Unveiling of two new luxury products.

2 Likes

Radico khaitan has come up with 2 new releases in luxury segment…

Magic moments dazzle vodka.

Royal ranthambore malt whiskey.

Royal ranthambore will be released in 7 states including U. P, Karnataka and other states during the first phase of launch… Free cash flows for year 2020 was -25 crores, for 2021 it was + 253 crores…

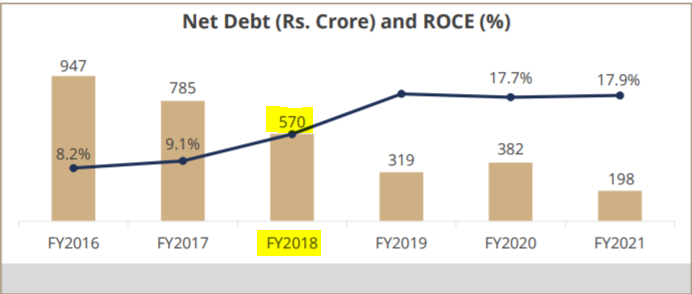

Roce Increasing steadily from 10% in 2017 to current 19%.

Cash conversion cycle reducing from high of 336 days to 238 days. Company hopeful of being debt free by 2023…however won’t be surprised if they do it early… Concentrating more on luxury segments which are high margins( looks like management is walking the talk) …

Steady going in first half of Q22…

Disc invested since 18 months , no transaction in past one month…

11 Likes

Investor presentation Q2FY22.

Concall

1 Like

Sharekhan has initiated coverage on Radico Khaitan

6 Likes

Significant greenfield expansion announced for Sitapur -

Q3 results investor presentation, pressure on margins is the key low light; nothing that I could notice as a highlight

2 Likes

Management has confirmed capex of around 7.4 bn to remove dependency from imports of ENA.

They are feeling inflation pressure in packaging of non-IMFL segment and glass bottles too with raw material ENA.

Business was in process of becoming debt free but they again started a huge capex which has caused stock price to come down.

Management is taking a risk to backward integrate also increase the volume but key risk I feel is management is not focusing enough to make brands reachable to more consumers.

Also the focus on bringing a good brand to compete with blenders pride is missing.

Premium segment whisky is surely going to face huge competition from foreign players as well as domestic players like Amrut and Paul John.

Expensive segments in whisky needs to be differentiated well as consumers of premium whisky are less and usually brand loyalty remains with foreign brands alot.

My view in long term is still positive but will have to watch and see if it doesn’t turn out to be a capex heavy business where management just don’t want to share wealth with share holders.

Disc:- Invested in business

6 Likes

I am worried about the newly formed co’s they will use it for capex , as in UP u can’t take land in a single name there are some restrictions, but matter of concern is that co must not use it for 3rd party transaction as election is approaching so there may be violation as I m expecting, will monitor it closely for 3rd party transaction, other than everything is fine, being a CMO earlier they know ENA price will hit their margin hard, as Ethanol exposure is rising more volatility may come, So Grain is the most best option which is ample available, also with the praj technology & dual feed will bring more yield with captive power consumption & BI & ZLD & lesser water consumption the margin will be much higher, as the new maturation capacity will make more P& A segment product, also extra ENA they can sell off to other CMO’s , so long term story is intact , just a caution for the newly formed 7 co’s

4 Likes

Q3FY22 concall notes

- Q3FY22 industry volume growth at 2% vs. 7% for Radico

- 9MFY22 industry at 14% and Radico at 18.6%

- P&A volume grew by 18% and Radico at 23%. (9MFY22)

- Core P&A segment reported volume of 18.5% and revenue growth of 21.5% YoY.

- 9MFY22 industry at 14% and Radico at 18.6%

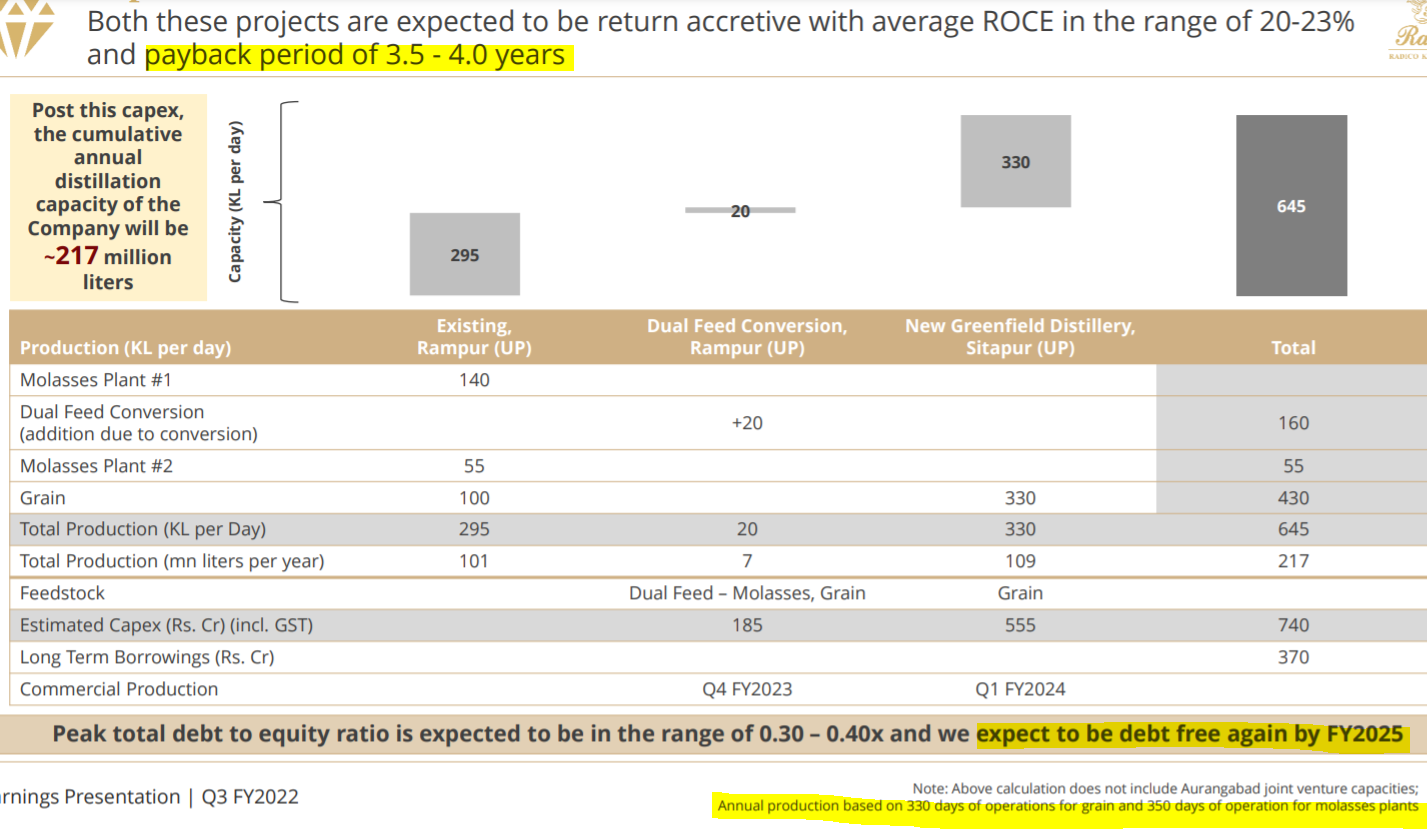

- Capex:

- New backward integration greenfield capex of Rs.555cr in Sitapur will be completed by Q1FY24

- 107 acres of land acquired and formed 7 step down subsidiaries.

- Rampur Dual capex of Rs.185cr will be completed by Q4FY23

- 50% Funded through internal accrual and rest through debt.

- Debt will peak in FY23 but will be debt free in FY25.

- 50% Funded through internal accrual and rest through debt.

- Both capex will generate ROCE of 20-23% with payback period of 3-3.5 years.

- Post capex the capacity will reach 217 million liters (currently at 101 million liters)

- Peak total debt to equity ratio is expected to be in the range of 0.30 – 0.40x and we expect to be debt free again by FY2025

- Rationale for capex: In future the company could face a problem of sourcing ENA so they want to start in house.

- The industry will move to Grain due to ethanol blending and Molasses will go extinct.

- Management says this investment is for their premium brands for next 5-7 years.

-

They are going to borrow Rs.370cr at 6-7% interest, whereas the yield is 20-23%

- The debt level will reach back to 2018 levels

- The debt level will reach back to 2018 levels

- New backward integration greenfield capex of Rs.555cr in Sitapur will be completed by Q1FY24

3. Magic Moments has 26% market share

4. Expansion of Jaisalmer brand distribution from 4 states to 10 states.

5. Dispatched first order for Rampur and Jaisalmer to CSD in January 2022

6. New Launches:

1. Royal Ranthambore Whisky and Magic Moments Dazzle Vodka launched in UP and Maharashtra initially and now rolled out in three more states.

2. DART Report: “The newly launched products are at a higher price point (Rs 1,650 in UP, Rs 2,700 in Maharashtra) and are expected to drive up the realizations going forward.”

7. Rise in freight cost by 5-6 times due to which exports are affected but order pipeline is strong.

1. Near term operating margin remains affected

2. This affected the Gross margin

8. Question: Bigger players are not putting up backward capex, why are we doing it?

1. Answer: Radico is the only company to create 10-15 premium brands in last 10-15 years because of our quality of spirit.

2. It is their strength like they had done earlier. They don’t want to outsource their USP to someone else.

16 Likes

Couple of Internal management team picking up shares from the market. One of them is VP of Finance.

Disc - Invested

6 Likes

Hi, Can you explain the meaning of realization? How do we calculate it?

For instance (this statement is from Q2FY20 concall): In terms of realization also, regular brands realization is up by 7.5% whereas Prestige is just up by 2.2% for first half as well as the quarter trend.

Revenues of the segment divide by the number of cases sold

Hi fellow investors,

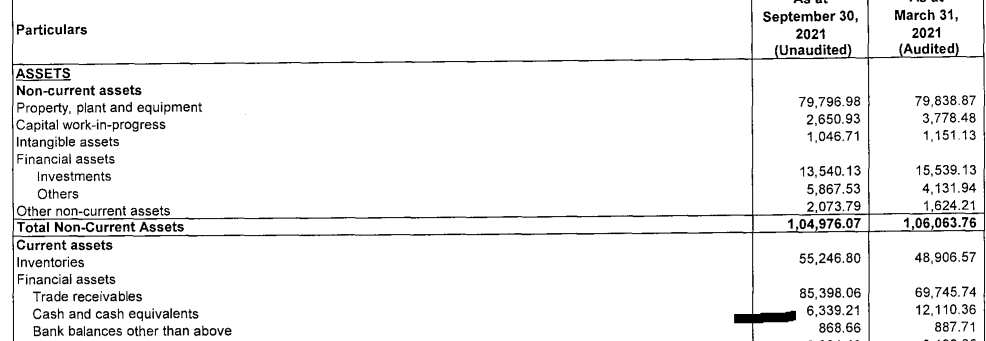

I was going through last year’s annual report and found that cash and bank balances were almost 13,000 lk while average range has been 1500-1800 lk. Has management ever shared their views as to why almost 8 times extra cash and bank balances were being maintained on balance sheet and why that couldn’t be utilised. Also because it makes ROIC to be -2% as per my calculation.

Have recently started studying this business.

@arjunbadola, @sujay85 if you could share your knowledge on the same too. Thanks.

2 Likes

13,000cr seems too high I think it was close to 130cr

That is in lacs so its 121cr in cash and 8.87cr in bank balances

Sorry for that but the question still holds valid. 11cr->130cr

That is a one time bump in cash part and this is reverted to normal when you see same in q2 fy22 balance sheet. And also you can also see there is equivalent amount of drop in accounts receivables and this also reverted back to normal in q2 fy22.

This could be because of some bulk payments from some customers

1 Like

I think there is huge fund requirement for payment of excise licences , Label registrations in all states and statutory expenses to be incurred in April every year.

2 Likes

Thanks for the reference.

Their cash balances did almost halve. Need to study the business and go through past few quarters to understand their cash and other strategies.

At least now for me, it’s not much of a red flag if such fluctuations keep happening.

FTA with Uk will affect the margins of Radico khaitan as india imports constitute majorly single malt whisky from UK. Prices of imported single malt scotch can be drop by almost 20%. Imo this will affect premium whisky segment which is focussed by Radico khaitan. With the availability of cheaper single malt scotch , there will be tough competion in market.

Dis: Invested from 870 levels. Can anybody confirm my above thesis.

7 Likes