@sujay85 - Will check Crompton greaves Consumer too when time permits and evaluate against Havells India.

@Investor_No_1 - You can use valuereasearchonline which gives cagr returns even for SIP Investments.

Regards,

Puneet

@sujay85 - Will check Crompton greaves Consumer too when time permits and evaluate against Havells India.

@Investor_No_1 - You can use valuereasearchonline which gives cagr returns even for SIP Investments.

Regards,

Puneet

Use XIRR function in excel. Check this: https://economictimes.indiatimes.com/wealth/invest/how-to-calculate-returns-on-sip-of-mutual-funds/articleshow/53841350.cms

What is you criteria for exclusion?

@karthik_kamath_ - There are multiple factors which i review quarterly and yearly include top line, bottom line, ROE, ROCE, Debt, Change of Management and most importantly company industry performance as a whole based on which i gradually move out of the stock or stop allocating additional funds.

Lupin - I had stopped SIP i had stopped at the right time (2 Years back) fortunately as stock didn’t had any trigger and was getting battered due to USFDA inspection and as a whole pharma industry is struggling from 3+ years now !

Kajaria - The unsold inventory of real estate completely hints that stock dependent on real estate will also face the burnt including tiles.

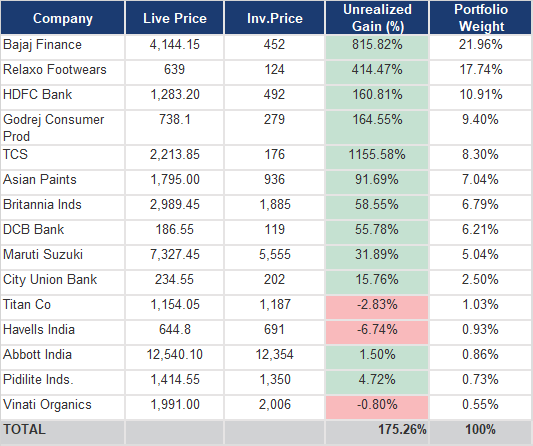

One thing which i want to learn from this community is how to put large portion of cash as i have multiple stocks which are 5x (Realxo), 6x (Bajaj Fin) but since i could put only 50% of cash i always feel left out

Regards,

Puneet

I would like to ask. You started SIP in 2013, how did you go about taking a decision to invest at that time when the market was dull. And not later when the market was bullish. This is a remarkable quality which most investors do not possess. Which I think is the biggest hindrance in being a long term investor.

Also great methodology: Selection of leaders makes your PF resilient. Sound sleep, normal BP.

DCB is a misfit. If you must have a bank, find a replacement like Bandhan or IndusInd.

In fact, DCB, Vinati, City Union could be traded out for Gold ETF. Having 10% in Gold is wise.

“One thing which i want to learn from this community is how to put large portion of cash as i have multiple stocks which are 5x (Realxo), 6x (Bajaj Fin) but since i could put only 50% of cash i always feel left out”

Pls rephrase. To better understand the issue at hand.

Are you saying this because its a smaller bank? If so, then why not suggesting HDFC or Kotak Bank?

DCB comes across as a bank which is not future ready. There are better options in the same small category. Even IDFC-First is ok.

Any reasons why CUB is a trading bet? AFAIK, CUB’s NPA numbers are most trustworthy across all banks. New gen pvt sector banks under report NPA as there is incentives for performance for executives over there. CUB is a well managed bank, I feel not being a future ready, is one way a moat

Well, put.

New Age banks are under performance pressure. One has to be selective.

Yes. City Union Bank is well managed enterprise. But, the sector is currently expensive. Banks are far from good value. This is the reason why Nifty is holding ground.

Can you elaborate your statement that DCB is not future ready. Sorry for my ignorance, I did not understand.

@jamit05 - Typically i don’t look out which level market is if i am going with a SIP methodology for stocks and i did same during 2013; my SIP would have continued from Jan, 2018 to July, 2019 had i not faced an unexpected event in family. I have planned additional funds for emergency and plan to continue with my SIP’s as i have faith and believe in Indian economy which hopefully should turn around in another 2-3 quarters (If there is no prolonged recession) as the base top and bottom line itself will become 50% of what it was 3 years back !

Since i have to devote a lot of time to work and family which most of us do, i don’t plunge too much in small/midcap rather i let fund manager do the same on my behalf by buying aggressive small/midcap mf’s (Direct Plan).

What do you mean by DCB as Misfit ? Is there any particular parameters which you are referring to ? I wanted to have a small bank which will grow faster due to small base and have negligible or less NPA’s with a credible management. Both CUB, DCB fit into this criteria and have given good returns in last 3-4 years.

DCB had fallen on face 5 years back when it had announced to double its branches in 2 years timeframe and stock came down from 130 levels to 75 bucks which is when i loaded truck load of DCB’s followed by monthly SIP’s

Gold is definitely a good hedge … but i have never been fan of the same. Will analyze and come up may be with 5% of total allocation.

Relaxo and Bajaj Fin investments were for my house interiors as i had expected 2x in 3 years but they started performing amazingly well and i couldn’t sell any of them. Since i had additional cash at that time, i should/could have deployed more to both stocks. My dilemna is kinda FOMO which should overcome by SIP’s which i have kicked Off again in the best market times (Lot of correction done and another led expected) …

Cheers !

Puneet

@jamit05, i never liked IDFC and IDFC Bank due to its NPA’s and focus on infra projects when it was launched. Not sure about the current portfolio of bank apart from Infra project financing. If you look at the returns of stock in last 3 years it is nowhere comparable to DBC, CUB.

IDFC Returns - 3 Years ( - 10%)

DCB Returns - 3 Years (20%), 5 Years (20%), 10 Years (18%)

CUB Returns - 3 Years (20%), 5 Years (24%), 10 Years (28%)

Above are CAGR Returns and not absolute returns and not a criteria to buy/sell a stock; it is just a comparison of returns and yes there are other financial parameters and investor interest which takes stock to higher levels and consistent returns.

Kotak, i will study and see if it gets a place in my portfolio as i already have HDFC B, Bajaj Fin, CUB, DCB.

Cheers !

Puneet

For banks, I think the following points are to be compared.

NPA

Cost of Deposits

Net Interest Margin

RoA

DCB falls short on all these counts to Indus Ind (and Kotak, HDFC Bank too)

Aside from that, I want to highlight, while I applaud, the fact that you narrowed down to a good stock like DCB, waited for a good correction and then got in. This is remarkable.

When a good company is facing temporary bad news, which the management can tackle in a few quarters, due to which the stock price falls, that is a great time to get in.

I say DCB is a misfit, although it is run by a good management, because you have chosen the top stocks in other sectors, then why go for the second rung in banks.

It is not so much work. Just a few hours a week. I say this because fund managers cannot tailor fit your investments.I mean, if you consider yourself good and disciplined investor then there is absolutely no reason to employ a fund manager whose targets and criteria for making an investment is very different from yours.

I would not count on a recovery anytime soon. But, that is a part of an investors journey. Nifty PE is still at 26. And most stocks on my list are still far from their normal valuations. I feel there is plenty of downside room, which could quickly get filled if there is an international event or could take its sweet time and drag along.

However, overall I think you are a long term winner. Your approach to investment via SIP and that too only when the market has well corrected is a sureshot method. Kudos to u.

Gold is definitely a good hedge … but i have never been fan of the same. Will analyze and come up may be with 5% of total allocation

Gold is not only a hedge, but assuredly gives 8% CAGR over the long term. And in times like these, you won’t be disappointed.

In fact tell me, do you think its a good time now to do reverse SIP in stocks that are at the very top and giving good profit? And divert the investment into scrips that have corrected or Gold or some dirt cheap dividend giving PSUs?

DCB has good numbers, the management apparently has things under control. But, future growth is a key distinguishing point.

Some private lenders and banks are future ready.

IndusInd (great numbers)

Bandhan (good growth prospects, as its business complements HDFC, its partner)

and even Yes Bank at Rs.50 a pop

Future growth has to be incisively strategic. This comes with a certain pedigree, which I think is missing with DCB. It may not be able to expand with the same momentum.

However, entry price too is important. Right now I think banking and finance sector is very expensive. And atleast a 30% correction is warranted given the current economic environment.

I understand now. DCB is a turn around story. You can not compare its balance sheet, return ratios with established banks. DCB investors visualize its return ratios after three/ four years. Its granular retail assets/ liabilities are its specialty, NPAs are better than industry. Operational efficiency has started to kick in improving return ratios and hence the valuation. Management pedigree is not questionable, its not easy to turn around businesses especially finance/ bank ones. I think, presently, it is the perfect case of growth + rerating. From 2009 to 2013, it was a perfect case of successful turn around. Now after turn around, profitable business model is in place, it needs to replicate and scale up. I request to study this story.

Happy New Year ValuePickr’s !!

Here is an update on my portfolio as of 10th Jan, 2020 !!

Sitting with 20% cash; suggestions and feedback is appreciated !!

Last 5 Stocks have been added in PF 6 Months Back due to which allocation is negligible; it will go up with time as monthly SIP’s increases the investment amount.

Cheers !

Puneet