Many may be aware of Thomas Cook and its largest and most prominent investment - Quess Corp. Quess is filing for IPO and I had a chance to look into its RHP, along with other public documents.

That is an excellent post Krishnaraj, thoroughly enjoyed reading it.

On that note, I have always felt that Fairfax, despite all its talk, does not really care much for minority shareholders. It is possible that their vision is really long term, but their short to medium term actions in the case of Thomas Cook and the whole saga of retaining Mr Isaac have been largely unfriendly towards minority-shareholders.

Surprisingly, nearly all institutional investors gave a thumbs up to TCIL’s proposition. It was only e-voting retail investors, some of whom voted against the proposal. This despite SES advising against the resolution.

A friend of mine asked me to look at Fairfax’ numbers closely; especially new share issuances. I was prepared but was surprised to see that since 1996 number of shares outstanding has grown by 2.2 times! In other words contribution to book value growth should have come substantially via new shares issued at fair value. The Fairfax latest annual letter begins - “We had another excellent year in 2015 even though it was not obvious in the numbers”. Maybe true in many ways but it sounds to me like “trust the numbers only when I ask you to”.

I have also been following Adi Finechem for some time now, prior to when Fairfax announced they were acquiring it. Here again, while I think the company will do well in the future - I am a little skeptical on the growth that most analysts have projected for it. Of course, a lot of these projections become higher once Fairfax announces its acquisition of the company. Overall, I think Fairfax invests in meaningful sustainable businesses, but the timeline for their returns seems to be very very large - far larger than probably what retail investors can hold for. For example, I cannot see how Thomas Cook will “grow” into its obscene valuation with the current model. Yes, I know all about operating leverage and all associated jazz, but there seems to be little light at the end of the tunnel after two years. How long will it take - 2 years more? 5 years more? 10 years more? There are business that will give you excellent gains in that time, and Thomas Cook in that time may just begin to justify its valuation rather than show any growth on top of it.

I have similar notions about Adi Finechem. The opportunity may be large, but I don’t think the Indian market (not the stock market, the market for its products) really needs the company at the moment. Maybe it could be an export play, maybe demand in India will increase substantially. But again, there will be a long period when the company will have to grow into its obscene valuation.

These are just off-the-bat thoughts that have been around in my head for a while, so feel free to dispute any of my conclusions.

By and large I agree with you that there is an “obvious over payment” for businesses. In fact Prem himself said that he overpaid to buy 9% of ICICI Lombard at 5 times book value (in small font) in his letter.

I do not know much about Adi other than casual reading but a friend pointed out that for such a high valuation that was offered, even the promoter partly cashed out.

I think Warren Buffett makes it sound really easy when he says that he acquires businesses and lets management run it as it wishes. He has mastered it no doubt but I think it is mighty difficult to sit in corporate office, own a bunch of companies and let managers have a free ride. At times others who try to copy this find stuck…like some manager saying issue me additional shares or I am gone. I recall Warren, after acquiring Buffalo News, spent 10s of millions turning it around via Stan Lipsey; and when it did turn around, no manager including Stan Lipsey was paid out of BRK shares simply because they did a great job.

Anyway it’s always nice watching the movie without any stake in it . Let’s see how it proceeds.

Also, I think in an advanced economy like the United States, “hype” is something that is tougher to generate for valuations than it is in India. Apart from a few select technology companies, you will rarely find businesses trading at 30-40 times earnings. Take the example of Harley Davidson vs Eicher Motors. Tomorrow if Harley were to decide to compete in the same segment and price point as Royal Enfield, I doubt Harley Davidson would start trading at an earnings multiple of 54, even though it could possibly ratchet up similar sales and growth.

In that sense, in the United States, getting a business at a reasonable valuation and having a good idea of how to turn it around / improve efficiency is a much more visible projection that can be relied upon by those with foresight. In India, I don’t see how it makes sense to pay 30-40 times earnings and then project stupendous growth in bottom line as well as top line. Buffet’s strategy is a lot more logic based and in my frank opinion, requires fewer magic tricks to execute than what Fairfax seems to be undertaking.

I remember reading the Q1 letter of Fairfax India Holdings and a lot of the pitch seemed to be on the India turn around story. In fact, at one point they inserted a rather ‘random’ comment when talking about Adi Finechem!

I guess they too are taking the ‘mother of all bull markets bet’

I think you should study fairfax more closely and not look just at the number of shares issued. What were the shares issued for ? have you looked at the accquisitions of oddsey re and other insurance companies for which these shares were issued ? did the company get value in exchange of shares issued ?

If over long periods of time a firm issues a lot of shares and I find that book value growth is near about share price growth (like in Fairfax) then it is highly likely, very highly likely that growth in book value on account of internal accruals is materially lower than growth in book value on account of capital raised on issue of shares. That is because the issuer will mostly have issued shares when shares are priced higher than the firm’s value, which will generally be much higher than book value. So if you mix newly issued shares that are issued at a premium to book continually over a period of time with existing shares that are growing through internal accruals, and you find that book value growth and share price growth in the end are the same, internal accrual growth will have to be lower than share price growth (dividend payout included as it seems low)

As a simplified example, say I issue 10 shares and raise ₹ 100 growing it to ₹ 110 end of year 1 when I raise 10 additional shares at 1.5 times book or ₹ 165. The book value after raising this sum is ₹ 275 with 20 shares outstanding and book value is ₹ 13.75 per share. I can now rightly say that book value grew 37.5% even though the internal accrual which is what should matter for value grew by only 10%.

It does not matter what was exchanged and what value the company got as it would get captured in the internal accrual growth.

Hi krishnaraj

i am not debating the mathematics of share issue above book value.

All that i suggested was to look at how fairfax has done on a per share basis, whether the stock is fairly priced today as it stands today and what has been the past performance of the company on per share basis (over a 20+ year period).

Look at their combined ratios and the improvements in their insurance subs and reason for lack of performance in the investment portfolio, and finally wholly owned companies before reaching conclusion on book value as true indicator of performance. you could be surprised.

anyway my comment was a suggestion to dig deeper and not argue If you have made up your mind, then its your choice.

That is what I thought I inferred from the math, i.e. that book value growth per share from internal equity will be materially lower than book value growth mentioned in his letter and why.

Thanks for bringing to notice the corporate governance issues. Its a tough but very important task.

I haven’t tracked Quess closely but I did attend the lecture of Mr. Ajit Issac and was blown away by the journey and thought process of the guy. During the Q&A, I did raise him a question - that his stake is pretty low and doesn’t he feel the pinch that he is doing everything but value creation is being done for “arm chair investors”. He did answer it well and added - these things are best solved by just sitting one day and talking it out with the majority investor…if he finds value in your services, you will be taken care off.

When the Fairfax gave away the equity to Mr. Ajit a lot of hue and cry was raised but I think it was totally normal and perhaps a good decision. I really fear an organisation where the key person running the show has a small stake and might be dis-satisfied.

Point no 2 raised by you on debt seems very concerning and there should be clarity on the same. As I don’t track the company or the space closely, I don’t have thoughts or clarity on other points.

you may note that the PAT is quoted in dollars whereas the growth in PAT is measured in rupees , during which time rupee fell from about 45 to 66, a 46% fall! In any case we may be digressing here.

Thanks Ayush,

Not being a TCIL shareholder, it is not my botheration on what happened between them; further, the transaction was done with a thumping approval of shareholders. However it does make one more cautious and circumspect about future transactions. Like the fact that part of the proceeds from Quess IPO will go towards capex of a subsidiary that would give 40% of its earnings till 2019 to Fairfax. RHP is does not clarify why.

Further the shares renounced by TCIL were to “secure his full commitment to the Quess performance” but the shares were renounced to a company nearly fully owned by AI where the only other director is the CFO and Wholetime Director of Quess. This entity has modified its MOA just after the renouncement, to get into various ventures like real estate etc. It is reasonable to assume that the value of the renounced shares to this entity will be used to undertake activities that will take away some commitment of AI. Consequently there are reasonable grounds to believe that TCIL’s idea of “securing full commitment” may not materialise.

Let me put some disclaimers so that i am not see talking my book - i have owned fairfax for sometime and also thomas cook. so you can take what i say with a pinch or bag of salt.

fairfax has sold at 3-4 times book in the past to close to book value recently. They have compounded their book value at around 20%+ in the last 30 years. even if you assume that they issued stock at 3 times book value (the higher side, although a lot of share issue has also been around 1.5 time book), it would account only for 7-8% of the book value increase. the rest has come from internal accurals which is basically retention of profits. so they are not running a forward chain letter scheme. A 15% compounding net of share issuance in a low inflation country is considered quite good

In addition to this, the book value has changed in the last 20 years. In the early to late 90s, this was an insurance company with publicly held securities and hence the book value approximated the market value of its assets. Since then the company has been acquiring wholly owned companies like oddessey rey, TCIL and many more. these wholly owned companies are valued at acquisition costs with some level of amortization of intangibles. Hence the book value understates the IV of the company.

hope this clarifies my comment, that the share dilution has accounted for at most 25% of the increase in book value

I am not making a case for quess, TCIL or fairfax. If one does not trust the management, then all this is a moot point.

@rr1980 : teamlease is in my humble opinion horrendously over-valued - 48x Fy16 EV/EBITDA and 35x FY17 EV/EBITDA as per sell side analysts bullish on the stock like IDFC (also IPO bankers) and Prabhudas. That too for a business with EBITDA margins less than 2%. Laws of gravity should prevail in this counter within next few quarters unless they can deliver stellar growth (which they havent in the past). I would avoid both Quess and Teamlease. Rethinking whether I should be holding TCIL

Its not good to read the structuring of the acquisition and then using the IPO proceeds for the indirect benefit of Fairfax.

On the second point - Somehow its not sounding very concerning to me because I believe the intent of giving shares to Mr. Issac for “securing full commitment” must be - 1. To make up for the lesser stake he had 2. Make sure that Mr. Issac doesn’t starts a new private venture in the same field and continues to give his 100% to Quess. The second point is really important and many often people do this once they have cashed out. Bigger example is the MNCs - most of them have set up new private limited companies in India just to get back 100% of the earning vs lesser holding in the listed entity.

It would have been bad and a question on the integrity had Mr. Issac started a private co with MOA to start work what Quess has already been doing. Renouncing shares to private company instead of individual name can be due to various reasons - one simple one is tax planning. Also, real estate is a very simple business and doesn’t need too much of bandwidth and attention (until and unless one is doing development work on a big scale etc).

I do feel that the management might have their genuine reasons for doing such transaction.

Its good that you have worked hard and raised the concerning points. When combined together, they need explanation from the management.

That’s fine. I hope to have the temperament to stick to facts and go where it leads me.

The question is to find out growth in intrinsic value (or annualized returns of employed equity capital) for Fairfax even as when it continually issued shares. One way to do that is to look at book value of a share at a point in time and see how much earnings it accumulated over the time horizon. Those earnings adjusted for reinvestment of dividends, spin-offs, adjustments for bonus etc over long periods will give us the growth / returns. These earnings will be generated from the capital used in the business; so fresh equity will matter only to the extent it gave earnings to the share.

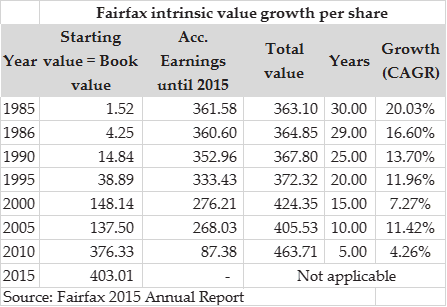

These figures are fortunately available for Fairfax, and given in page 1 of the annual report (FF AR 2015). So if we apply the method we see that end of 1985 book value per share is $ 1.52. This share over the next 30 years, from beginning of 1986 until end of 2015 accumulated earnings worth $ 361.58 giving us an annualized growth of 20.03% pa. That’s wonderful. (I ignored reinvestment earnings of dividends, and assumed there were no spin-offs / stock splits as I could not find them). Then I looked into their 1985 annual report (FF AR 1985) and discovered that substantial convertible capital (2x of equity) was added in Sept - Dec 1985 that was not counted as equity until 1986, but was equity capital for all practical purposes. So I decided to apply the same method from 1986 instead of 1985, as there were no such “equity capital not counted as such”. End of 1986, the book value per share was 4.25, and the accumulated earnings were 360.6, and the annualized growth drops to 16.6% pa. That’s a big drop from 20.03% pa and tells that that equity that is about to get fully diluted but not counted as such can be misleading. There’s nothing technically wrong with that but we need to be careful while evaluating performance.

I then carried out subsequent growth in value for a book of share end of every 5 years since 1990 and until 2015. The attached figures show that intrinsic value growth has dropped substantially since 1990 (at 13.70% pa) from the 1985 or 1986. Reinvestment income from dividends declared are not added but they wouldn’t change the big picture much.

From the figures in page 1 of AR 2015 we can compute how much of equity at the end of 2015 is external equity. We know opening equity or “Common shareholders’ equity” of previous year (call it A), current earnings (computed as “Shares outstanding” multiplied by “Earnings per share”) (call it B) and closing equity or “Common shareholders’ equity” of current year (call it C). So C - (A + B) will be the external equity added or bought back in any year by shares issued or bought back (say D). The sum of D for all years as a proportion of equity at the end of 2015 will be the external equity added. That figure is 31%. In other words, internal equity was only 69% and had to take external equity “steroids” to push shareholders’equity by another 45% (which is 31%/69%)

If I come to know that my rate of compounding over the past 30 years, was not 20% but 15%, it means I have just lost 72% of the wealth I thought I had. My self-potrait as a compounder will be go up in flames

I do not know how to evaluate management reliably so trusting / not trusting is beyond me.

Hi Ayush,

Not sure how you can say that in order for him to start a competing business we better give him shares?

Integrity, honesty and ethics demand that he not start a competing enterprise, if indeed that is the agreement he had with fairfax at the time of the initial sale of shares…

to then blackmail them into giving him more shares and short changing minorities as a result is UNETHICAL!

Corporate governance in India is poor because most investors worship management and management believe that they are doing us a favour. Once a company is listed, it is public and that means all shareholders should in theory be treated equally.

The 250-500 crore issue of shares to Ajit Isaac at par value only speaks of the disdain he has for his partners, i.e.Thomas cook and minorities. A fair deal would have been to give him options to allow him to raise his stake, this is usually how management is compensated in order to retain them or allow them to increase their stake in the business. This way the options vest over time and more importantly a fair price is paid for it.

Why did Ajit Isaac sell a stake in quess to begin with? he could have raised money from other sources or even from a private equity firm, but he is smart. He knows that in fairfax’s case he has a long term partner who will genuinely support him. A PE firm would have had him locked in with all kinds of punitive clauses.

In my experience if someone is willing to cross an ethical boundary, it doesn’t matter what you say or give them today to pacify them, eventually they will try something else in the future. It doesn’t boil down to a figure or right or wrong. so in order to give him extra shares today with the hope that in the future he stays doesn’t hold water…he could eventually sell out to the highest bidder…

Buffett and Munger let their blue eyed boy David Sokol go once he crossed an ethical boundary with them…no questions, no ifs buts or ands…im really not sure that Ajit Isaac is as valuable as David Sokol…

. Let’s see how it proceeds.

. Let’s see how it proceeds.