The company needs to find a right balance between ticket pricing and occupancy. By keeping ticket prices in check the higher occupancy may offset the variable contribution or perhaps add by way of higher food and beverage sales.

Am sure the company must have worked out all this.

The major issue in last 2 quarter seems to be lack of good movie content.

PVR-INOX earning call notes

this was the first earning call from combined entity PVR-INOX after completing merger in march.

PVR-INOX has 1689 screens across 361 cinemas in 115 cities, largest multiplex chain India by miles. Co decided to shut down 50 odd screens in next 6 months, which are loss making and malls located are at end of their life. Will open 150-175 new screen in FY24.

Reported revenue of 1165 crore with EBITDA of 27 crore and 286 crore loss in PAT. This acounts for one time write off of 160 crore from deferred tax/merger expense/and screen closure(?). foot falls of 3.05 crore for FY23 quarter and 14 crore for full FY23. Pre-pandemic footfalls were around 17 crore for PVR+INOX.

New screen openings will be with focus on profitability, try to capture quality shopping centers in most of the cities. holiday period for rental cost is over, back to pre-covid contracts. Advertising re venue well below pre-covid levels, down by 30 percent.

Company breaks even on EBITDA basis with occupancy around 22%, with synergies from merger this could reduce to 20-25% in few quaters. Pre-covid occupancy was around 30-35%.

ATP has gone up 16% and SPH is 30% from pre-covid.

In my view, biggest negative for multiplex buiseness is they are not in control of their topline, this is completely depend on movie box office. PVR-INOX has struggled in FY23 due to weak content - mainly in Hindi circuit with low number of release + only handful of success. I think this will continue for Q1 FY24 as well, with Adipurush being only big tentpole hindi release pending. Hollywood calendar is packed for June, so this might help a bit.

Real test for me is how Hindi circuit will improve from Q2FY24. If they can meet their FY24 capex goals with internal accruals, then company will be in good shape, Debt/Equity ratio should be key monitoring criteria going forward.

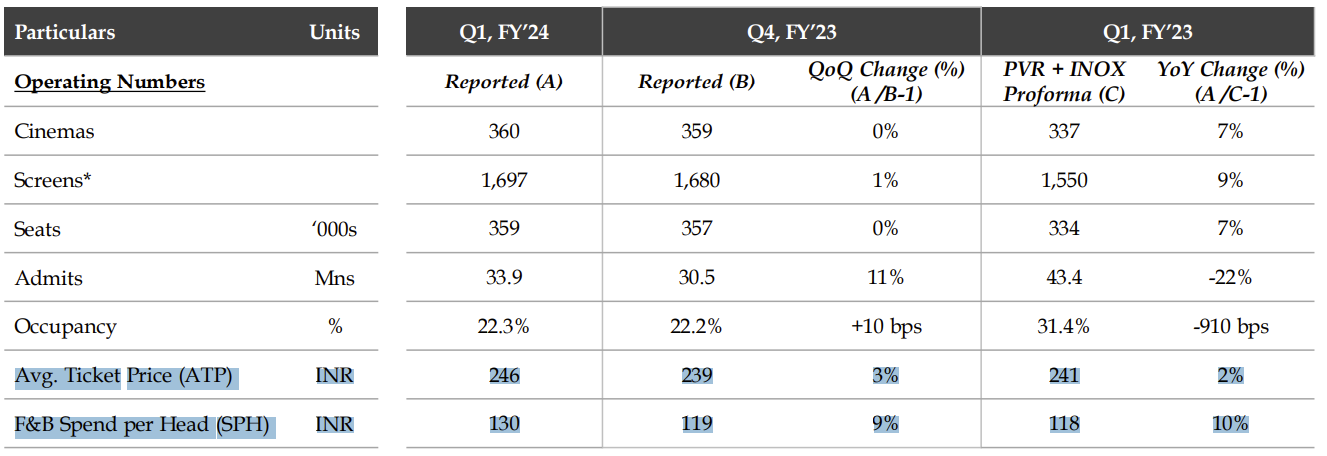

PVR INOX Q1 FY24 Earning updates

Another weak quarter from PVR-INOX, 1324 Cr revenue, 100 Cr EBITDA and -44 Cr PAT.

Improvement visible on QoQ basis, helped by strong perfomance of hollywood movies.

Footfalls improved by 11% QoQ, ATP up by 3%, SPH up by 9%. Advertising revenue is still subpar

July numbers looks much better, expected to have strong results in Q2 &Q3.

Expansion is on track for FY24, will add about 170 screens.

40-45% of new screens are in South India, entering smaller cities along with metro markets.

What is interesting, is that even though that Cineline focus more on Tier 2 cities. Still they have a comparable Avg Ticket Price (ATP). Though F & B spend (SPH) is lower which is understandable.

Then I went for a deep dive in analysis of Cineline & found this interesting video :

Ma’am @WomenInvestor , am new on the platform, I have a question :

Do you think, considering the size of both the businesses, are the numbers really comparable.

Are these really apple to apple. I mean the no of screens mentioned above is 1697. Cineline is no where close to it. Also, what was interesting was the occupancy %. Now, PVR being a such a large brand, does a occupancy of just 22% really justifiable.

You are right. Numbers cannot be compared. PVR is 16,000 crores in M.Cap while Cinepolis is Rs. 300 crores.

@WomenInvestor is suggesting here that expenses for a consumer is almost similar between the two and she is basing her analysis on that. It’s a good way to think.

Secondly, your question on occupancy - yes at 22% it is justifiable. Because one has to consider the sector has recently come out of a war between consumer’s preferences due to OTT platforms and covid-19.

As discretionary spends will increase, people will prefer experiences in the form of movies and sports on a big screen. Plus, there’s a set of ‘feel’ to it that is not possible at home.

It will be interesting to track the subscription model on movies and food going forward. If they can crack it right, they have the potential to do really well because they already have the screens in place.

Not thinking ahead makes one prone to errors of judgement… lack of big ticket releases owing to the cricket world cup in the first half of Q3 and the actors strike in hollywood notwithstanding, we have salman and ranbir to shake things up from mid november… I am not too gung-ho about the 699 monthly plan as upon reading the fine print it has a lot of ifs and buts… but well tried to the company management…

As long as good content gets generated this appears to be a reliable money making machine, post merger it has higher market share and caters to the luxury, premium and now with tweaks in f&b and rationalizing of ticket prices, attempting to tap the value seeking customers as well… for me, this dip appears to be a perfect opportunity to add positions for bigger targets … I am pre-empting an INHS in the weekly charts and as always, prone to pulling the trigger before time

The stock is down from 1800+ to 1450. Straight 20% cut in less than 2 months. During the initial phase of fall I thought it has something to do with rising COVID cases and controversy related to Salaar vs. Dunki.

But both the above issues seem to have faded. Puzzled over the price action

A different take on PVR’s prospects from top down perspective. I am not invested in PVR stock or have any opinion about it. But I like tracking this stock given that I am a movie buff.

PVR’s revenue consists of 50% in movie tickets, 30% F&B and rest miscellaneous (advertising etc). At first glance it may seem that they have diversified revenue stream but it’s all actually driven by a single factor- customer footfall. So if a movie is flop it will impact revenue in all the categories.

Their current one year trailing topline is 6000 crores so for them to grow at a modest rate say 15% rate, they need to be pulling in around 900 crores next year, 1000 crores year after and so on. PVR-INOX combined accounts for 40% of total screen revenue in India, so the total market also needs to grow by 2000 crores next year, 2300 crores next year and so on. Which means there has to be at least 4-5 massive blockbusters every year to generate that kind of total market revenue.

Stock did well last quarter because we had some mega hits in the form of Jawaan, Pathan and Salaar, each doing 500-600 crores business in india. But this quarter has been quite lackluster so far with none of the big releases (e.g. Fighter) bringing solid ticket sales in india. So clearly market is waiting for another spate of blockbusters.

In addition, PVR’s presence in South is mostly limited to Karnataka with small market share in Tamil Nadu and Andhra Pradesh, which have produced most of the blockbusters. Also competition there from single theaters is quite tough and state regulations prevent PVR from taking price hikes.

I believe this is what makes taking any long term call on PVR so difficult. They have absolutely no control over the quality or quantity of the products they are distributing while carrying a high fixed cost. The fact that these days all the blockbusters are available on OTT within 2-3 weeks of their releases is also a dampener.

So 2-3 mega hits are what PVR stock needs right now to trigger a fresh rally.

Thanks for your detailed response. Agree with all the points.

As regards 15% growth - this need not come only from growth in box office collection but also from additional screens. PVR has been adding 4-5 % (net) screens every year.

It needs about 5-6% growth in either footfalls and/or box office collections and a 2-4% price increase.

But yes quality of content is the main ingredient for PVR success.

Additional screens will contribute to box office collections. 15% sales growth is a reasonable performance you would expect from small-mid cap stock.

When a movie makes 500 crores you don’t care if it was because of higher ticket price or higher footfall. Point I was trying to make is that growth needs to come from an expanding pie of the overall market. And in this case continuous supply of blockbusters is what expands the pie.

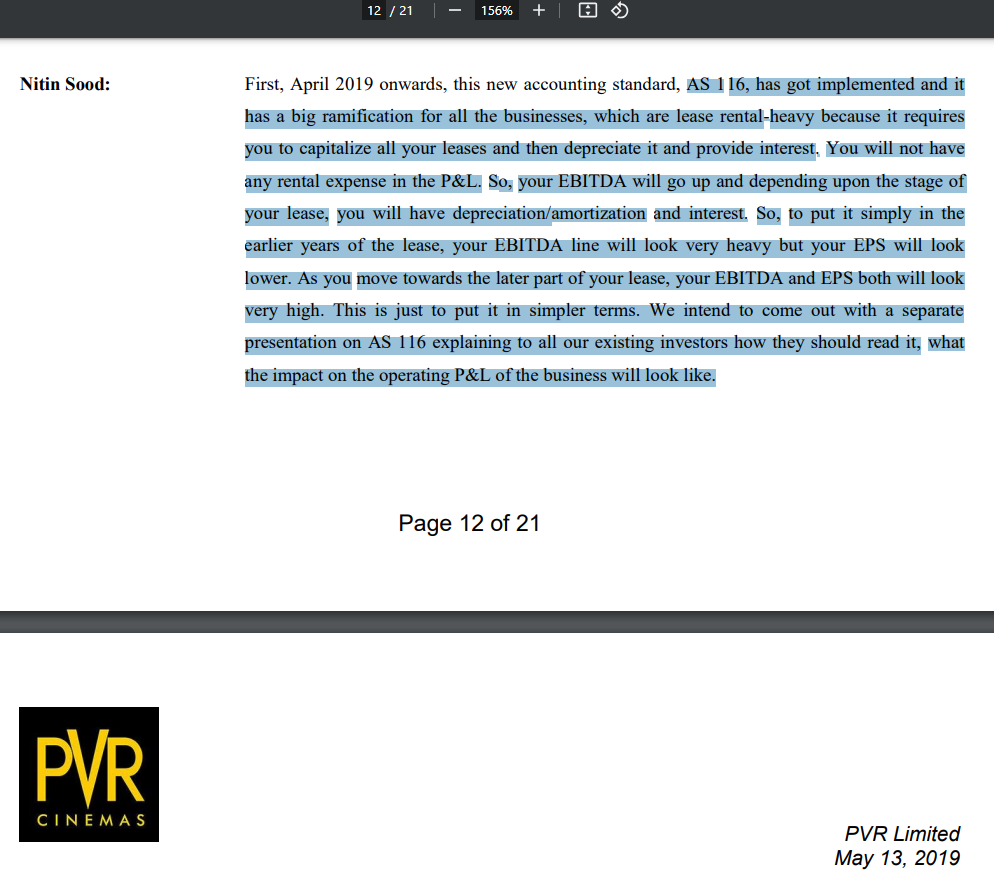

Have a basic question,may be some finance practitioners can help to understand. Why the depreciation cost is always higher? Most of the time it’s > 50% of the operating profit. Is that because of their ongoing capex/expansion? If so will it settle at some point in time? Thank you.

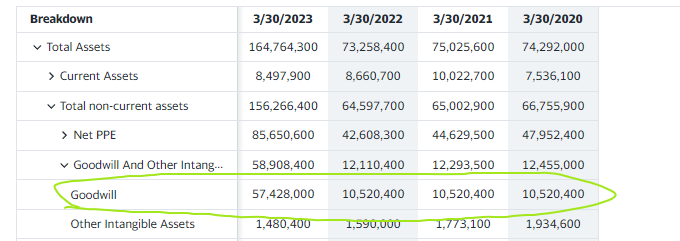

Company Goodwill is increasing to the point it is 1/3 of Total assets. Couldnt find management reasoning on this in the transcripts of last 3 calls either. If someone has any explanation on this. It will be greatly appreciated.

Both interest and depreciation cost will be high due to requirement to capitalize lease costs. This artificially depresses earnings and inflates P/E.

Trent is another example where you see high P/E due to similar accounting requirements as most of their stores are leased.

Only thing which bothers me and need clarity on is - Company is of Rs 12,000 Cr having debt of 8000 Cr. PVR’s total 5 year Cash from operation is Rs 2235 Cr . From where it gonna pay this huge debt where there is net profit.

Im optimistic here by taking cash from operation because company has to pay interest and compnay has to improve there theatres no matter what.

On that 8000cr number, roughly 6500cr is the lease rental (300cr quarterly run rate of rent as of Q3FY24) which leaves 1500cr odd borrowings at 9% (35cr/qtr interest payment) which is fairly manageable for them to service.

My bigger issue with this company will always be the lack of control over the content pipeline which is keeping me away from it.