Radico Khaitan is one of India’s oldest and largest liquor manufacturers. Formerly known as Rampur Distillery which was established in 1943. It was only in 1999, that Radico decided to launch and market its own brands, thereby embarking on a period of phenomenal growth. To further boost its production capacity of bottled and branded products, the company has tied up with bottling units in various parts of the country.

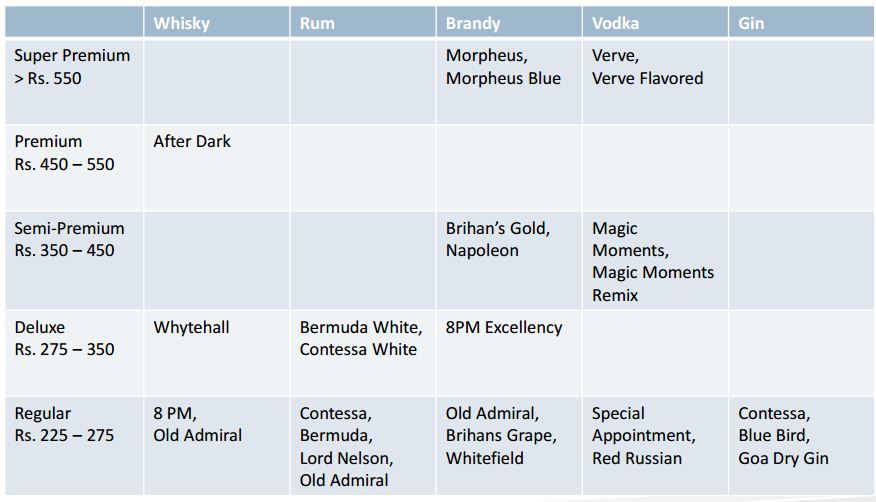

Radico Khaitan Ltd today has four millionaire brands in its portfolio. Radico’s flagship brand, 8 PM Whisky, launched in 1999, was a runaway success. In the first year alone, it sold one million cases - a record for any Indian or foreign brand operating in India. This also made it the first brand in the liquor industry to makes it to the Limca Book of Records. The other millionaire brands are Magic Moments Vodka, Contessa Rum and Old Admiral Brandy. Today Radico Khaitan has brands that straddle almost every market segment and price category.

Radico Khaitan is India’s oldest alcoholic beverage company. It entered the IMFL segment in 1999, with the launch of its flagship brand, 8PM. RDCK has three distilleries in Rampur, UP and holds 36% Interest in a JV in Aurangabad, Maharashtra. It owns six bottling units and maintains 27 contract bottling units. It holds 8% market share in the IMFL industry and ~24% market share in the CSD segment. The company offers all types of liquor, except for beer and wine, in regular and premium categories.

RADICO KHAITAN PRODUCT SPREAD

INDUSTRY OUTLOOK

The Indian liquor industry is a high risk industry due to higher taxes and innumerable regulations governing it. As a result, Indian liquor companies are suffering from low pricing flexibility and have insufficient capacities, which is consequently leading to their poor financial performance.

During FY2011 to FY2015 Indian liquor companies witnessed pressure at the operating level due to high competition and firm ENA prices. During the same period, various Indian liquor companies like United Spirits, Tilaknagar Industries, Globus Spirits and RKL reported EBITDA margin reduction of 1,255bp, 1,198bp, 850bp and 448bp, respectively. Also, the companies have high debt on their balance sheets, thus resulting in higher interest costs, and in turn lower profitabilities.

IMPROVING SIGNS

Liquor companies suggests that the industry has now bottomed out. It is now expected the industry’s pricing environment to likely get better going ahead due to the following reasons:

(a) Since the last two years, the industry has not received any significant price hike in its products due to delay in approval by state governments for the same.

Radico Khaitan has received price hikes in only a few states in the last eight quarters. Hence, the industry is now expecting significant price hikes in the coming financial year.

(b) The industry leader – United Spirits - is facing pressure at the operating level and the company has a huge debt on its balance sheet. Hence it is expected that the company’s new Management would shift focus on profitability over volume growth, which in would lead to increased scope for other liquor companies to hike prices.

Higher mix of Premium products to drive profitability for RKL

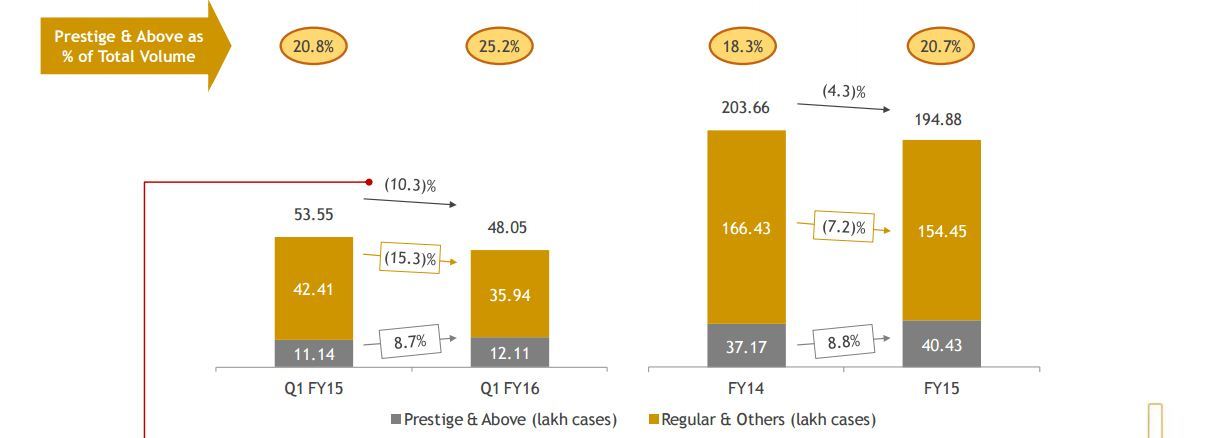

In the IMFL segment, more than 20% of the company’s volumes come from prestige and above products like Magic Moments Vodka and Morpheus Premium Brandy, and the balance from regular and others brands like Old Admiral Brandy, Contessa Rum, 8 PM Whisky etc. The company’s prestige and above brands command higher margins than regular and others brands. Since the last seven years, the company’s prestige and above brands’ volume has reported a CAGR of ~26% and their share in the product mix has increased from 7.9% in FY2009 to 20.7% in FY2015 and to 25.2% in Q1FY2016 due to strategic defocus on low margin products.

RKL is now more focused on selling higher margin products like Magic Moments Vodka and Morpheus Premium Brandy. Also, we expect volume contribution of prestige & above category products in IMFL segment to increase which would improve the overall margin for the company and result in higher profitability.

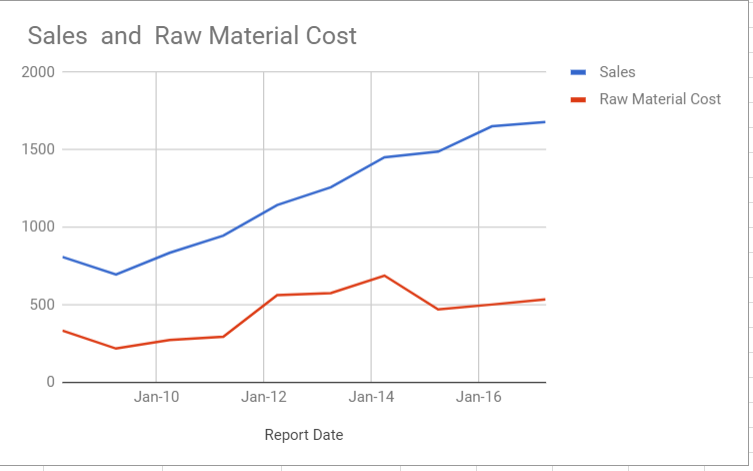

Raw material prices expected to ease

The price of extra neutral alcohol (ENA), a key raw material for the company, to remain stable and potentially even decline going forward. This is because sugar production during the October 2014 to May 2015 period has risen by ~16% yoy to 27.9mn tonne, which is an 8-year high production level. As a result ENA (a by-product of sugarcane) production too would be higher this year.

The procurement cost of petrol (excluding taxes) has reduced from ~48/liter in July 2014 to ~34/liter in July 2015 due to falling crude oil prices. Earlier, oil companies were procuring ethanol (to blend with petrol) at 44-45/liter when the procurement cost of petrol was around ~48/liter. Now, the price of petrol is around ~34/liter and ethanol costs around 48-49/liter which makes it unviable to blend ethanol with petrol. Thus, this would cut down demand for ethanol and lead to a decline in its prices.

Wide distribution network with strong brands

RKL has a strong sales and distribution network with a presence in retail and offtrade outlets in the relevant segments in different parts of India. Currently, the company is selling its products through over 45,000 retail outlets and over 5,000 on-premise outlets. Apart from wholesalers, a total of around 300 employees divided into four zones, each headed by regional profit centre head, ensure an

adequate on-the-ground sales and distribution presence across the country.

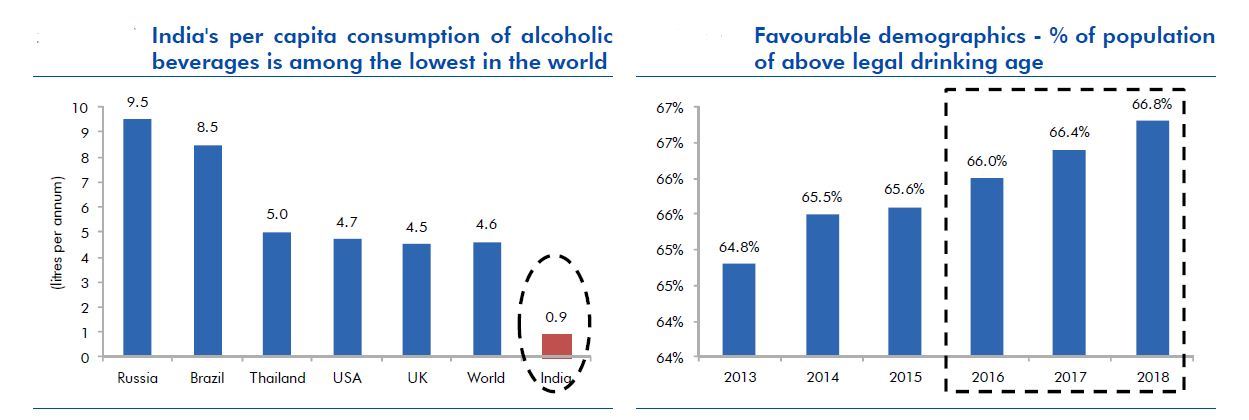

LOWEST PER CAPITA CONSUMPTION IN INDIA AND FAVOURABLE DEMOGRAPHY

HIGHER FREE CASH FLOW AND REDUCING DEBT

According to latest company presentation, it is focusing on cash flows and have reduced debt fro 903cr to 849cr in fy15.

CHEAPER THAN MOST LIQOUR COMPANIES

RADICO KHAITAN IS TRADING AT SIGNIFICANT DISCOUNT TO UNITED SPIRITS AND WE CANNOT CONSIDER TILAKRAJ INDUSTRIES BECAUSE OF VERY BAD SHAPE OF CURRENT OPERATIONS.

KEY RISKS

- Indian liquor markets are highly regulated and have many taxes.

- Liqour price increase is a political calss generally.

further relevant views are invited

Disclosure: i dont own any equity in the dicussed scrip.