From the Q4 2023 concall:

Although we anticipate another quarter or possibly two of

challenges, we are optimistic about returning to our normal earnings range

soon.

(Emphasis mine)

From the Q4 2023 concall:

Although we anticipate another quarter or possibly two of

challenges, we are optimistic about returning to our normal earnings range

soon.

(Emphasis mine)

The last time they took advantage of similar down curve they posted rs19 eps… this time they are operationally in better position… lets see 2 more quarters…

In simple terms you will have 100cr extra being shelled out to interest expenses., ideally they should do 250cr PAT in normal seasons now it may be jus 150cr which means around rs 3 eps.

But sez plant and other operating efficiency which they said will kick in… may boost profits to unseen levels …

And any interest rate reduction in coming year in US may give added boost… hence I think its safe bet from here since it seems worst is behind…

The second problem is the raw material cost which is hurting the income margin significenly respect to previous years:

Always the price difference is passed on to customers with one or two quarters lag effect., that is what is happening now., when the prices goes up from here which should since it has bottomed out., they will reap the benefits of inventory…they easily maintain 14% plus margin always… check last 10 years data

As an update on the progress of our ongoing R&D project focused on

Anhydrous Carbon Pellets or ACP, we would like to inform that this

initiative is strategically aimed at meeting the long-term demand for RPC,

essential for manufacturing the ever-increasing demand for CPC from our

valued Aluminium Smelters.

We have received promising feedback from couple of North American

Aluminium Smelters, which has fueled our determination to enhance the

competitiveness of manufacturing ACP. Our efforts are concentrated on

optimizing the conversion cost while utilizing marginal grade RPC for ACP

production, which is essentially high dense raw material. Notably, the

utilization of ACP will not only bolster cost-efficiency but also contribute to

a significant reduction in CO2 emissions, aligning with the sustainability

goals of our Aluminium Smelters.

Moreover, our exploration extends beyond mere substitution. We are

actively investigating diverse applications for ACP and are diligently

pursuing patent protection to safeguard our intellectual property rights.

Once the operations of the ACP Plant in the USA are stabilized, we will

seamlessly transition to advancing the ACP Project in India.

It is important to emphasize that while ACP does not directly contribute to

incremental revenues, its adoption as a substitute for RPC or in CPC

manufacturing processes for use by the Aluminium Smelters underscores

its strategic importance. ACP represents a tangible opportunity for our

partners to not only optimize costs but also demonstrate a commitment to

environmental stewardship. ACP is a transformative journey shaping a

future that is both economically viable and environmentally sustainable.

Notes from the Transcript of Management Commentary on Annual Audited Financial Results

Margins

2023 review

Outlook

External challenges

CAQM relief and impact

(Commission for Air Quality Management)

Reason for poor performance vis-a-vis competition

I bought back the sold quantity today at 179. Since CAQM ruling, FOMO is created in me for this stock, though I know it will take 3-4quarters for improved results as told in conference call.

Thats good, i think it will stay at this price level for some quarter. So, it a good point to start accumulate.

Disclaimer - Very closely tracking & not invested

Ganesh Nicely written, the gist of the working of RIL

One important thing I came across in annual report published today:

In 2023, we achieved a significant milestone in our Carbon segment by completing industrial-scale aluminium smelter trials of our proprietary Anhydrous Carbon Pellets (ACP). These trials involved a shipment comprising 70% CPC and

30% ACP, with the resulting anodes successfully utilised in electrolysis.

We are awaiting final feedback from the trial, quality testing results. Additionally,

we devoted significant effort towards investigating ACP production flowsheet changes to increase production rates. While the upgrade project is currently on

hold due to market challenges, we remain optimistic that the identified optimisations will enable a threefold increase in ACP production rates in the future

Calcined petroleum coke (CPC)

Coal tar pitch (CTP)

Cement

Carbon Segment:

CPC Outlook

Advanced Materials Segment:

Cement Segment:

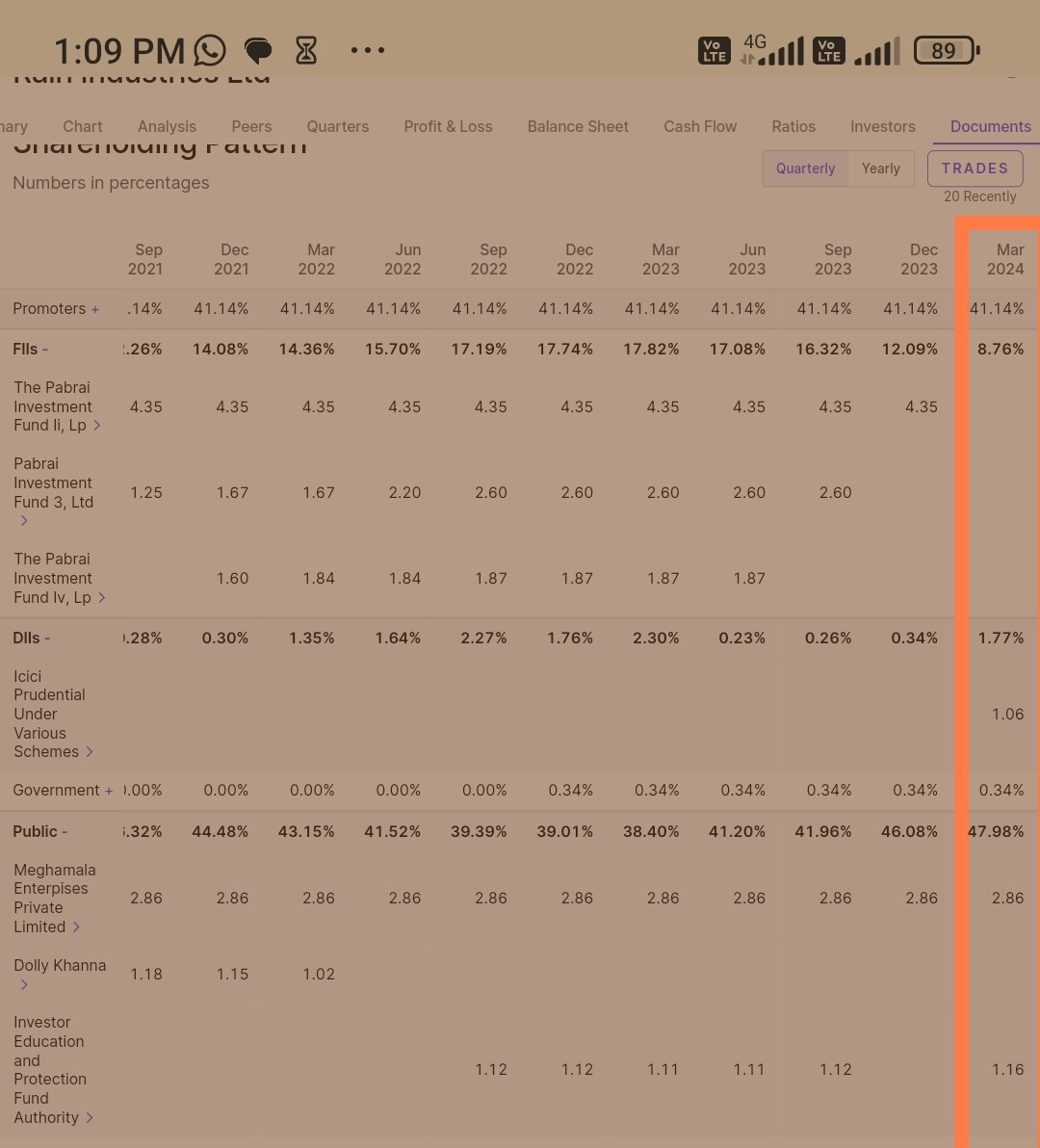

Pabrai has exited Rain Industries completely in March quarter, this time no notification from the co.

An expected move from Pabrai.

Good thing is most of the selling got consumed without much(any) downside on the share price.

Pabrai India investments did not perform so well, he has exited edelweiss and major chunk of Sunteck also

He is interested in Metallurgical Coal which is needed for steel and iron which are needed to build cities & hence he has invested in American Companies…

Good commentary from the management today, few highlights

On recent relaxation of those import restrictions:

“RAIN anticipates finally being able to ramp-up the

Indian operations to higher capacities, which would allow us to significantly improve the overall performance”

Regarding the import of GPC and CPC for RAIN’s Special Economic Zone plant:

“cannot begin its ramp-up until that clarity is given. We anticipate those regulations to be issued soon”

On aluminum, its role , demand and growth:

“Trends such as the shift towards electric vehicles, lightweighting in automotive and aerospace industries, and the growth of renewable energy infrastructure are expected to drive demand for primary aluminium in the coming year”

On Advanced material segment:

“In response to these trends, RAIN’s R&D teams continued in 2023 to work on several new and innovative products and materials in the battery space for future launch.”

“Due to an improvement in demand for HHCR,

coupled with our regional customers’ preference to procure larger quantities of HHCR locally, we expect to reach 50% capacity utilization at our German HHCR plant by the end of 2024.”

On reducing Debt:

“The cash flow from our operations, including the release of working capital which accompanies a fail in commodity prices, would be applied to reduce our debt.”

On normalizing fuel and energy cost:

“By combining our Cement segment’s waste-heat power production with our now-further-expanded solar electricity generation, RAIN is making great strides in producing cement with an ever-lower carbon footprint, by using 39% of electricity consumed in manufacturing of Cement from Green

energy sources.”

Further

“We anticipate a positive shift in demand for RAIN products starting in the latter half of 2024”

Any further SEZ delay will be concerning… time is ticking, as Sanvira coming up with huge plant in Oman. additional to already commissioned plant.

Eagerly waiting to read your comments on quarterly results @Srinidhi_Adiga @Rahul_Singh_Dhek and @amit.wilson

Need to wait for another quarter, no much insights from this results…