THE COMPANY:

Qualitek Labs, a NABL ISO / IEC 17025 : 2017 accredited laboratory company formed by Industry professionals having more than one decade of experience in the testing, inspection, certification, homologation and audit services. They have state of the art infrastructure facility at Pune, Bhubaneswar, Noida – India, offers innovative leading edge solutions to the automotive, electrical, aerospace and allied industries on testing, homologation, certification and consultancy. The services includes testing, Inspection, Research and Development, Consultancy. They serve various industry like automative, electricals, electronics, foods and drugs, energy, minerals etc.

The company came out with IPO in January, 2024 @ Rs. 100 per share. Later, in the month of August 2024, preferential allotment of around 26 lakhs shares was made to the group of 40 investors at Rs. 198 per share. In this Preferential issue Ashish Kacholia acquired almost 5% of the company.

The company is acquiring a group company ITC Labs Limited for cash consideration of 32 Crores [for 50% shares] and issuing 16 lakhs shares for remaining share swap. The company is also acquiring a software company- Quality and Testing Infosolutions Private Limited for a cash consideration of Rs. 5 Crores.

Presently the company equity stands at 9.98 crores, which will go up to 11.6 crores after shares will be issued to the shareholders of ITC Lab on share swap arrangement. Qualitek is mainly into automative testing (80%) and single digit revenues from water, minerals and defense sector. While ITC Labs is majorly into pharma, cosmetics and food testing. ITC Revenue was 32 crores in FY24, with profit of around 1.5 crores.

ITC Labs is facing a litigation issue. ITC Ltd has filed a case for the name of ITC Labs and defamation of 50 cr. This might lead to long legal battle but the order is on stay in Calcutta HC at the moment and company is allowed to use the name ITC Labs.

At AGM, chairman gave targets of 90 Cr. for FY 25 and 120 Cr. for FY 26 on consolidated basis.

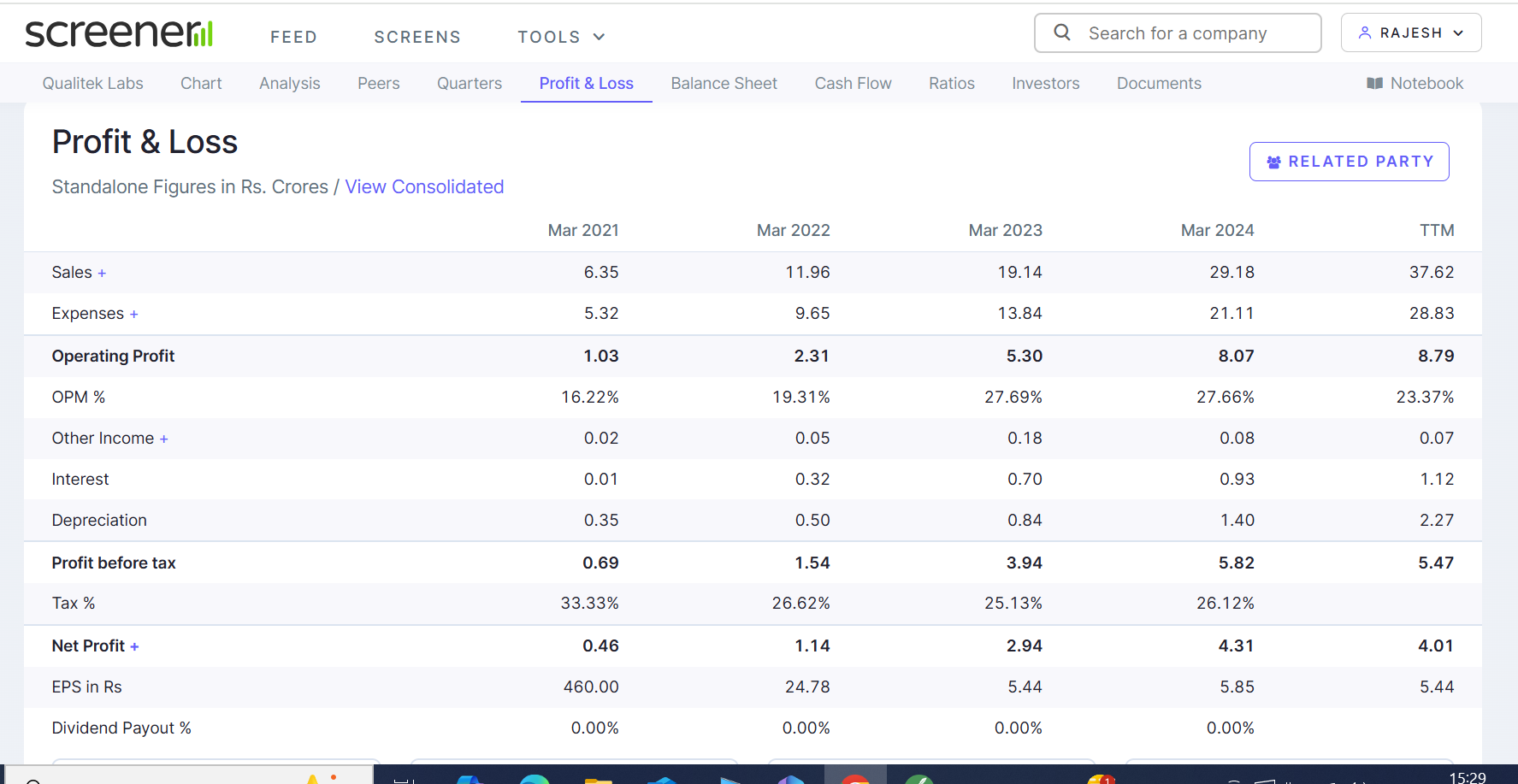

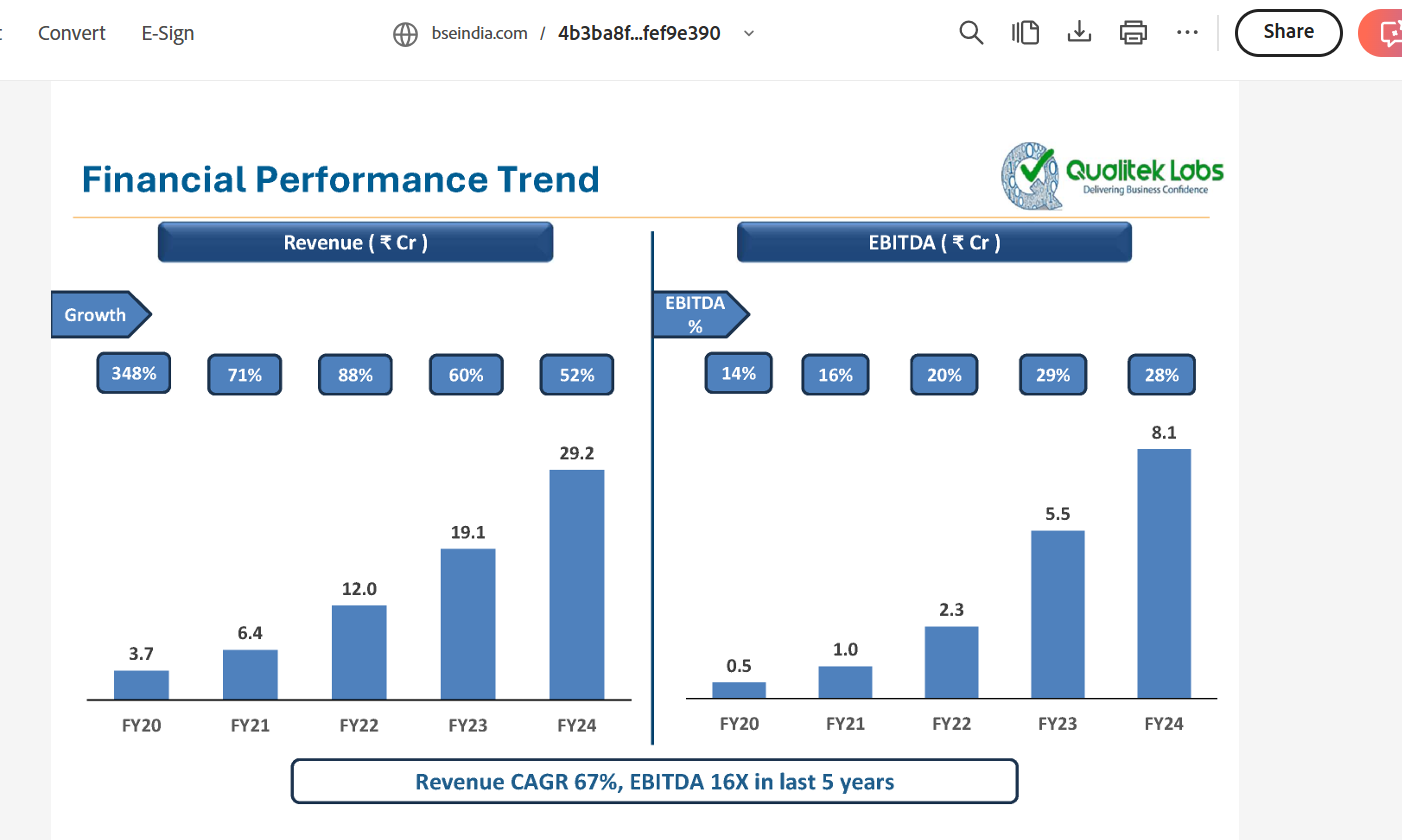

FINANCIALS:

Standalone financials of Qualitek is impressive;

Growth rate has been impressive for last five years;

By the end of this financial year, the company will be able to acquire ITC Labs and shall be reporting consolidated numbers. The management has guided 90 Crores revenue in 2025 and 120 Crores revenue in 2026 on consolidated basis.

H1- 2024-25:

On a standalone basis, qualitek revenue is almost 21 crores, with net profit of 1.7 crores. Margins have been under pressure in H1 as two labs are being created in Noida and Bhuwaneshwar with pre operative expenses. The management has explained the same in the investors presentation.

4b3ba8fd-929c-49c8-af7c-c4f7fef9e390.pdf (3.2 MB)

Management has further reported that in the existing lab in Pune and Bhuwaneshwar, EBIDTA margin has improved by 1% point.

They are expecting revenue from Noida Labs from Q4-2024-25 onwards and Mineral Testing Facility in Bhuwaneshwar from Q1-2025-26 onwards.

Investment Thesis:

- Industrial testing companies are supposed to have moat and they are able to operate on decent profitability. However, we do not have any listed peer in Indian Stock Market. Comparision with Bureau Veritas is not fair. However, it can be seen that the company, though operating on a very small scale is opearing at 25-30% EBIDTA in the last few years. I expect them to maintain EBITDA around 25%.

- In a developing economy like India, society is becoming more conscious of health and safety hazards, environment, quality, durability etc. giving a tailwind to testing and inspection companies.

- With acquisition of ITC labs, software company and various expansion plan; the company is likely to get a scale and operational efficiency. Further, the business looks scalable. Promoters are in this field for last many decades, and they can execute the plans.

- Though the valuation look stretched as of now, on projected revenue of 120 crores in FY 2026, with 25% EBIDTA; valuation looks okay.

RISK FACTORS: - ITC Labs has lower profitability. The management is expecting to improve its profitability, which they may not do.

- Valuation looks stretched without much margin of safety.

- Company has already seen a sharp upside and deep correction cannot be ruled out.

- The company has ambitious growth plans, and will need huge capital outlays for financing such growth.

- Micro cap stocks are risky by nature and one can lose 100% of invested capital.

[Disclosure: Invested and Biased]