I can see a high dividend payout of159.86% in FY12. Any reason why they paid out such a high dividend, dont they need cash for growth or they dont see any growth ahead and thus distributing cash amonginvestors?

The company has been very effective in terms increasing generating cash.

Last year company had in excess of 105Cr cash and have been able to generate positive free cash flows. If one time negative of “Payment of deferred consideration to erstwhile shareholders of subsidiary” can be ignored from Dec12 cash flow statement it did quite well in FY-12 also.

Given less capex required for the business, cash flow statement is expected to be decent in coming results.

Margin improvements have been observed in recent quarters and with weak rupee currency and export oriented business company is expected to post very strong results.

Currently trading at 16PE and buyback announcement (although less amount) for a debt free company providing good dividend yield this seems to be a very attractive bet.

Reviving this thread with Jun’15 results.

The company has posted excellent standalone results and ordinary consolidated results.

And lengthy disclosures in the quarterly results.

Results link:

http://www.rsystems.com/investors/PDF%20Page/Y2015/Results_for_the_Quarter_ended_june_30_2015.pdf

I’m at a total loss to understand their disclosures regarding transfer pricing, subsidiaries etc. etc. and what it means to the share price. If someone could explain that, I would be grateful.

From my primitive understanding it seems that

- Chennai and Pune businesses were transferred to a private limited company in India. What does that mean for valuations and results? (In Lynch lingo, spin-offs might be good. Is that the case here?)

- Company seems to have 100 Cr+ cash in bank accounts that can be returned to shareholders.

Views invited.

Thanks,

Rupesh

Disc: Invested, ~4% of portfolio

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Hi @suns

What is this comment. Please read posting guidelines before posting anything.

My only problem with this company is that it keeps on diluting the equity year after year thus hurting the existing share holders.If they are cash rich really a cash rich company as they claim to be why do dilute the equity every year…

And I am not sure when they will stop this equity dilution trend.

nabilmoideen,

Almost all technology companies issue employee stock options (ESOP)/restricted stock units (RSU) to their employees and when they are vested - number of shares go up resulting in equity dilution.

What is more important to check is -

- Percentage of equity dilution (which seems small for R Systems)

- KMP/Top management actions with these ESOPs/RSUs.

Thanks,

Rupesh

1 Like

R Systems International Limited (NSE: RSYSTEM)

The company’s share price (as on January 08, 2016): Rs. 73.80 per share

Market Capitalization: Rs. 940 crores

52 week high –low: Rs. 99.95(16/04/2015) – Rs. 59.00(27/07/2015)

Business

R Systems, founded in 1993, is a specialized IT Services & Solutions and IT-enabled Services provider catering to a wide range of global customers. R Systems is a leading provider of IT and ITeS services and solutions. R Systems’ core service offerings include Outsourced Product Engineering, sold under its brand of iPLM (Integrated Product Life Cycle Management) IT and ITeS services.

http://www.rsystems.com/investors/PDF%20Page/Y2015/R_Systems_International_Limited_Annual_Report_2014.pdf

In 2013, the company won India’s highest quality award, the “Rajiv Gandhi National Quality Award”. R Systems was listed among the top five best mid-sized IT and BPO organizations to work for by NASSCOM.

Ownership Analysis

Promoter and Promoter Group hold 50.8%.

Bhavook Tripathi, an individual investor, holds 36.85%

Hence 12.35% of shares are there in public float.

Customers

R Systems rapidly growing customer list includes a variety of Fortune 1000, government and mid-sized organizations across a wide range of industry verticals including Banking and Finance, High Technology, Independent Software Vendors, Telecom and Digital Media, Government, HealthCare, Manufacturing and Logistic Industries.

Currently, R Systems operate from 11 development and service centers spread across Asia Pacific, Europe, and North America. In 2014, USA geographic region generated 57.1% of company’s total revenue and Europe region generated 23.4%.

Investment Thesis

I. Industry:

The Indian IT sector is expected to grow 11 per cent per annum and triple its current annual revenue to reach US$ 350 billion by FY 2025 according to NASSCOM. According to Gartner, Global IT spending is forecast to grow to $3.6 trillion in 2016, a 1.5% increase from 2015.

According to India Brand Equity Foundation (IBEF), IT services in India are about 3-4 times cheaper than the US. IT-BPM sector in India is estimated to expand at a CAGR of 9.5 per cent to US$ 300 billion by 2020.

II. Improving financials

The company’s revenue and net income in the last 5 years (2010 to 2014) increased 123% and 364% due to both organic growth and thorough acquisitions.

The company’s SG&A as a % of revenue in the last 3 years (2012 to 2014) decreased from 27.6% to 23.4%.

The company’s EBITDA margin in the last 3 years (2012 to 2014) increased from 7.5% to 13.9%.

The company’s revenue for the nine months ended September 30, 2015 decreased 5.3% due to divestment of Indus Product Business. During the same period, net earnings increased 60%.

Strategic initiatives to focus on core businesses

In 2014, the company sold its Europe BPO Business.

In 2015, the company sold its Indus Product Business.

(Rs. in millions) Year ended

31-Dec-10 31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14

Net Sales / Income from Operations 2,925 4,110 4,658 5,967 6,534

Sales Growth % 40% 13% 28% 9%

Profit from Operations before Other Income, Interest and Exceptional Items 97 169 253 685 841

Profit before Interest and Exceptional Items 146 210 295 726 883

Net Profit 168 165 184 527 781

Key ratios

(Rs. in millions) Year ended

31-Dec-10 31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14

Return on Avg. Equity (%) 8.4% 11.0% 14.7% 33.6% 50.3%

Return on Avg. Capital Employed (%) 9.7% 8.7% 9.3% 24.7% 35.1%

Cash Dividends

In 2015, the company paid Rs. 4.90 per share as dividend to its shareholders. Its dividend yield is an impressive 7%.

(Rs. in millions) Year ended

31-Dec-10 31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14

Dividend Per Share 5.85 2.05 2.35 0.36 0.24

Buyback:

In 2015, the company repurchased approximately Rs. 595.74 lacs worth of shares (at an average share price of Rs. 87.85 per share).

III. Bhavook Tripathi’s presence

Bhavook Tripathi is one among the top 10 investors in India. To learn more about him, please look into the stocks like FAG Precision Bearings, Solvay Pharma and Excel Crop Care.

In September 2010, Mr. Tripathi announced that he holds 3.1% of R Systems. Mr. Tripathi steadily increased his holdings in the last 5 years in R Systems to 36.85% as of September 2015. It confirms that Mr. Tripathi is betting on R Systems to be a potential multibagger.

Risks:

Technological Obsolescence: The IT and ITES sector is characterized by technological changes at a rapid rate.

Currency Rate Fluctuations: More than 90% of company’s revenue, generated from foreign regions. Operating profits will be highly impacted by foreign currency rate fluctuations.

Comparable Valuation:

Company Name M.Cap. (Rs. In million) EV (Rs. In millions) EV/Revenue EV/EBITDA

Persistent Systems 50,380 45,300 2.2 12

Nucleus Software 8,040 5,570 1.6 15

Average 1.9 14

Median 1.9 14

R Systems International Limited 9,280 8,320 1.3 12

Potential Upside:

Scenario 1: Based on the comparables’ low EV/EBITDA valuation, the company has a potential upside of 20% to 30% (i.e. Rs. 88 per share to Rs. 95 per share).

Scenario 2: Based on the comparables’ low EV/Revenue valuation, the company has a potential upside of 10% to 20% (i.e. Rs. 80 per share to Rs. 88 per share).

(https://valuestocksindia.wordpress.com)

2 Likes

@Mr_Bharathi can you help me to check the source for buyout by company in 2015

http://www.rsystems.com/investors/PDF%20Page/Y2015/Results_for_the_Quarter_ended_september_30_2015.pdf

page 2 - point 6.

Thanks @Mr_Bharathi nice write up.

Thanks Mr. Gaurav. This was my first post.

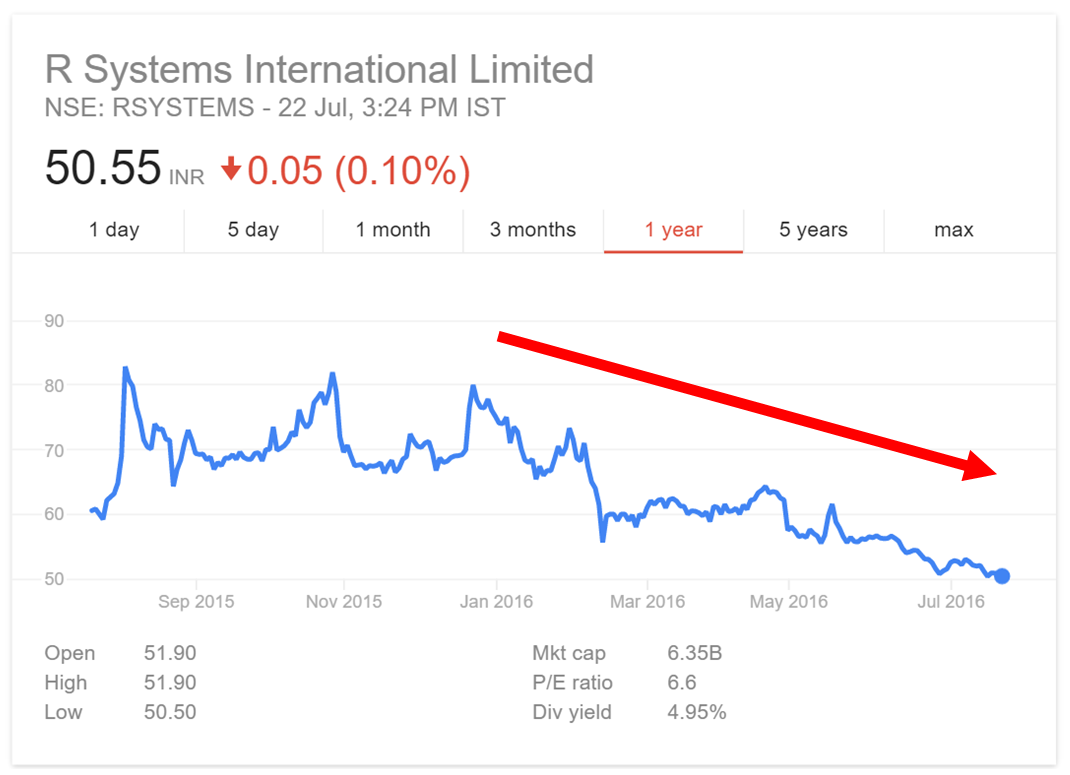

I could not understand why so steep rise and fall in the stock? Is it due to low holding by the promoters?

Source - moneycontrol.com

Something seems fishy to me here. Company did a buyback which was very minuscule quantity the stock price soared when buyback was announcement. Seems promoters used that opportunity to exercise options.

1 Like

From Oct 01, 2015 to Dec 31, 2015, the company received 2 investor grievance and they resolved it, as per the following link.

http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/0FA7B385_7391_4D69_B0E8_82C28ADA65E4_111617.pdf

Is there any relationship for the decline?

At current market price stock looks attractive

Is anyone attending the AGM?

The management says sale is impacted due to sale of Indus products. When can one see the end of the adverse effect and a growth in sales?

@Karl : You have any updates? Since you were tracking this company closely

I’ve also been tracking this stock for a long time and yes, the price of this shares is continuously falling since Dec’15.

With no drastic change in its financials. Also, It has great fundamentals.

I can’t perfectly say the reasons for this drop but chances are that the company is currently facing a slowdown due to global impact on Indian Tech firm.

Even other big players in this sector, like HCL, Wipro etc are facing a slowdown. It might be a temporary condition still take action with your due diligence.

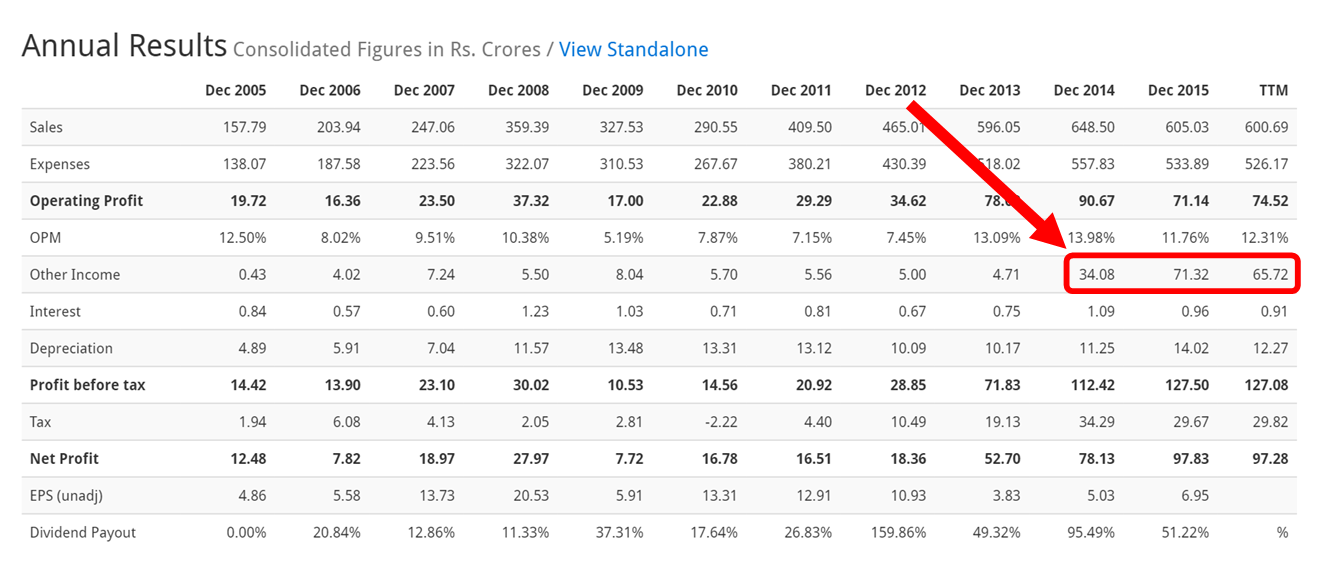

The thing which afraid me a lot regarding this company is it’s around 50% of profit consist of other income since last 3 years.

In simple words, only 50% of company’s profit is due to its core operational activity and other 50% are from other income.

Other income may include profit from the selling of asset, land etc.

SO it is a greatly associated risk as its profit will fade away as soon this other income will fade away.

Also, its compounded Sales growth are in decreasing trend:

5 Years: (15.8%)

3 Years: (9.17%)

TTM: (- 6.94%)

That is why the position of this company is quite suspicious. Can’t fully rely on it. There are many other excellent stocks out there in the market.

Disc: Invested but sold it a few days back.

1 Like

R System. Agreed that Other income will come down TTM Other Income “10.96 Crore” , so profit also coming down. However with P/E 14.11 & CMP/BV 2.39 & Dividend yield of 7 %, stock looks good buy for High Risk /High Return Kind of investors. Co also pays tax regularly.

Disclosure: Invested 4 % of my PF,

Update from Feb 2019

In a stock-market disclosure, R Systems vice president Ramneet Rekhi said that the acquisition has strengthened the company’s digital practice with niche data analytics competencies and a marquee customer base in the financial services industry.

R Systems further said that Innovizant’s facilities in Chicago will be used as a Center of Excellence, which will focus on developing new business models that use technologies such as Internet of Things (IoT), artificial Intelligence (AI), data science, machine learning and robotics.