This is my first post here. Regret getting to know about this platform late.

I am a novice investor.

This is the first stock I picked up and have done a bit of research.

It would be great if all of you can share your inputs (criticism is much appreciated).

Introduction:

Rajapalaym Mills is the mother company of the Ramco group. The company makes quality yarn; counts from 4’s to 300’s and it has always incremented capacity to produce value added yarns like Compact, Elitwist, Slub, Gazzed yarn in singles and doubles among others.

Company’s performance:

During the last 5 years, the company has reported modest growth of 5.3% in operating revenues deriving 25-30% of its revenues from exports.

The company posted its best ratios in last 5 years in H1 FY 17 with RoE of 14.9%, RoCE of 13% and RoIC of 10.4%.

The company’s has been consistent in repayment of long term loans evident from Rs. 404 Cr in 2011 & 277 Cr.in 2016 and is poised to be free of long term debt by 2021.

Goes with the Management:

Competency - The Management has decades of experience and has established a brand name in the spinning industry. Debt repayment - It has been paying off long term loans as per the repayment schedule . Infact, they have been paying off more amount as required in the schedule. This shows the serious attitude to run the business unlike many other companies. Loan from Directors - The loan taken from the Chairman/MD are at average interest rates of 7.1/8.3% (last 5 years) which is in line/cheaper than loans taken from any financial institutions.

Goes against the Management:

Managing Director’s Remuneration - The remuneration paid to the MD as a % of Net profit for the last 5 years is ranging from 2.2% - 11.2%which is quite wide. A reputed peer listed company pays in range of 2.5-3.5%. Promoter’s share holding - The promoter’s have pledged 28.05% of their holding which is not a good sign. The intent needs to be checked and the time frame for the release will also need to be assessed. Related party transactions - There are a number of such transactions - the intent and the requirement needs to be assessed.

Interesting insights:

Capital Allocation - Business segments:

Surprisingly the company’s capital allocation is an area of concern. It allocates on average 80% of its capital in the textile business butthe windmill business has been generating higher return on capital - 15-20% and also contributing 50-60% of the company’s PBIT. Also contributing to this is the fact that there has been a growth in Income per lakh KwH generated has gone up by 9.3% CAGR over the last 5 years showing an uptrend in tariff rates. The company’s future allocations will be on the radar to see if it has any strategies in place for further growth justifying the deploy of capital.

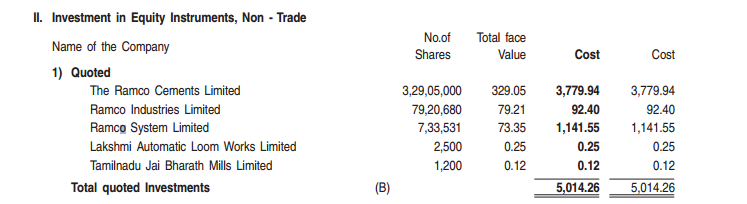

Stake in Ramco cements worth Rs. 3000 per share:

It has a 13.8% stake in Ramco cements with a market value of around Rs. 1750 Cr. along with stakes in other group companies implying a discount of around 80% to the company’s current market price.

Statistics

The correlation between share prices of Ramco cements and Rajapalayam Mills in the last 5.5 years has been 0.65 and in the last 3.2 years has been a strong 0.91.

I do not understand what justifies the 80% discount to the market value of the investments.

Also I request the experts to please share your views on how can I improve my analysing skills based on the above analysis. @hitesh2710 Please share your views.

Since all these companies are well known and the individual companies have their own boards as well, there is a very small chance of value unlocking. Though the value of each share means a very big sum of money, the ownership pattern itself doesn’t warrant a gratification of that sum at some point of time.

I feel if this parent is dissolved and the value realized by selling the holding shares at open market levels to public, then the money can be made, if not a huge dividend payout by selling stock can also be another option, but since all of the group companies are listed, I find no justification as such

The basic question rush158/Rushabh has asked is whether value unlocking is possible, and short answer may be - its difficult. There are quite a few such examples in Indian market, where holding companies are trading at huge discount (50%+) as its very very difficult to unlock value by realizing gains of market prices of their holdings. Few examples that comes to mind are - Tata Investment Corp and Bombay Burmah.

However, in this particular case of Rajapalayam Mills, two things are notable: One- the holding company has its own business and two- theoretical value of its holding is almost five times of the market cap ( 400Crs mkt cap vs 2000Crs market value of holding).

Thus, the question boils down to this - what is the intrinsic value of the yarn business and what is the value of the “holding company”. One way to look at current situation is that market has given a zero value to the yarn business and holding company is trading at 80% discount. If one thinks that Yarn business has a certain value, and/or holding company discount will reduce (perfectly possible- recent re-rating of Bombay Burmah) then there’s some value in this script.

I appreciate all your insights.

I had the same query if there was a possibility of a value unlocking here, if anybody had any update for this company. But even leaving the investment in ramco cement, the company has a Brand name in the fine count yarn market.

The current textile scenario should see many mills in the south close down and it could benefit from lower cotton prices in the coming years and aid margins.

Expecting sops for this sector in the Budget.

And sorry for asking a basic question what’s the reason market discounts so much for holding companies ? Only because the value is not unlocked or is there anything else ?

Perhaps anyone could give insights on its valuation - whether it is under/fair/overvalued currently? @paresh.sarjani1@suns@ketand

Now for Rajapalayam mills all the numbers have changed …

Consolidated EPS:-RS.196

Cons. Book value:-Rs.2000

Value of investment:-Rs.3500 cr

Current Mcap:-Rs.900 cr

Big Question is Does the minority share holders gets Justice??

Now in the current market correction this stock has fallen quite a lot and the current market cap is around 420 crores.there are various factors contributing to it like the primary business is suffering also the underlying share values have decreased due to market correction.Seems like a good value buy at these levels.when overall business improves,the share should increase.Anyone monitoring the stock or invested kindly provide guidance.

Mcap - 540 cr.

Yearly sales - 850 cr.

Market value of investments ~ 2700 cr.

I was following this company from past few years purely as a holding company which has not played out from value unlocking perspective. However, my view has changed a bit because of following -

Company has done a huge capex in last 2 years to add capacity and modernize current machinery. To give a context -

Total capex = approx. current market cap.

They have used a bit of their holding company shares (sold some ramco cements ~ 90 cr. and some rights issue). In their AGM they mentioned that they intend to buy back Ramco cements again. Broadly to me the holding acts as a cushion and as long as they are used for investing in their own business - one should worry less. Should watch out for ROCE for next couple of years. I have started seeing it as not a value unlocking play but a separate cash generating company with additional cushion from investments.

3.This is one of the few companies I could find where sales is on constant rise maintaining the margin.

You can read more about in their ARs and AGMs (last 3 years videos are on youtube)

I am unsure of the future demand - There can be China + 1, pakistan +1 etc. but sales numbers are encouraging . Very vaguely - considering the capex they have done - operating leverage can help drive margin to higher values.

Cotton is their main raw material which shot up after COVID but has now reverted to mean -

From a holding company discount they are currently at 80% discount which is on the higher side and if you believe in cement cycle (boradly sales rise but profitab. impacted due to coal prices) Ramco cements is the second most efficient cement producer in India.

All in all its a classic value play and has less downside. If earnings come we can see PE and EPS increase.

View invited.

Disc. - Bought tracking quantity today.

I dont think its too high but yes it is indeed eating away the profit. This usually happens when you do huge capex by external debt. Textile in general is a capex heavy business and return could be subdued for long. Here they have taken external debt + rights + selling some Ramco cements.

I agree with you - debt number should be observed carefully.

Holding co taking leverage on their own standalone business is a very big trigger. Its not just a core investment co to be valued at 70-80% discount now.

Capex done in textile business in last 5 years is 800-900crs as per crisil. 500-600crs in last 2 years of which 60% is already contracted with buyers. Exports to Japan market which is very tough to crack.

Investment of 2600crs in Ramco cement shares. Best way to play Ramco cement shares.

Focus is on value added yarns like mercerized yarn and now forms 20% of topline. Focus on Value-add creates value.

Decent group and no major corporate governance issues. Should unlock value for minority shareholders if it wants to. Rajapalayam Mills was the first business of Ramco group.

Can get good terms from bankers since common group borrowing. Has 75-80% of the power requirement own sources.

Triggers going forward and some crystal ball gazing:

Consolidation of Ramco group’s textile business into 1 or organizational restructuring to better focus on the textile business. Simplification of shareholding structure of the group can also unlock value here.

New CEO appointment since current CEO is aged.

Textile sector tailwinds with UK FTA.

Sale of Ramco cement shares where they have got approval (they instead purchased shares of Ramco recently).

Ramp-up of fabrics unit and operating leverage.

Issues:

No focus yet from the Ramco group.

Corporate guarantees given to unlisted promoter groups (provided some total 60-70crs of guarantee)

Instead of board approval to sell Ramco shares, they have recently purchased it.

Huge capex done recently which can be negative if Industry doesn’t improve. Additionally, Ramco cement is on capex spree as well.

Labour related issues.

Textiles business - a deep cyclical industry

Illiquid share

Your different views accepted. Disclosure: Invested. Not a registered RIA. Not a buy/sell recommendation. Consult your Investment Advisor.

Good article which mentions why Ramco group wants to reduce/eliminate all cross holdings. (basically foriegn investors avoid investing in group having multiple cross holdings and various holding structures and group wants to attract more FIIs). The article says Ramco Industries would be holding co of all other listed cos.

Initially I though the article is just a rumour but things are happening as per the article.

Ramco cements sold all shares of Ramco Industries.

Ramco Industries to buy Rs 160crs worth of Ramco cement shares

Rajapalyam to sell Rs 120crs worth of Ramco cement shares. (most like to Ramco Industries). Not sure why Rajapalyam buying ramco industries shares…

This is a good trigger. Added today.

Disclosure: Invested . Not a registered RIA. Not a buy/sell recommendation. Consult your Investment Advisor.

With Cotton Yarn spread increasing from 87-88/kg in Q1FY25 to 90-91/kg in Q2FY25 i expect the operating margins to rebound to 12%. Regarding revenue i feel with capacity utilisation at 45% in the fabric division for q1, they should reach atleast 60-70% by year end with this boom in textile markets.

Also, Ramco cements is near ATH, and i have seen holding cos doing better when the underlying keeps on hitting highs. Additional as mentioned in the earlier posts, there could be reduction in cross holdings by the grp which gives more comfort