrics and methodology

1. Valuation Metrics

- Price-to-Book Value (P/B) < 4: The stock’s market price is less than four times its book value, indicating it’s reasonably valued relative to its net assets.

- Price-to-Earnings (P/E) < 25: Ensures the stock is not overly expensive in terms of earnings, yet greater than 0 to avoid unprofitable companies.

- PEG Ratio > 0 and < 1: Reflects undervaluation relative to growth, indicating the company is growing faster than its valuation suggests.

2. Profitability Metrics

- ROCE (Return on Capital Employed) > 15% (Annual and 3-Year Avg): Ensures consistent profitability and efficient use of capital over time.

- ROE (Return on Equity) > 15%: Highlights strong returns for shareholders, reflecting operational efficiency.

3. Growth Metrics

- Revenue 2-Year Growth > 10%: Indicates steady revenue growth over a medium-term horizon.

- YoY Revenue Growth > 5%: Confirms consistent growth in sales over the last year.

- EPS TTM Growth > 5%: Ensures earnings per share have been increasing.

- Cash EPS 3-Year Growth > 15%: Reflects strong cash flow-driven earnings growth.

4. Market Strength and Financial Health

- Market Capitalization > 500 (Crores): Targets established companies with significant size.

- RSI > 50: Indicates bullish momentum, suggesting upward price movement.

- Debt and Profitability: Ensures operating profits (Operating Profit TTM - Tax TTM) exceed financing activities, suggesting good cash management.

5. Valuation Based on Cash Earnings

- (Current Price / Cash EPS Annual) < 30: Ensures the stock is reasonably priced relative to cash earnings.

Summary

This screening formula is tailored to identify high-quality growth stocks that are:

- Profitably and efficiently using capital.

- Growing revenues and earnings consistently.

- Reasonably priced relative to their growth potential and financial strength.

- Exhibiting bullish market sentiment.

Right now this screener gives the below stocks

- KNR Con

- PFC

- Motilal Oswal

- UTI AMC

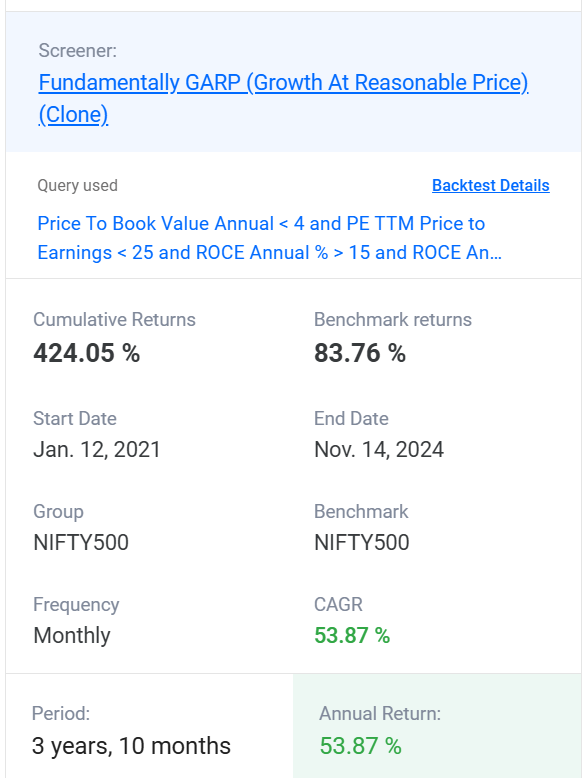

I have backtested it. And below are the results

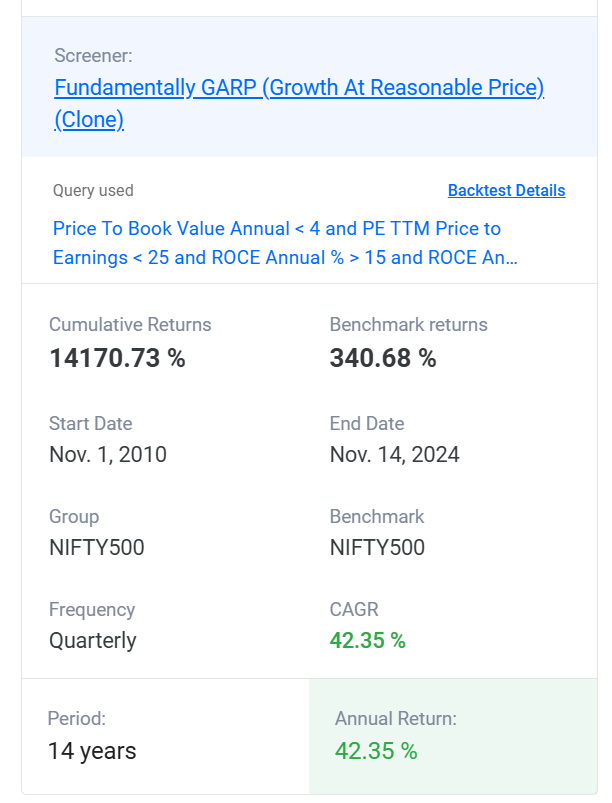

Now the holygrail of backtests

I’m not batting for the strategy blindly, It does has its low period as well. To make most of this strategy, one need to go really really really long term.

If one has to understand why 43% CAGR over 14 years mean is, If you invest 1000 one time in this strategy with a 43% CAGR over 14 years, you would receive approximately 149,522 at the end of the period

4 Likes

Hello Everyone,

I have gone ahead and did the portfolio investments. Since the Nifty is reaching its immediate support and we are almost closing out the month, I am investing today.

I have couple of new entries. But Let’s go step by step

CSM certification - Completed at Rs.15000 / 2 year

Gym membership - Rs. 7k / 6 months

SIP

20k - Helios Multicap Mutual fund

15k - HDFC Gold fund

15k - SBI contra fund

10k - Quant Small cap

Equity:

3 X Nuvama Wealth @ Rs.6800

2 X Dr. Reddy @ Rs.1325

50X Goldbees @ Rs.63

60XITBees @ 48.22

6XITC @ Rs.467

2XLT Foods @ Rs.419

80 X Pharmabees @ Rs.80

5 X Samhi @ Rs.202

120 X South Indian Bank @ Rs.25

4X Tata motors @ Rs.743

2X United Spirits @ Rs.1573

2XZaggle @ Rs.533

I’m still sticking to the same rationale. I strongly believe that there is a K Shaped recovery in India and the fall in Rupee is going to be consistent (Its fallen to Rs.85/USD spot price)

So most of the stock SIPs are either catering to ultra rich customers, value investing (stocks trading at lower value than its peers or stocks which have been beaten down for no good reason) and the instruments which will work with the dollar appreciation.

With respect to portfolio:

I have reinvested my dividends and profit back to stocks, Right now portfolio is withstanding the onslaught of FII selling. GARP strategy stocks are also present which is steely resilient. GARP stocks in my portfolio right now are as per screener,

- Natco pharma

- UTI AMC

- Motilal Oswal

- Jindal Saw

- Manappuram

- KNR Con

Investment summary this year

Equity + ETF: Rs.12 lakh

Mutual fund: Rs.1.8 Lakh

Gold; Rs.2.2 lakh (bought 37 gms at avg 6000 per gram)

Cash: Rs.20000

PF: Rs.84000

Investment in Dad’s equity portfolio: 1.5 Lakhs

Portfolio exits: Electrosteel castings

Portfolio Additions: Pharmabees, IT Bees, Goldbees, South Indian Bank, Nuvama Wealth

2 Likes

Hello Everyone,

I have done the most of my investments for the month. Wanted to post the monthly update

PowerBI PL300 certification - Registered at Rs.5000 and free renewals for the year.

(I’m still preparing for the exam though)

SIP

20k - Helios Multicap Mutual fund

15k - HDFC Gold fund

15k - SBI contra fund

10k - Quant Small cap

Equity:

I’m still sticking to the same rationale. Wealth distribution is incredibly skewed and the fall in Rupee is going to be consistent. Incredibly fallen into Rs.86/ territory which is not going to stop soon. The situation is so bad that RBI is mulling for Rupee-to-Rupee transactions from NRIs and with Donald Trump adding more strength via tariffs, H1B visas and upcoming rate cuts by RBI aint going to help improvement in rupee value as well

Sticking to this rationale makes my investment boring but I have already made mistakes in investing in Jio financial services (I was being too cocky on its prospects, and I really don’t believe it has in it in a widely, intensely competitive financial services market). And more credit loans are being disbursed, savings are lowest at all time levels. CDS is encouraged by banks to be added in portfolio. Banks are suffering with very poor CASA ratio. It clearly shows microfinance, NBFC and banks are going to have more pain ahead.

You might think then why am I investing in South Indian bank and Karnataka Bank. It has fallen below book value, and it is purely a value buy

I have also exited Tata steel which is also facing so much pain. Both Jio and Tata steel are having too high valuations. Not the greatest of times to own such stocks

With respect to portfolio,

Portfolio additions: Investments in Samhi, Manappuram, Dr.Reddys, Zaggle, Tata motors and South Indian Bank and reallocated some of the invested amount in Indus towers into Dr.Reddy’s.

ITC hotels are also going to be listed out soon. I got credited with 18 shares which i know will plunge at the onset of listing, I’m not planning to sell it either

Will split another 30000 and continue investments in Tata motors, Karnataka Bank, Indus towers, Dr.Reddy’s and Goldbees for the month of January

But due to loss harvesting the PF has shrunk by few pp and Portfolio is in red now, down by 0.5%

Big Bets are in Pharma stocks - Natco Pharma, Dr.Reddys, Value stocks in Tata Motors, ITC, Motilal Oswal Services & Gold

Portfolio exits: Tata Steel & Jio financial services

Hi,

If you are going to follow Ruppee deprication, Gold funds are best. If Nifty dips further to 22000, Gold funds are going to outperform almost all small cap funds for next year or two.

You can also invest in USA etfs like Motilal Nasdaq.

In Indian stocks, they will fall with the market whether earning in forex or not as almost all companies hedge their forex rates.

My 2 cents. Please do your own diligence.

Cheers

1 Like

I want to track down my portfolio Big Bet companies for their QoQ performance. Let’s Start. Markets are so much in punishing mood, even a good result doesn’t matter at this moment is what I can understand.

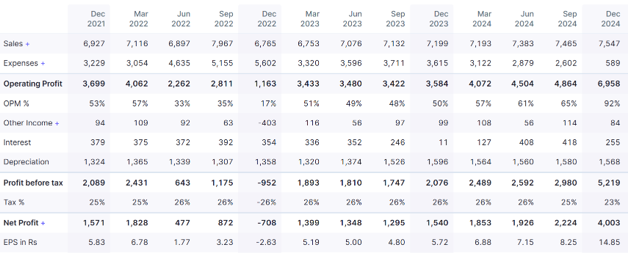

Dr.Reddy’s

So the revenue is up, Margin is up, tripled their R&D expenses and their PAT is down by 5%.

Now, a pharma company missing analyst estimates because of R&D expenses is very contradictory. The same analysts are going to punish the company if they don’t innovate. It’s good that Dr.Reddy’s took the punishment

No immediate impact from Trump. Europe market sales has grown by 52%

Very minimal debt. The new drugs / therapy include Nicotine replacement therapy, HIV Treatment drug, 2 cancer treatment drugs. They have expanded their API facility at Bollaram too

Now a company having a good sales growth, profit growth, with almost nil Debt, ROE, ROCE growth with a good pipeline releases results on increased expenses on R&D. and What happens?

Down by 12% , I’ll take all this with both of my hands with a mouth watering P/E, it’s a steal for long term

Next up Indus towers

Very similar case, the sales have remained more or less stagnant but a killer move from Vodafone where they have made a stake sale and reduced their debt which Indus towers had provisioned last half. Which had exploded the Net profit.

The EPS have been tripled YOY. But the stock moved nowhere. So, Good time to invest again at low P/E

Indus Towers is conducting pilots to assess the technical feasibility of the EV charging business, and its ability to deploy more charging stations. A pilot in this regard is already underway in Gurugram and Bengaluru.

Also the FII holdings are increasing. FII/FPI have increased holdings from 24.19% to 26.15% in Dec 2024 qtr. which is A fun fact where in a market FII are exiting a rapid pace. Promoters released all pledges in Dec 2024 qtr. Mutual Funds have increased holdings from 12.96% to 13.32% in Dec 2024 qtr.

Vanguard have entered in the stock, unlike MSCI index last year. Vanguard have gone full blown where they have entered with all their funds. Societe Generale, Morgan Stanley, Blackstone, NPS has also invested this quarter.

But stock has moved no where!!!

A 1 Lakh crore market cap company with a growing topline, bottomline attracting foreign investors (in a market where FIIs are selling), with no debt and a PE of 9.7, do you need more reasons to have it in consideration set?

It has also withered Elon Musk scare this quarter as well, though it is a long term threat.

Gold on a other hand, on the backdrop of weakening rupee, consistent demand, strengthening dollar have been going up & up & up.

Is at an all time high. It is just a matter of time, with an upcoming rate cut by new RBI chief, it’s a matter of time per gram rate is going to cross Rs.10000

Let’s wait and watch.

Our long term strategy is clear, moving towards in the direction of Cheaply valued growing companies and hedging against dropping rupee by investing in gold and gold finance companies like Manappuram which have also exploded from Rs.150 not so long ago to Rs.200 thanks to rising gold prices and removal of bans on Ashirvad microfinance