Hello Investors ,

I am Raghav Singh completed my MBA in finance and currently pursuing my portfolio management job with fx hedging and correcting durations.

I started my investment journey in December 2019 and my only purpose was to learn about what is mutual fund’s and how it cycle works and since their was some

family issues and my family had a huge investment’s in mutual fund’s and we all know when we ask mutual fund services like ICICI or Nippon to recommend us some

fund’s they give us their highly commissioned based fund’s. The thing I have learned from the market and have literally seen is that it always good to be

invested rather than waiting for the low’s. Consistency and compounding will always help you and to be optimistic is an added advantage. So yeah here I will be taking

about my portfolio both in mutual fund’s as well as stock and any of the feedback would be really helpful.

Before starting my discussion I have seen my portfolio going down -70 percent during pandemic to going up so yeah have seen almost

all the faces of market last year and I am a big fan of playing long term bets and getting the results from compounding.

I don’t know if any of my stock portfolio will be a huge multibagger for me but I will be surely keeping them for long-term and

my mutual fund portfolio is for playing sector rotation bet’s mainly.

Really it would be nice if the reader would be giving the feedback as I really want to know what all chopping I can do to optimize

my both mutual fund and stock portfolio

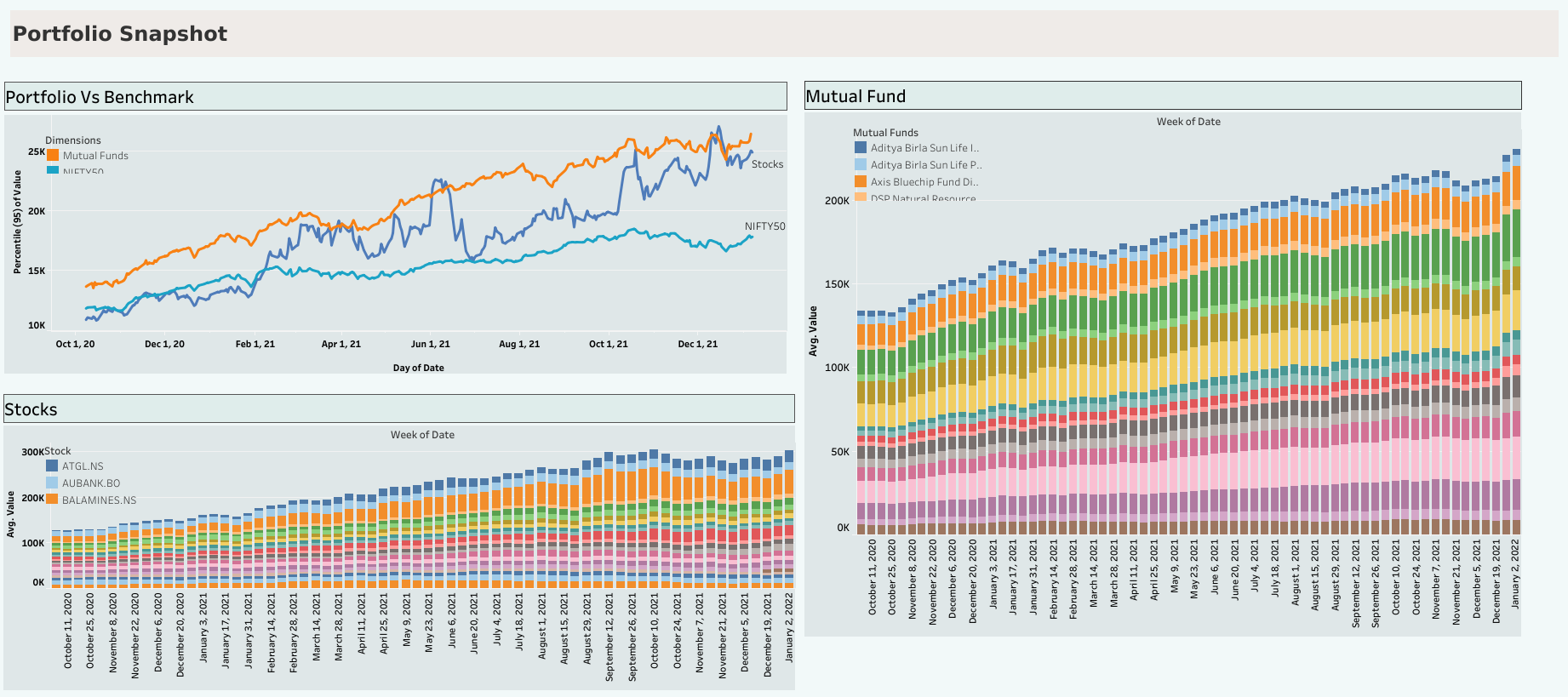

My portfolio is divided into 2 part’s

1. Stock Portfolio

Balaji Amines ( AVG - 812 , CMP- 2797)

They have specialized in the amines area and is a supplier to most of the big names in the Indian Pharma space. Also, they have a long term supply contract with BASF.

he margins are expanding due to softening of raw material prices. At the same time, the end product prices have also softened hence the turnover growth is not as high as production growth.

There has been good sales growth in last two quarters. Only thing is margins at net level are quite volatile ranging from around around 6 to 12% in last five quarters. Really a big fan of this company after the Covid’19 outbreak.

AU Small Finance Bank (AVG - 818.20, CMP- 1195.70)

I am huge fan of Indian banking industry and finding out underdog’s in them is my main motive. Au small finance bank is example of consistent growth as Over the last 5 years, revenue growth has averaged 41.32%, vs industry avg of 17.55%.

Over the last 5 years, net income has averaged 65.67%, vs industry avg of 19.75%. It focuses in rural and semi urban areas . It offers various services, such as commercial vehicle loan, car loan, loan against property, small and medium enterprises loan and have a really high foreign institutional

and domestic institutional investments in it.

CDSL( AVG - 753.87 , CMP 1052.55)

Currently there are only 2 DPs and there is a huge entry barrier for new players. The number of demat shareholders are expected to increase as many people / fund houses are entering the stock market.

Expenses are expected almost to be same and the upside revenue to grow y-o-y. Over the last 5 years, revenue has grown at a yearly rate of 15.56%, vs industry avg of 3.07%. Over the last 5 years, market share increased from 5.55% to 18.07%. Clearly market leader in it’s segment and since the time of pandemic the number of demat accounts opening are hell of a numbers.

Eveready Industries ( AVG - 168 , CMP - 338)

Always wanted to have exposure to battery sector in India we have giant like Amara Raja and even Exide is performing very nice but my bet was on Eveready

as Dabur increased their stake in it and demand for dry cell batteries, rechargeable batteries, flashlights, packet tea and general lighting products has

to be increased while doing work from home. Though the company has underperformed a bit and is really diversifying and decreasing their dependence on battery business.

Adani Total Gas ( AVG - 369 , CMP - 889)

In this particular sector I had a toss up between Gujarat gas , mahanagar gas and Adani gas since we all know how Adani is expanding business in our country plus

the revenue generation and total net income was higher than the industry so yeah until the Adani fiasco happened I was also bit concerned about my stock

selection though I had acquired it around 360 level’s it was never a concern for me but considering a good revenue growth and return on equity always wanted to

have this in my pf comparing it peers.

Finolex pipe industry ( AVG 124 , CMP - 183)

Finolex Industries Limited is a manufacturer of polyvinyl chloride (PVC) pipes & fittings and PVC resins. Company is almost debt free and having a PE around 15

vs sector PE at 60 is having it in very discount premium. Would be accumulating more with time as company is doing right thing’s by increasing margins

and increasing their product portfolio.

Indian Energy Exchange (IEX) ( AVG - 214 , CMP - 419)

It offers an online electricity trading platform for trading, clearing, and settlement operations alone leader in this with increasing

market share. The company has great return on equity and is almost debt free. With FII and DII both having stake in this for more

than 20% will be accumulating more with time.

Jamna Auto ( AVG - 53 , CMP -86)

Don’t have any auto sector stock rather have a mutual fund in it but thought of taking a stock which supplies major things to

the auto sector as supplying won’t stop so Jamna Auto is Jamna Auto Industries Limited is a provider of automotive suspension solutions for commercial vehicles.

One of the largest suspension manufacturer also the price of this gets affected by steel prices because of spring manufacturer.

The balance sheet is improving as company is reducing debt and I am betting on economic recovery which will mean to more purchase of vehicles.

Tata Consumer Products ( AVG - 602 , CMP - 763)

Diversified portfolio | revenue has grown at a yearly rate of 11.94%, vs industry avg of 8.37% | market share increased from 30.8% to 36.21% | really nice balance sheet

Vaibhav Global ( AVG - 738 , CMP - 810)

Really a fan of this stock whenever the major indices underperform this outperform them every time though from the time of stock split

it has made a flat base. Company is almost debt free. Company has delivered good profit growth of 47.54% CAGR over last 5 years

Company has a good return on equity (ROE) track record: 3 Years ROE 27.74% .

ICICI Bank ( AVG 511 , CMP -664)

Like earlier said I am huge fan of Indian banking industry and always want to find the underdog’s in them for ICICI bank what I believe

is very much undervalued as compared to peers. Net income has grown at a yearly rate of 12.55%, vs industry avg of 11.51%

HDFC Life insurance company ( AVG - 624 , CMP - 694)

The insurance sector is growing sector in India and with HDFC LIFE having return on equity around 14 % with great financials as

net income has grown at a yearly rate of 10.75%, vs industry avg of 7.22% and revenue has grown at a yearly rate of 31.58%, vs industry avg of 25.63%

The insurance sector will be really under boom after covid pandemic

Crompton greaves consumer electrical ( AVG- 388 , CMP - 460)

Crompton Greaves Consumer Electricals manufactures and markets a range of consumer products. The Company’s main products/services include lighting products (luminaries and light sources) and electrical consumer durables.

With FII and DII holdings is more than 10 percent and almost debt free company with diversified portfolio and with great results

profit growth of 39.58% CAGR over last 5 years and 3 Years ROE 38.12%.

The phoenix mills ( AVG - 718 , CMP -828)

Phoenix Mills is engaged in the business of operation and management of mall, construction of commercial and residential property and hotel business in India.

After the time of covid most of realty and infra stock were heavily undervalued so really wanted to have something from that sector

Numbers looked decent, strong growth consistent with valuation, PE wise and seemed this consumption story/overall trend would be a good long term play.

Nesco ( AVG - 553 , CMP - 659)

revenue has grown at a yearly rate of 3.72%, vs industry avg of -3.42% | net income has grown at a yearly rate of 3.65%, vs industry avg of -11.15%

Can see that company know how to operate in the time of pandemic as well with decent results with debt free company.

Mutual Fund Portfolio

For mutual fund my main aim is for untill any sort of financial emergency I will be accumulating on my respective funds and will

be allocating some amount according to the market cycle:

-

ICICI prudential Banking and financial service ( 11 % of folio) (

Main reason of buying this was banking sector was hard hit by pandemic and getting BANK nifty at 21000 was pure steel. -

DSP Small Cap ( 10 % of folio)

Small cap at that time was typically undervalued and by November 2020 I had started increasing my stake in this -

Quant Mid Cap ( 10 % of folio)

Same for midcap as well was very undervalued and typically started increasing my stake -

Edelweiss Greater China off shore ( 9% of folio)

Foreign Exposure as whole of 2020 was China boom -

Axis bluechip Fund (9 % of folio)

Typical Large cap -

Parag Parikh Flexi Cap ( 8% of folio)

Always meant to be in folio due to it’s magnificent performance -

UTI Transportation and logistic fund ( 8 % of folio)

Was very hard for me to go and find a good company for my stock portfolio that’s why though of picking whole set of companies

I know taking thematic funds is bit risky but can take that risk. -

Motilal Oswal s&p 500 ( 7 % of folio)

Foreign Exposure -

Motilal oswal Nasdaq ( 3% of folio)

Foriegn Exposure (IT Boom) -

Sbi Technology ( 6 % of folio)

IT boom sector -

DSP Natural Resources ( 5 % of folio)

-

Edelweiss Europe Dynamic ( 5% of folio)

Foreign Exposure so that can be typically diversified -

Aditya Birla Pharma ( 4 % of folio)

Pharma boom -

ICICI Infrastructure fund ( 4% of folio)

Almost a fourth thematic fund in my folio because I believed that infrastructure sector was really undervalued and was meant to be a next

market cycle with Covid relief fund’s and fiscal budget.

Learnt a lot from this forum and always wanted to have feedback in my portfolio so all feedback’s are welcome