Put option for NCI is essentially a contract that gives the right to the minority owners of the acquired firms, to sell their shares at pre-determined / determinable prices, in the future. So Quess will make this payment whenever it acquires the balance stake, and it cannot back out. So it is recorded as a liability in the books. When it makes the actual payment, cash will go away as will the liability.

You are correct, the fair value of the liability is not an expense, to the extent it does not change year on year.That’s because these liabilities are recorded at fair value, not at the actual payment. So if the fair value changes because of changes in what actually needs to be paid, and surely because as time between the reporting and actual payment closes, the difference will have to be passed through the P&L*. I will show one instance from their FY 17 and FY 18 Annual Reports below.

*There are some exceptions but that’s out of my syllabus

Therefor the total payout is not an expense and I was wrong.

Yes. However the liability can change and investors need to watch out. In the pre fair value days if a company said there is a liability for Rs 100, 3 years from now, then Rs 100 would be in the liability side and thus you know the actual amount that will be paid. Now this Rs 100 will be discounted, and if the discounting rate is 10% (higher in case of Quess), then Rs 100 will be shown as Rs 75.1 today, which will progressively increase to Rs 100, and each year there will be a progressive increase that will go via P&L. So in year one there will a charge of 7.5, year two of 8.3 and year three of 9.1. If an investor does not adjust to this kind of thinking, he is likely to be misled (not only that there can also be some absurdist entries)

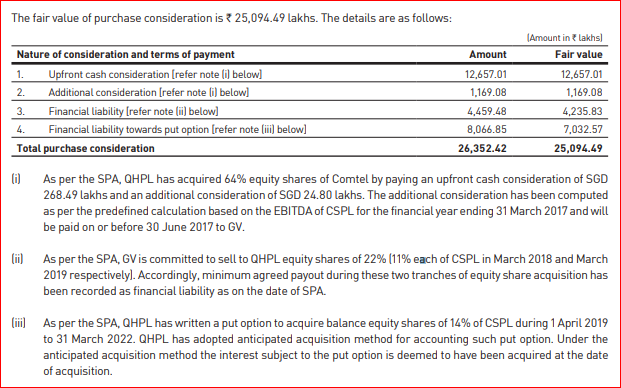

Let me highlight one case I saw in Quess. Quess acquired a company called Comtel Solutions Pte Ltd (CSPL). Here’s what they said about the acquisition in the Annual report of 2017

As of March 31 2017, Quess said CSPL was acquired for an actual payment of Rs 26,352.42 lakhs against a fair value of Rs 25,094.49 lakhs. The points 3 and 4 were payables including a put option, which was to be exercised during April 19 - March 22, as per the note.

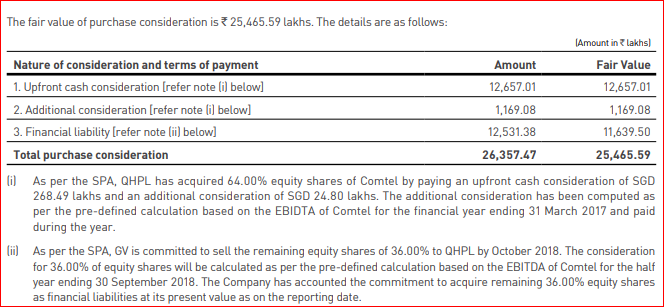

Now fast forward to March 31, 2018 and this is what we see:

The actual purchase consideration is broadly the same (an increase by 2 bps). The fair value has increased from Rs 25,094.49 lakhs to Rs 25,465.59 lakhs. This increase will be passed via P&L. But if you look closer you will notice that the terms have now changed. It says that now that the balance shares will be fully bought by Oct 2018 instead of Apr 1, 2019 - March 31, 2022. Thus the payout has advanced, and this will have an impact this year (FY19).

You can see this by looking closely at this:

This says that Rs 12,531.38 lakhs that will actually be paid by Oct 2018, and that this amount has a fair value of Rs 11,639.50 lakhs at March 31, 2018. This implies a discount of 13% p.a.!! And investors can expect Rs 9 crores to pass via the P&L in 7 months as cost of this financial liability.

Anyway I also got a report that talks, among other things, of aggressive discounting rates for fair value. These rates will come home to roost sometime, especially if numbers are not met.

, promoters and management did the right thing to offload a good chunk at 950+ levels much earlier !!

, promoters and management did the right thing to offload a good chunk at 950+ levels much earlier !!