There is stock which i have recently came across. Followings are some details about this company. Companies data are not in detail avaialble but we can understand the sector and its seems good.

Stock name:- Sumuka Agro

Compnay Profile:-

Company is dealing in FMCG Segment. Currently, the Company is engaged in the business of Trading and Retailing of a wide array of Dry Fruits Products and ready to cook items, nankeen/ snacks products, sweet and spices, selling of packaged foods online. Company trades though its brand called “GUJJUBHAI NAMKEEN”

Distribution: When checked on amazon company products were not available and on flipkart only 2 products had shown. Company has long way to go on distribution front.

Industry structure :

Only 19% of market of FMCG represents f & b items which is expected to grow to US$ 70 Billion by 2025. Of the above US $ 70B, 96% of market in Packaged food is still Unorganized.

Khakhra & Bhakhri is a food which is still not recognized at a national level. Sumuka want to bring this healthy segment range and build a strong position in National & International market. Sumuka wants to capture 0.25% market share of unorganized segment by 2027. (i.e. Approx. US$ 0.2B) .

Threats

- Changes in Regulatory Policies.

- Increase in raw material prices,

- Change in weather conditions

- Unexpected market factor (possible changes in customer preference)

- Impact of currency fluctuation.

- Competition from domestic as well as international front

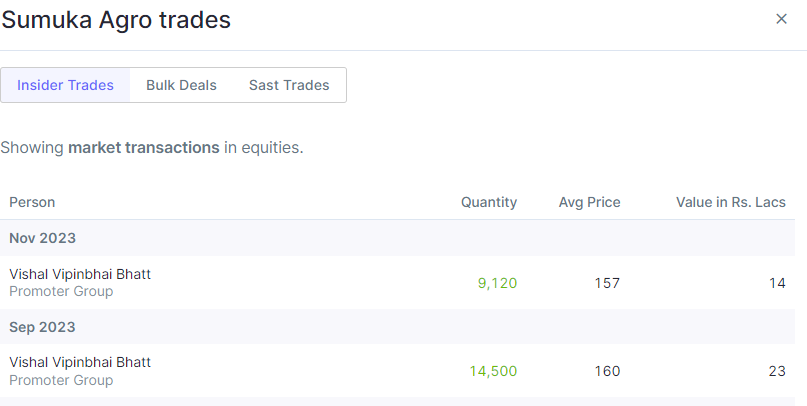

Investors: Promoter has been buying its shares and CMP is in range of 5% from promoter buying price.

Competion Details :- Compnay has competion from bikaji and haldiram. As bikaji is listed we will discuss BIKAJI here. Bikaji has target to have 2.5 lakhs touch points and they are very much on track. In Q2 FY24 they have added 46,000 points. Their currently touch point count is 2.05 Lakhs. Bikaji bhujia and namkeen products has been growing in double digits.

Future and valuation:-

Compnay is currently available at 28 PE and bikaji is at 85PE.

both bikaji and Sumuka has posted last qtr as their highest profit and sales.

Although on price to book ratio both are at 10 P/B.

Both have net profit margin of 10% and considering Threats to this industry I think inflation in RM prices may effect the company.

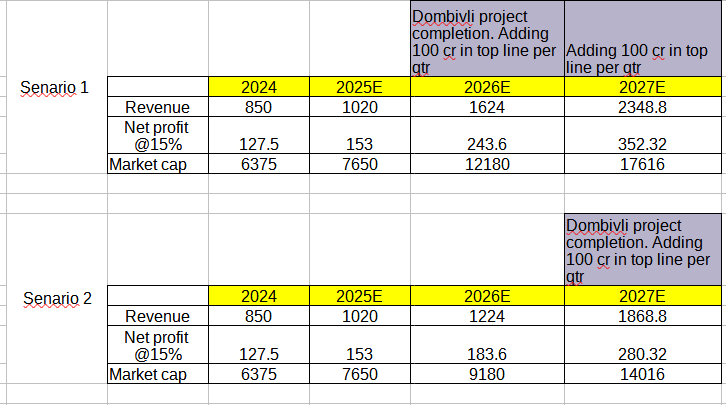

Assumption in Valuation:-

1)Considering 2018 to 2020 net profit margin of bikaji (bracket of 4 to 6%).

2)Companies target of acquiring 0.25% of all industry in packaged foods sales would be 1700 Cr considering this 50% of achievement sales would be Rs 850 Cr in 2027.

3) Average PE of bikaji in last 1 year is 80, Considering half multiple 40

net profit =Rs 850 Cr x 5%= 42 Cr

2027 price = 42Cr x 40(PE)= Rs 1700

Considering all above parameter I know target is very straggered but this is what it looks like as per management.

but if we skip management guidance aside and take bikaji growth rate which is 20% since last 5year. company would do sales(in 2027) of 90 Cr ,PE=40, Net profit margin = 5%

2027 price= 4.5Cr (NP year)* 40(PE)= Rs 180

Please guide and correct me!

I know this is very naive way of valuation but correct me on method or on technic.