If this quarter result > 5000Cr then rerating will be expected after this quarter result.

3 Likes

One of the best stocks fundamentally with PE, PB and Price to Sales ratios, highest ever EPS as well as stable OPM. With natural gas prices coming down, it should be able to restart the plant in Europe.

The biggest concern with this scrip is, rising trend of debt and negative cashflow for last two years.

What am I missing here?

2 Likes

I think they are funding some CAPEX with debt. If you look at ther debt to equity, it is declining steadily. So, they are not going too aggressive with debt either.

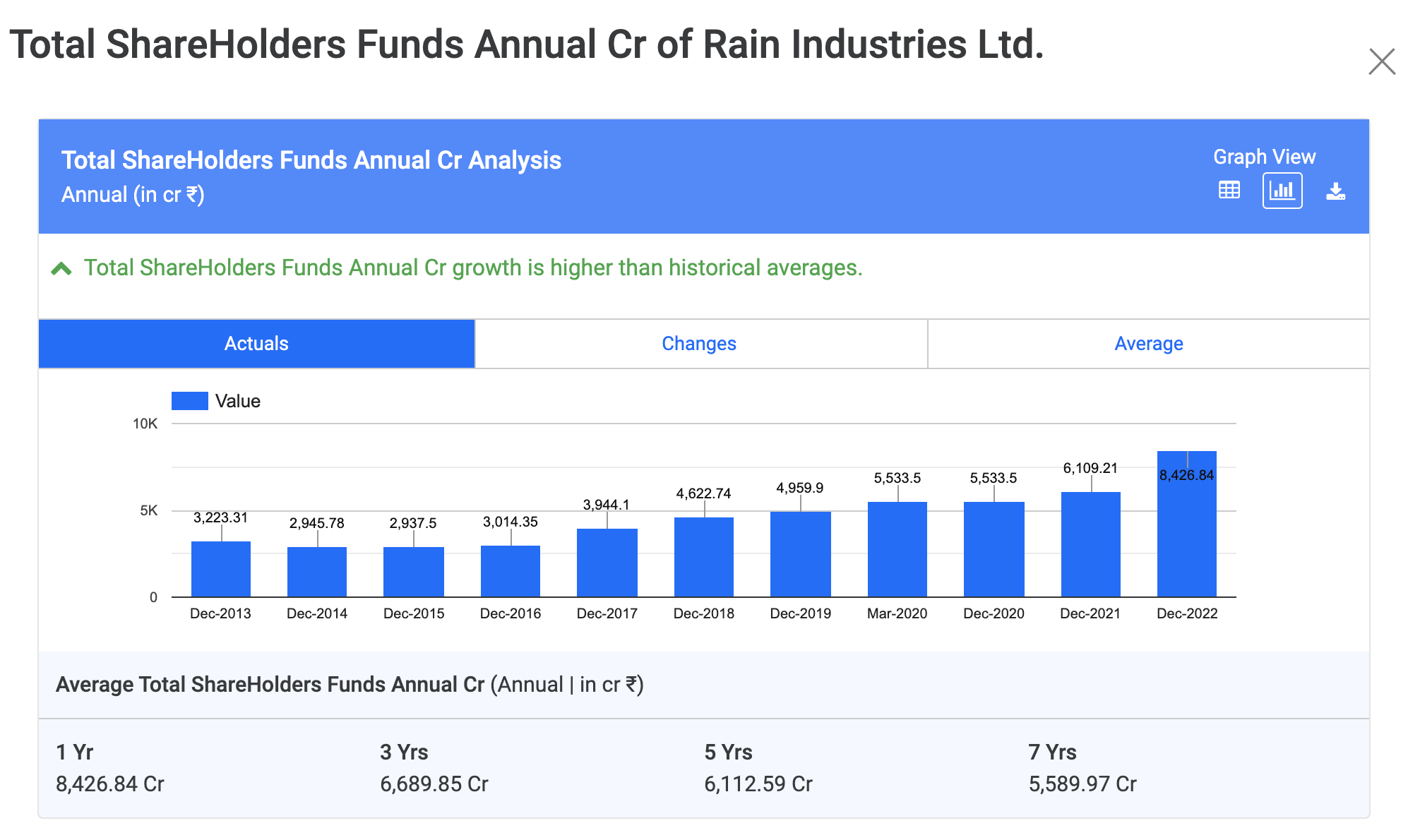

Their book value is increasing steadily too. So, debt in relation to this doesn’t seem to be an issue.

5 Likes

Rain Industries: Shouting Mid Cap Value Buy

Rational and Logic:

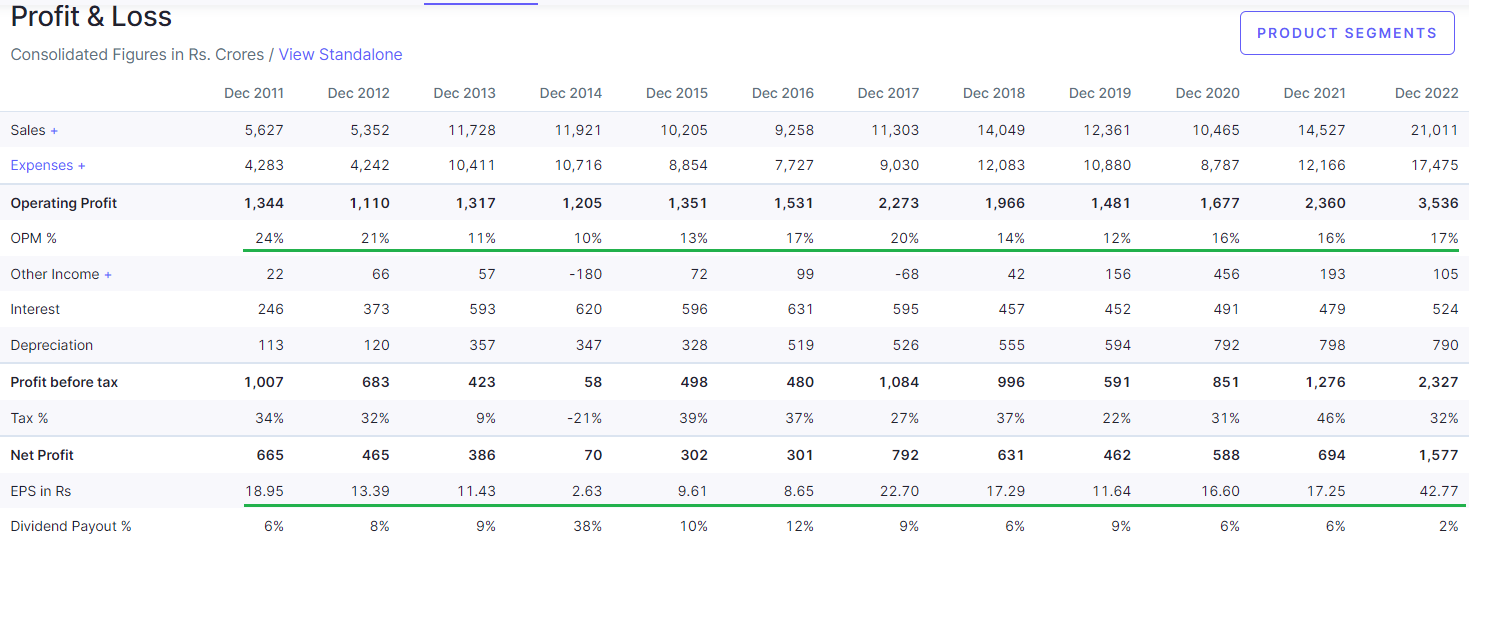

2022 CY profit - close to INR 1600 cr, 2021 CY profit - INR 700 cr, and expected CY 2023 profit will be around INR 700-1000 cr,

Sector PE at 34, EPS of last year at more than 40, at the current price and market cap appears a value buy.

Consistent EPS growth over the last few years

Significant sales growth as well, which is stable

The company have honest promoters, also Mohnish Pabrai, a US based investor and follower of Warren Buffet, is a big shareholder in the stock.

High debt seems to be playing on the company’s valuation, but the company will have increased cash flows as a result of savings in their cash flows now that capital expenditure is over.

Triggers for Upgrade: Recent re-rating of stock by India Ratings, Increase in Book Value over the past few years, Start of a plant in India going forward (this will take some time in my view depending upon the availability of the raw material).

Ind-Ra expects net adjusted leverage (net debt/EBITDA) to have reduced to around 2x in 2022 (2021: 3.20x; 2020: 4.28x, 2019: 4.63x) and the interest coverage (gross interest expense / operating EBITDA) to have increased to 7x-7.5x (4.9x; 3.5x, 3.3x), due to an improvement in the operating profit, led by a strong recovery in the commodity prices.

link to India Ratings Report - India Ratings and Research: Most Respected Credit Rating and Research Agency India

Disclosure: I am a current shareholder, too.

5 Likes

Just curious, how did you draw conclusion for Sector PE and which sector did you take for reference.

Thanks!

Khushal - would be interested to note your views on the following as part of the credit rating report :

“The revenue and EBITDA in 2022 are likely to have been significantly higher than the 2021 levels; however, the same would moderated in 2023 due to the expected further price correction in commodity prices.”

Do you believe that the stock price may correct further in the coming year ? Although the value and ratios may seem inciting - I do caution it may also have indicators of potential value trap if entered recently. However I believe this is a good company with fair fundamentals which could be worth revisiting in a couple of months or so - down the line in 2023

Even the management has indicated the environment may be challenging in 2023

Would love to your know your thoughts ? Do you foresee that the price has bottomed out ?

Personally I am of the opinion that the price may start to bottom out around 120-125

Disclosure : Not invested, but tracking closely for a future cyclical play

3 Likes

One needs to be extremely cautious on Cyclicals with low PE especially after the cycle has already topped out. If you’re planning to hold for a decade then fine, but if you’re planning for 2-3 years then it’s risky.

Also we’re in a high interest rate environment, refinancing costs would be higher for leveraged balance sheets eating away the bottom line.

6 Likes

They kept telling that they will cut down on debt,but they have yet to take action.

1 Like

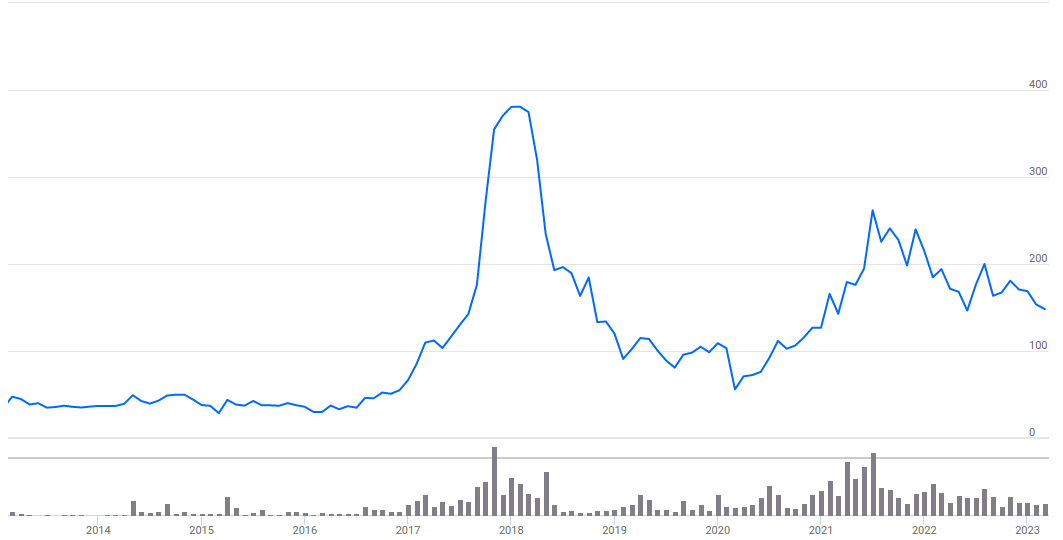

Just noticed some correlation between aluminium price and Rain’s stock price. Not implying that there is causation.

Aluminium price has seen peaks twice in last 5 years.

And these seem to be coinciding with last 52week highs of Rain industry (below).

I am not sure if it is entirely market sentiment or if there are underlying linkages, or may be it is just a coincidence ![]()

2 Likes

Aluminum is the one of the major end user industry of Rain’s products. Hence when Rain’s customer aka aluminum industry does well the company does well and hence the stock does well

2 Likes

Yes. I was expecting that too. But, when I checked the company performance, I didn’t see corresponding impacts on EBIDT margins or EPS. So, probably the market is reacting independent of company fundamentals…

As Rain describe itself of converter (with EBITDA margin fix of around 20%) so impact will be always lagging as it will benefit from supply demand mismatch (raw material price i.e. GPC prices vs finished product i.e. CPC).

Thanks!

The source for the sector PE is moneyconntrol.com

Thank you so much for your views. Its correct hence I mentioned that the Net profit for this year would be in the range of 700 - 1000 cr discounting the commodity price correction effect. Also even at this net profit levels, the overall net profit would be atleast double of historical levels and hence i feel it is a value buy. On the stock price front, its difficult to predict any levels as it is driven by market conditions. Overall, the point is any positive trigger which could be management deciding to do debt reduction etc could result in a significant rally only in few quarters.

2 Likes

Valid point… great insight. the scenario could change basis any positive trigger though

1 Like

They can’t repay the debt before 2025.If they choose to pay before 2025 they have to pay with higher interest rate.

Besides, Goldman Sachs forecasted that the aluminum price will be US$4,500/ton for 2024 and US$5,000/ton for 2025. - If this report prediction comes true, then sky is the limit. Source Link - Yieh Corp Steel News.

Goldman Sachs also predicted oil at 200 usd when it topped out at 140 usd. Predictions aside,we should mull over why we got ourselves invested in Rain Industries in the first place. Seasoned investor Mr. Sanjeev Khanna took a massive loss in this stock and gave up. Mr. Pabarai has held it for more than 6 years and is equally frustrated. I am a small retail investor, although the management is top notch integrity wise, but the business in which Rain operates is extremely difficult. In the last investor presentation, they have said that they are fine with aluminum at 3000 usd/ton…it is good for them to make reasonable profits. To be honest market has given up on rain share price improving in near future( less than 12 months).

I have held rain ind. for last 2 years with a small notional loss and larger loss of opportunity cost. I have now figured out that why Rain as a stock has not done well and will continue to underperform., It is the frequent empire building missions taken up by the management at the cost of huge debt pile. In the last qtr. itself they have written off several investments in plants etc. If they do not decide to " focus" on what they are good…the stock will continue to frustrate.

disc- invested at 180 levels since lst 2 years, 5 % of PF

3 Likes

Just trying give me 2 cents on above topics:

- P/E: In moneycontrol, it lists peer companies like PCBL and Goa carbon which have TTM PE 10 and 4.44 so no where near 34 (till few months ago, MC were including this company in cement sector - where it earns 7% of their revenue). I would not even consider them as their competitors as PCBL is totally different business and Goa Carbon is small compare to Rain capacity but by definition it will have different ROE/ROCE as their plant in 2 different economics so you also need to consider COF (I had write to company about their low ROE and they said it you need to consider us as US/Europe player).

- Pabrai investment: In last year he has increased in holding so I would not say he is frustrated, yes it’s not his best holding (might have even regret not selling in 2018 bull run). though it should not be major reason to buy or sell business based on some famous investor’s decision.

- I personally think though management is top notch but they do not try to anything for market (stock/valuation) so it’s stock price might underperform and they are not ready to sell cement business even at good value otherwise they can get 60-70% of today’s market cap just buy selling cement business (i think this is being first business is very close to their heart - it is like Berkshire hathway in Warren Buffett case).

- Debt: Major debt obligation will come in 2025 but I think they will refinance this year or next year. If I remember correctly, they can’t pre-pay money before Apr 2023 otherwise they need to penalty but I think after this months it is without penalty.

Thanks!

Disc: Major holding in PF

4 Likes

Rain industry has broken a major support on monthly charts and if there is a steep fall in NIFTY, then rain may go down to 110-120 price range…further the stock may continue to be in consolidation phase / move sideways for another 6-12 months…so investors will have to wait for perhaps one more year to make profits from this stock.

One the positive side, Rain industries long term chart patter is developing in a very potentially bullish fashion. Once the stock price comes out of this consolidation, then the returns from Rain industries can be quite big and in a short period of time.

Its a high debt commodity player- so once they roll over the debt it becomes a pure momentum stock. There is not much to analyse in any commodity stock. Just watch it carefully and jump in during the initial phase of the rally.

9 Likes