Overall Theme

Bottom up picking, Look for beaten sectors, Look for Turnaround Companies, Good Promoters

Prefer PE < 10 for adequate margin of safety

Horizon of 3-4 years, looking for 20 percent growth yoy

Folio constructed somewhere around start of 2017 (Nifty at 9200)

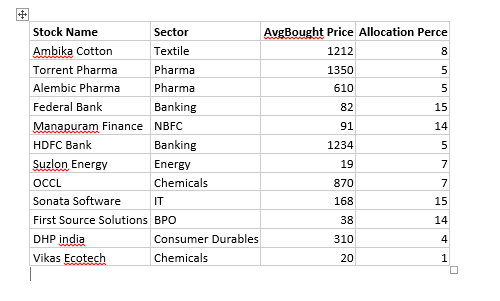

Ambika Cotton

Study Growth, Good Promoter, and Stability to portfolio

HDFC bank

Study compounder and consistent performer

Federal Bank

Private sector banker on fast growth over the last 2 years with consistent performance. FY 18 growth seems to be on track.

First Source Solutions

Value buy, Study turn around, Study growth over last 3-4 years,dept free by FY 19 which will double EPS, Might get re rated

Sonata

Value buy, Study turn around, Study growth over last 3-4 years, good dividend, IP focused delivery,Might get re rated.

Torrent /Alembic Pharma

Good number of ANDA filings, hopefully able to maintain margins and growth (Need to reevaluate as the pharma sector is undergoing headwinds)

OCCL

Among the market leader (top3) in world, Capacity expansion will boost its sales and profits. Good management

Manapuram Finance

Value buy, Growing rapidly non gold folio, good management, possible re-rating

DHP India

Could be multibagger microcap, consistent financial numbers, growing at good pace

Suzlon Energy

Turn around candidate, debt reduction, Sangvi on board, Lessons learned from past, Bullish on future for renewables (though am skeptical on huge equity base and wind energy vs solar for pricing)