This is quite insightful. just trying to understand if they refinance debt which means they will not reduce overall debt and it would remain on them for many years to come.

This is fifth year I am holding this stock. Clearly I am victim of Value trap and I think even Monish Pabrai is trapped. The kind of cach flow this business generates is mind boggling. May be this is the reason for holding

2 Likes

By definition, in this industry you keep the debt on balance sheet as this is treated like utility based business as Aluminum/Steel/copper will needed for foreseeable future for this industrial metals so if you pick any player in industrial metals they will (most likely) have debt around 1:1 or more as you can clearly see improvement in ROE.

Though recent bull market in these metals have helped companies to reduce debt but you can assume that this will be there.

For RAIN IND, if you heard management in past, they had never said that they wanted to be debt free. Of course, at that time debt was much cheaper so it was good as your ROCE is >interest rate you are paying on your debt (by margin!) but now interest rates have increased both USA and Europe so we need to see how much they go ahead and refinance. If management thinks that they have enough for WC then they might pay 40-50m USD and rest refinance as they have around 140m USD in cash or cash equivalent.

Thanks!

2 Likes

Actually, all the fellow value pickers posting in the thread are stuck in this stock(including me) due to coattailing Pabrai Sir. Mr. Mohnish is a fantastic human being,doing good work with the dakshina foundation. He has close friendship with Mr.Munger and I am sure he must have sounded off this idea with him. How I look at rain is that Mr. Pabarai has positioned himself for an assymetric payoff with Rain Industries, his average will be still below Rs.50-60 considering that he has sold some at around 400 levels and then bought at around 200. Rain Ind. is not a bad stock,its just that the business is very tough, Mr. Nellore is an honest man with limited desire to get phenomenally rich or gain popularity. However, the business being in many geographies is actually low ROE business and the market is valuing it that way.

3 Likes

Negatives for me

-

Debt

-

Low margins

-

Main business is Cyclical in nature

1 Like

Positive for me

Available at good valuation

Generating good cash consistently

Presently cycle is not at the top

Holding good amount of cash and inventory

Till now despite of good cash promoters were not interested to reduce debt because of low interest rate. Now intrest rate is increasing and any intention to reduce debt will be a game changer…

2 Likes

Dividend will be announced on May 9th along with results, expecting it to be 2.5rs or higher compared to last year dividend.

1 Like

Unlikely,

1.they have given 1 rupee dividend for like past 10 years. Unlikely they will increase it now.

2. Interest rates have increased, down cycle on cards, debt repayment obligations.

Unless the promoters have said that they will think about increasing dividends in one of the con-calls, its highly unlikely that they will do that.

2 Likes

1rs dividend announced.

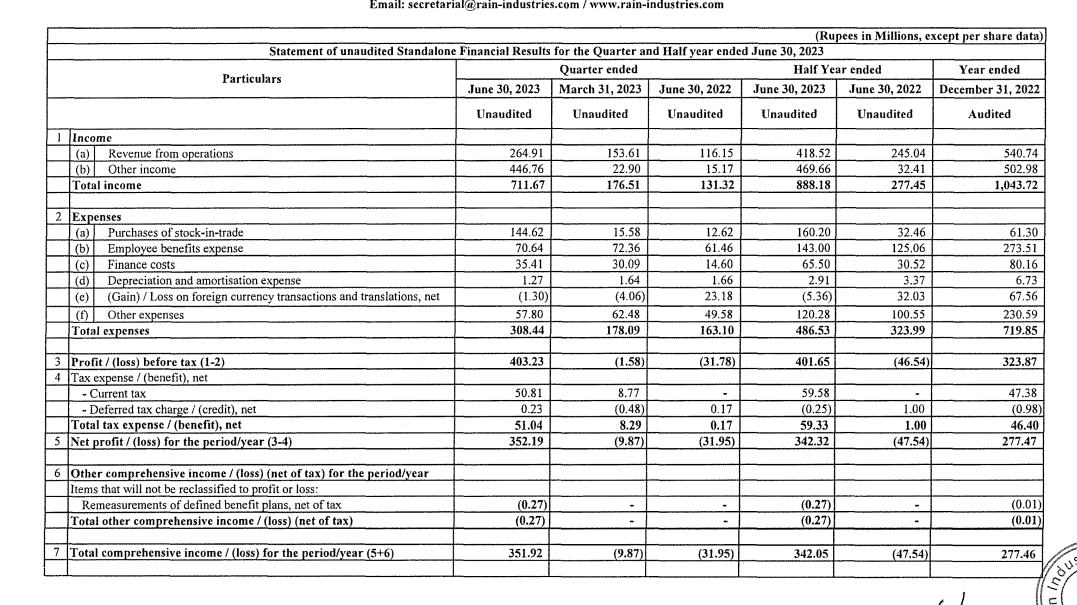

Unusual high raw material purchase at 1.1k cr generally it was at 500-700 cr. Mostly raw material prices might have dropped.

because they have taken 143 cr finished product realization loss this quarter as well.

Management call /presentation

1 Like

1 Like

Effect of the Notification: Import of pet coke for fuel purpose is ‘Prohibited’. However, Policy Condition 6 of Chapter 27 of Schedule-I (Import Policy) of ITC (HS) 2022 has been amended to allow import of Needle Pet Coke for making graphite anode material for Li-Ion battery as feedstock/raw material, and Low Sulphur Pet Coke by integrated steel plants only for blending with the coking coal in recovery type coke ovens equipped with desulphurisation plant, subject to terms and conditions set out by MOEF&CC.

2 Likes

Not sure how exactly this will help rain industry…

@Srinidhi_Adiga, please provide your comments on Rain Industries Results…

Invester presentation has some number and Board outcome report has other number. Please anyone can clarify

@starpenchal2018, Please refer to consolidated financials instead of Standalone financials.

2 Likes

As per me the main points based on results:

- ACP patented product is still under trails at customer end, with higher energy density this is game changer for rain, the dark horse… but there is no timeline from when it will start, however plants are ready both in USA and INDIA for the same.

- Second patented prodcuts like Petroras and Carboras will have more demand when China ecoomy will pick up, EV related products.

- HHCR resin plant have started in Europe where as two competitor plants are closed there. one is BASF , so demand will be suitable for rain .

IF USD or EURO appreciates it is good for Rain so no matter political or currency instability inside India. - Environmental norms have been issued from govt in june , which rain is already and exceedingly complying , these norms to be effective from mid 2025.

Overall the the management seems to be good and the renegotiated loan term which will be done in this month will also matter.

2 Likes

The real benefit from this stock may or should happen once ACP is started and loans are reduced(which management is focused now since capex are almost over including solar plants in India operational), EPS will shoot up to rs 15-20 ++ for quarters, I think it should take two years from now… if that happens rain is having potential to cross 500 in two years…

5 Likes

Below mentioned recurrent risks do not allow to judge the growth in sales and earnings of this business:

| # | Risk | Remarks |

|---|---|---|

| 1 | Regulatory Hurdle | .. Temporary green petroleum coke(GPC) import ban in India .. CPC import ban impacted blending strategy |

| 2 | Maintenance shutdowns | Both unplanned and planned |

| 3 | Weather disruptions | Plant closure |

| 4 | Seasonality | Impacts demand particularly for Advanced Materials segment |

| 5 | Weak end-market demand | Margins sustain even though Realizations and EBITDA are lower |

| 6 | Weak end-market demand and Increase in raw material prices | Margins impacted negatively alongwith Realizations and EBITDA |

| 7 | Suspending operations until market dynamics improve | Due to high energy costs or Weak end-market demand and Increase in raw material prices |

| 8 | Delay in pass through of incremental raw material costs | |

| 9 | High energy costs (natural gas prices) | |

| 10 | Supply chain disruptions |

Too much debt storyline:

| Year | Net Debt, Million USD |

Remarks |

|---|---|---|

| CY15 | 1013 | Bought back SSN of US$51.4 million 2 tranche of HY bonds, Maturing in Dec2018 and Jan20221 |

| CY16 | 927 | Expect Capex at ~$60 million, Balance will be used for expansion/deleverage/return to shareholders |

| CY17 | 999 | slight increase compared to CY16 due to the unfavorable Euro vs USD conversion rate and debt refinancing costs An ideal debt-mix between Euro and US Dollar debt to match the underlying cash flows of the company; the effective average rate of interest is reduced by 250 BPS.average interest rate after the January refinancing is about 5.3%. |

| CY18 | 993 | refinancing decreased its average interest rate to 5.3% compared to approximately 7.6% in 2017 |

| CY19 | 937 | Average cost of borrowing stood at 5.14% |

| CY20 | 932 | $280 million of cash, increased significantly due to proceeds from the sale of our Polymers business; average borrowing cost stood at ~5%. The primary goal is to reduce debt and interest expense |

| CY21 | 914 | must continue our metamorphosis into a 21st century company that transforms industrial by-products into essential materials for lighter, cleaner, and faster products and applications |

| CY22 | 958 | high earnings we enjoyed throughout 2021 and into first half 2022 |

| CY23 (WIP) | 890 → 852 | planning to buy back any shares? immediate goal is reduction of debt, considering the increase in the interest rates. plans for debt repayment and refinancing? expecting an increase in interest expense as the cost of capital has increased globally….watching the debt mkt closely and will continue to watch them to find the optimal time to refinance our debt. initiated the refinancing of our debt maturing during early 2025 and are expected to complete the same in next couple of weeks. |

Management is again looking to refinance the debt that is due in 2025 like it did in 2017 when the due date was in 2021. This is the only option as I do not see any alternative to repay all the amount within 2 years. However, interest cost will increase after refinancing due to current credit market conditions.

Why debt was not repaid with urgency (in the last 7+ Yrs. that I charted in the above table)?

Per my understanding:

- Debt had a low cost of capital compared to the ROCE. In turn, it enabled the business to earn decent ROE on their capital-intensive operations.

- With the above in mind, management focused on spending spare cash flows in strategic capex to improve the amount of operating profits.

What next on Debt?

I sense that debt repayment will become a key focus area in the coming years due to increased cost of borrowings. Paying interest expense will not be a problem (expect base EBIT of~1900Cr., and DA is a real expense and shall be excluded from calculating interest coverage). Also, repaying majority of the debt anytime soon is not possible due to insufficient yearly operating cash flows and management’s disinclination to consider asset sale alternative. I think that the business can do normalized OPM of 15% on a revenue of ~17K Cr.. In turn, EBITDA would be around 2500 Cr. Capex (maintenance), Interest, Taxes and Dividend would take away ~650 Cr., ~550Cr., ~350 Cr. and ~100 Cr. respectively. Hence, business will be left with ~800Cr. on a yearly basis to decide whether to repay the debt or do a strategic Capex.

Let us see how reality unfolds.

Disc: No Position.

15 Likes

Regulatory hurdle - there is no alternative technology to ban this material as of now, and emission wise rain have highest standards than any company in this field.

2 Likes