Executive Summary

The stocks of Alexion Pharmaceuticals (ALXN) is undervalued and worth investing on the following grounds:

• Quarterly increase in stock value is 23%.

• Return on research capital is 6.2 which keeps it in top three performers.

• Liquidity situation is more than satisfactory.

• Profit margin is 34% which makes it at the top of the list.

• Price Earnings ratio is comparatively low.

Overview:

In 2019, the US remained the world’s largest single pharmaceutical market, generating about

$490 billion of revenue. Despite being solely a 0.2% increase from the previous year, the US

market accounted for forty eight percent of the worldwide pharmaceutical market.

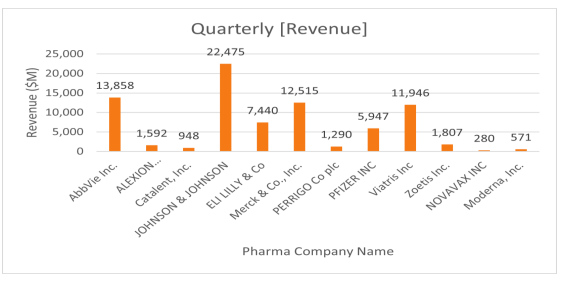

Top US pharmaceutical companies by revenue during the last quarter of financial year 2020:

• Johnson & Johnson — $22.5 billion.

• AbbVie — $13.9 billion.

• Merck — $12.5 billion

• Viatris Inc — $12.0 billion.

• Eli Lilly — $7.4 billion.

KEY FINANClAL METRICS

Portfolio Quarterly Analysis:

According to the portfolio result indicated in the column “Quarterly % Change”, it is evident

that the stock value has been increased by 35%, 25% and 23% in favor of Eli Lilly & Co, Novavax Inc and Alexion Pharmaceuticals Inc respectively.

RORC (Return on Research Capital):

Return on research capital could be an element of productivity and growth since analysis and

development is one among the ways that firms develop new purchasable merchandise and

services. This metric is usually utilized in industries that trust heavily on R&D, like the

pharmaceutical business.

The RORC (return on research capital) is that the quantity of profit earned against the amount

spent on research and development at any given intervals (usually a year). This is calculated as current gross profits (typically found on the present year’s financial statement) divided by the previous year’s R&D expenses.

The previous year’s R&D expenses area unit used because of the payoff is not usually complete like a shot. Rather, it is usually complete in some future purpose in time. One will fairly assume that higher returns mean that the corporate has spent sagely in terms of research and development and is getting the financial benefits from its struggle.

We can observe from the data available on Research and Development Expenses for

pharmaceutical companies, Johnson & Johnson spent 12.2 billion dollars, 9.9 billion dollars by Merck, 8.7 billion dollars by Pfizer and 6.4 billion dollars by AbbVie during the financial year

2019.

These amounts seem to be impressive on individual basis but when compared to their respective RORC, all these pharmaceutical companies are showing positive performance. On point is to be noted here that top pharma giants such as Johnson & Johnson, Merck and Pfizer

which are indicating below average positive performance. So far as this financial indicator is concerned that Zoetis (RORC: 10.1) and Perrigo (RORC: 9.7) and Alexion Pharmaceuticals (RORC: 6.2) are top performers.

This analysis is made expressly on annual figures because research expenditures are normally incurred on long term basis and especially its impact cannot be seen on quarterly basis.

Market Capitalization:

Johnson & Johnson, Merck & Co, Pfizer, AbbVie and Eli Lilly are dominating the pharmaceutical industry in United States. They have invested 411.4(JNJ), 207.0(MRK), 205.3(PFE), 189.2(ABBV) and 169.8(LLY) billion dollars respectively according to the last quarter of the financial year 2020.

Liquidity Position:

As per the data and graph available on Quick Ratio, the liquidity position of the major pharma companies is rather delicate. The normal yardstick for this financial indicator is 1:1 but the figures are showing less than 1 for main companies for example Johnson & Johnson (0.6),

Merck and AbbVie are also both at 0.6. Pfizer and Viatris have quick ratio as (0.5).

Alexion is indicating 2.7 as quick ratios which seem to be high. This shows that the liquidity

situation is more than satisfactory, but this may also give clue towards unnecessary liquidity residing in the company.

Risk and Reward Relationship:

Return on equity is exceptionally high for Eli Lilly (38%) which can be explained by high total debt to equity ratio (2.8). Higher amount of debt can increase the company’s profit margin and ultimately more funds available for distribution among the shareholders. But at the same time, the credit risk associated with such type of investment strategy can also not be ignored.

ROE figures for Catalent (5.3%) and Zoetis (9.5%) are also indicating high returns. Catalent is performing well keeping in view the fact that the credit risk is low (total debt to equity ratio

0.9). On the other hand, Zoetis is taking comparatively higher credit risk (1.9).

Profitability Aspect:

The gross profit margin in pharmaceutical industry seems to be relatively high for most of the companies ranging from 56 to 90 percent except for Catalent (35%) due to their excessive cost of production.

The top performers under this financial indicator are Alexion, Eli Lilly and Zoetis having profit margin 34%, 29% and 20% respectively during the last quarter of financial year 2020

NB IXBRLANALYST allow users to do this Analysis easily on excel

Valuation Analysis:

Four types of valuation techniques were used to compare the worth of each pharma company selected. Enterprise Value was compared with Revenue, Gross Profit and EBITDA (Earnings before interest, taxes and depreciation) figures of these companies. Price Earnings Ratio is equally calculated.

These calculations can be consulted from the table under heading

“valuation” and the relevant graph is also available for appraisal. Then, these figures were compared with the average figures calculated for pharma industry at the end of this template.

The companies (Merck, Pfizer, Novavax and Moderna) have negative EV/EBITDA ratio which means that they have enough net cash to pay off all debts and can buy back all its stocks, if needed. But at the same time, these companies have negative price earnings ratio which demonstrate bankruptcy risk, if the situation remains consistent.

There is another point to be noted that these companies have already signed an attractive contract for the delivery of covid-19 vaccine with US Government and the demand for this medicine will remain intact in near future, thus there is possibility that PE (Price/Earnings) ratio may become favorable in incoming period.

Alexion Pharmaceuticals is another company which needs to be observed. Its stock price is

low as compared to its earnings which is evident from low PE ratio when it is compared with the average figure for pharmaceutical industry. Enterprise Value/Revenue is also on the lower side when compared with its industry figure. This makes Alexion’s stock attractive.