Pyramid Technoplast –

Pyramid Technoplast is the company incorporated in 1997, situated in Malad, Mumbai. Involved the manufacturing of containers for APIs, Pharmaceutical products, Chemicals, Liquid food storage (Vegetable oils), personal care products (shampoos), Industrial products (Paints, adhesives), etc.

The company IPOed in August 2023 at a price of 150 against the current market price of 140

The IPO was mix of both Fund Raise + OFS, the IPO was structured as the maximum permissible stake is kept with the promoters (almost 75%) and the stock is listed.

Fresh Issue – 55,00,0000 Shares where as OFS = 37,20,000 Shares (Credence Financial consultancy LLP)

Promoters – Agarwal family

The company has 3 main divisions –

1. HPDE Drums:

HDPE drum is High-Density Polyethylene drum. These Drums are made from high density polythene HDPE is a type of plastic known for its high strength-to-density ratio and its resistance to many different solvents, making it commonly used for containers like drums. HDPE drums are often used for storing and transporting various liquids and chemicals in industries such as chemicals, pharmaceuticals, food and beverage, and agriculture.

The HPDE drum is more of a commodity product – Why?

The process of manufacturing is Just 2 steps process –

- The process begins with the procurement of raw materials required for manufacturing HDPE drums. This includes sourcing high-quality HDPE resin pellets, which are the primary material used in drum production. Resin pellets are typically purchased from chemical manufacturers or resin suppliers.

What are HPDE Resin Pellets - HDPE pellets are small granules of HDPE resin.

What are HPDE Resin - HDPE resin is a type of thermoplastic polymer produced from the monomer ethylene. It is known for its high strength-to-density ratio

So the Harmful chemicals which can even burn through our skin, will not cause harm to the drum Just because of the above HPDE chemical chain

HDPE resins are typically produced through a process called polymerization, where ethylene molecules are chemically bonded together to form long chains of polyethylene molecules.

- Inject Molding - HDPE resin pellets are melted and injected into a mold cavity under high pressure. The mold is then cooled and opened to release the newly formed drum.

Why is the above commodity product any changes in the price is passed to the customer increase/decrease meaning that the margins remains constant but the increase or decrease in RM won’t benefit company

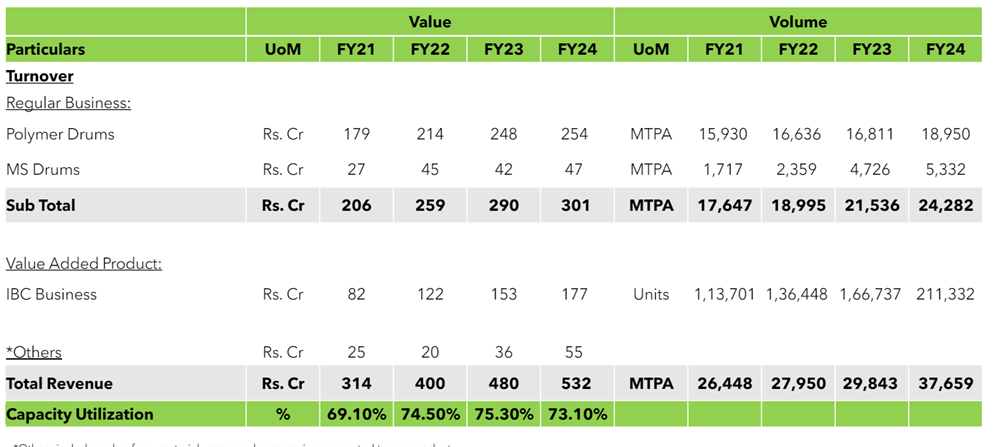

Total capacity for the company 450,000 drums per month so around 5,400,000 drums per year

2. Intermediate Bulk Container (“IBC”):

IBC is a value-added product for the company due to various reasons –

- IBCs are often designed with features like built-in pallet bases and forklift pockets, making them easier to handle and transport compared to individual HDPE drums. This can lead to efficiency gains in logistics and reduce the labor required for loading and unloading.

- While HDPE drums are durable, IBCs, especially those made from materials like steel or composite materials, may offer greater durability and resistance to damage from handling, stacking, and environmental factors. This can result in longer service life and reduced risk of product loss or contamination.

- In some industries, IBCs may be preferred over HDPE drums due to regulatory requirements or industry standards for handling and storing certain materials. IBCs may offer features such as UN certification for hazardous materials or compliance with food-grade standards for storing food products.

Let’s understand the manufacturing process –

- Raw Material - In some industries, IBCs may be preferred over HDPE drums due to regulatory requirements or industry standards for handling and storing certain materials. IBCs may offer features such as UN certification for hazardous materials or compliance with food-grade standards for storing food products.

- Composites - involves combining the prepared materials to form the composite structure of the IBC. This typically includes techniques such as hand lay-up, filament winding, or compression molding, depending on the desired properties and design of the container

- Curing - IBC undergoes a curing process to harden the resin matrix and bond the fibers together. This may involve heating the composite to a specific temperature and applying pressure to facilitate the curing reaction

- Assembly – Once the components of IBC are fabricated and cured, they are assembled to form the complete IBC. This may involve joining the container body with the pallet base, installing fittings, valves, and closures, and any other components required for functionality and performance.

Company has the product range of producing the composite IBC ranging in the capacity from 20 Liters to 1000 liters

The company has undertaken a huge capex in IBC 240,000 units the total capacity will be 600,000 units

FYI the total sales volume of IBC around 210,000 Units Refer below exhibit

Good thing about this business is that they are majorly focused in domestic business major competitor’s capacity in IBC is outside India, their major focus is not in India, hence there isn’t much divergence in terms of the winning over the customer.

Good thing about this business is that they are majorly focused in domestic business à major competitor’s capacity in IBC is outside India, their major focus is not in India, hence there isn’t much divergence in terms of the winning over the customer.

IBC is far more superior than metal and HPDE drums à this results in better margin profile for the company, however the same is more useful and adds value to customer also à IBC although costly is used majority for exports, sometimes it’s the demand from the buyer’s end to supply the product in IBC only

The IBC supplied can’t be shipped back to India reason being the cost. à the customer of the company is forced to sell IBC to local player à however, the return on this whole exercise is higher than that of Plastic drums since the resale value is far superior in IBC

Gestation period in IBC is also very high

Refer below Exhibit

3. Metal Drums:

Metal drum business is very little in comparison to the whole pie, however the margins and realization on metal drums is far better than HPDE drums due to their capacity of holding the high volume of liquid than your normal HPDE drums,

The current capacity of 50,000 units per month is expected to be increased to 90,000 units per month the mix is such that the company expects the % of revenue from MS drums to be around 10% of FY26-FY revenue

not very excited about this business → very low PBT margins hence management tends to keep the same at very low level of total business

General Info

The company has the total of 8 Manufacturing facilities:

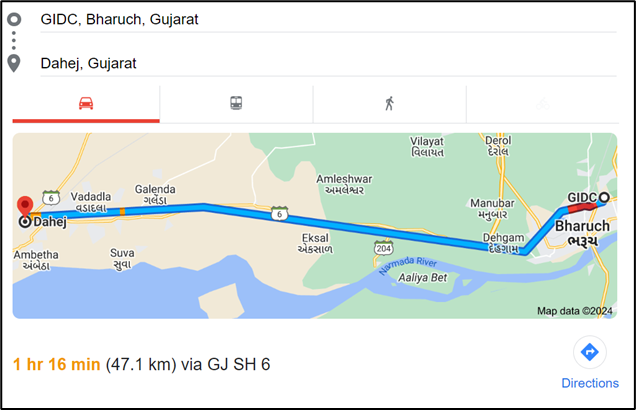

Majority of the same located in GIDC Bharuch, the reason being that the clients of the company requires them to be as close as possible to the factory of theirs

Dahej being the hub of Chemicals, the major clientele of the company is situated there

See the SS below, the Approx distance between the Factory and Dahej is mere 47 Km.

The above thesis can be confirmed by the below exhibit also

Let’s understand the moat – The chemicals and pharma industry is highly regulated industry – We can’t just wake up one day and decide to be the supplier to one of the company in this industry as one F up will lead to the client facing huge regulatory licenses and sometimes even losing the major client.

The APIs, Pharma products or Chemicals handled by this packaging material is highly dangerous and hence you won’t at least appoint the new supplier as your vendor partner.

However, that being said as said earlier that the manufacturing process of HPDE is very simple hence we see immense competition from various small unregulated players + HPDE depends upon the RM derived from crude oil any volatility takes on the hit on inventory + margins in fact that’s the reason even why companies like Time Technoplast even compounded the sales growth at mere 13% butt they are also moving from HPDE/metals to IBC (“Value added products").

What makes this situation different is IBC

Asset turnover across the company is 5x, the IPO of the company was undertaken for the purpose of repaying the WC debt and normalizing the cycle + Paying of the debt used for the expansion in line of IBC in the past (See the exhibit below)

Pipeline for Growth -

The capex to be undertaken for Unit 9 – is worth around 40 Crores – 50 crores where the asset turns are approx. 5x

Optionality might play out in metal drums too Metal drums can be used as a substitute for plastic drums reason being at the almost similar price metal drums have bigger holding capacity than the plastic drums

Operating leverage in play the current capacity utilization is in 60s, with new capacity coming live better capacity utilization will result in better absorption of the fixed cost and better margins overall Source Maiden Transcript

The capex to be undertaken for Unit 9 – is worth around 40 Crores – 50 crores where the asset turns are approx. 5x

Optionality might play out in metal drums too Metal drums can be used as a substitute for plastic drums reason being at the almost similar price metal drums have bigger holding capacity than the plastic drums

Operating leverage in play the current capacity utilization is in 60s, with new capacity coming live better capacity utilization will result in better absorption of the fixed cost and better margins overall Source Maiden Transcript

Management expects the same to be in range of 8% - 9%. This would also rise due to change in the products mix increasing revenue from IBC and decreasing revenue from Commodity products (Refer Exhibit below)

My Investment thesis

What makes this investment compelling

Not a huge believer in guidance since there are only 2 people who knows what’s going to happen, God and a Lier

And hence I don’t prefer taking buy/sell decisions on guidance.

However the guidance and actual performance can be a good Quantitative matrix for judging the management capability

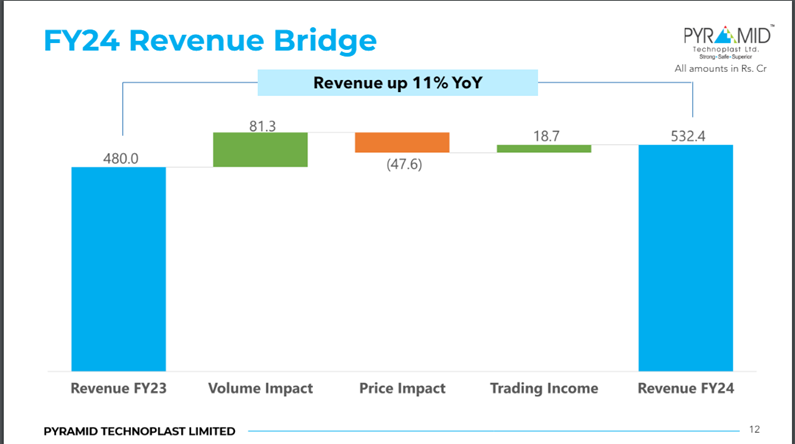

Going through the concall I noticed they gave the soft guidance of approx. 30-32 crores of bottom line and 550 odd crores of Revenue for FY 2024.

They achieved the same efficiently.

Question than why is the business still available at 1x Sales – ??

Refer below exhibit

Above is the price of one of the main RM of the company has been in downtrend due to which immense increase in volume the company has been able to increase the top line in the same pace major contributor is HPDE which is pass through hence this RM decrease has to be passed through resulting in decreased EBITDA and PAT

If it were not for the price erosion the incremental growth could have bee 50% i.e., 30% against 20%

With increase in IBC revenue the same should at least stabilize with low volatility for the company

Even today the management is quite confident in terms of Volume

- Even though the margins in HPDE are low the only way to increase is by the way of better utilization of capacity + or decrease in the cost

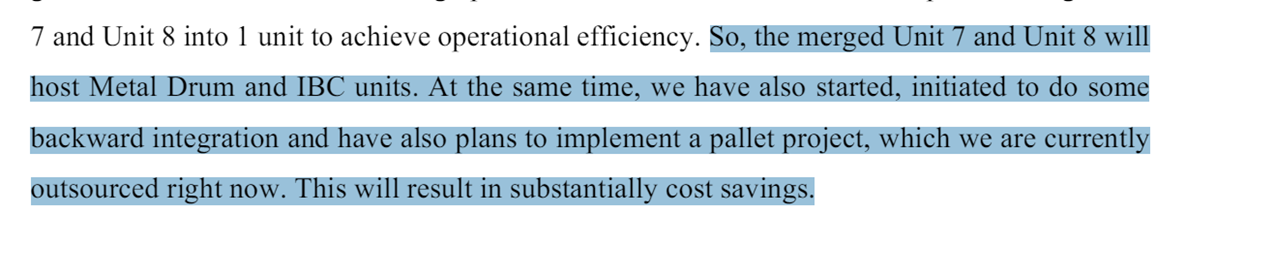

The company ventured in backward integration by undertaking the pellet production used in plastic manufacturing this Pallet will be used in IBC adding the incremental margins for the consolidated entity

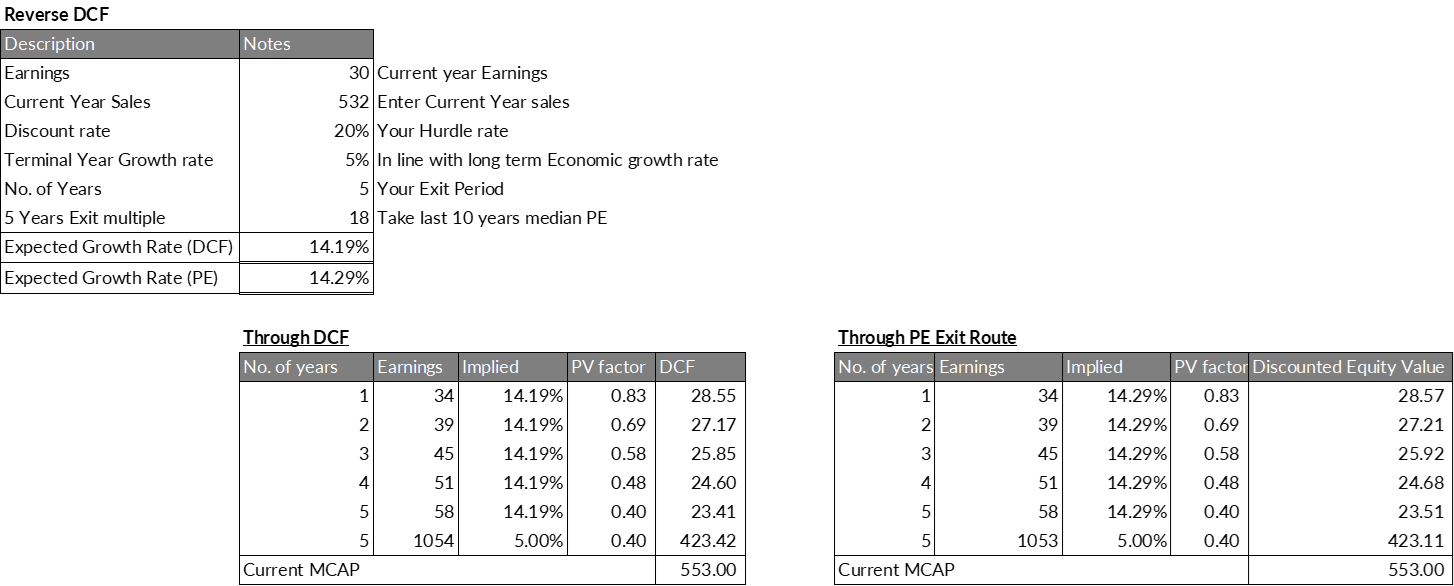

Implied earning growth required is merely 14% inline with large cap company’s growth for your investment to grow at 20% keeping in mind no margin expansion no product mix is taken into account, that’ll be cherry on top, have not taken as putting money you have to be conservative as possible. The current scenario is the most bearish I can be

Please note this is a bear case scenario, management inputs are as below

Summarizing the thesis → Increasing volume 20% YoY but margins and realization impacted, RM reverting to mean + Capex coming live + better capacity Utilization can turn fire in forest fire

One Anti thesis → Time techno their close competitor is starting IBC facility in India too,

They were highly focused outside india, keeping in Account India’s total capacity for IBC is very very less only 800,000 currently (Source: Q3 Concall) can the oversupply play out?

In that case your VAP becomes Dud

Something to think about

Disclaimer - Invested and consider me baised