Demand growth in global paper industry is highly contributed by developing economies like India compare to western countries. Per capita consumption of paper in India is 13 Kg against global average of 57 Kg and significantly below 200 Kg in North America. Global paper and pulp mills industry has contracted slightly over the past 5 years (Due to shift in digital media and paperless communication across developed economies) but demand in emerging markets has seen increase in demand from packaging material.

Indian Paper Industry:

Paper Industry is highly fragmented segment in India. Indian Paper Industry is made of 750 mills out of which, 60% mills are small units with less than 50 thousand TPA capacity.

This Industry is broadly classified into 4 segments:

• Printing and writing

• Packaging paper and board

• Speciality papers & Others

• Newsprint

Raw material scenario:

• Pulp is primary raw material

Pulp costs over 40% of raw material cost obtained from

wood – 30-35% contribution,

wastepaper=45-50% contribution &

Agri-residues 20-22% contribution.

• India has a total land area of 3.3 million sq km with forests covering only 0.7 million sq km. About 78% of the total land area is non-forest area. That to diminishing. Hence, concept like agro forestry started and this has started yielding results.

Fuel

One of the important fuel for paper industry is coal. In last few quarters, there has been continuously shortage of coal in India. Hence, paper industries in India accesed international market for coal which resulted in to increased cost.

Opportunity

In age of digitization, a growth can be limited in writing and printing paper segment but this is being offset by the increase in demand growth for packaging board segment. Demand for better quality packaging of FMCG products marketed through organized retail, rising healthcare spends, over the counter medicines and increasing preference for ready-to-eat foods are the key demand drivers for paperboard.

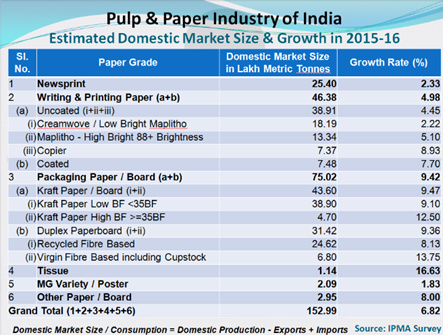

Following is the growth forecast, forecasted by IPMA (Indian Paper Mills Association)

Among this, Bllarpur and JKP are the top two companies in terms of market share. Find the highlights of both the companies below:

Ballarpur Industries Ltd

• Over the last 7/8 years, company has made significant debt-financed investments to modernise and scale up capacities across most of its Indian manufacturing units as well as in Sabah Forest Industries (SFI), the pulp and paper producing facility acquired in Malaysia.

• SFI has not been able to generate sufficient returns, largely on account of an unrealistically strong Malaysian Ringgit.

• Committee of Directors to consider and recommend a financial restructuring plan under the Strategic Debt Restructuring (SDR) scheme of the Reserve Bank of India.

• shares will be allotted to banks and financial institutions according to the proportion of their outstanding loan exposure to BILT. After the allotment, the Joint Lenders Forum will collectively own 51% of the fully paid up equity share capital of your Company.

• This will reduce the promotor stake in the company.

• They produce paper only on demand against advance payment.

JK Paper

• JKP able to maintain a leadership in copier segment with the 24% market share and amongst the top two positions in the coated paper and packaging board segment.

• JKP around 52000 KL per day water requirement .

• Managed to reduce cost well

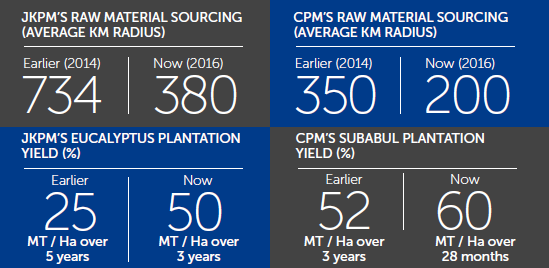

• Landed cost of raw material reduced by 10-11% on account of agro forestry.

• they outsourced the paper and marketed that under the brand name of JK Paper. (Shift from manufacturing to distribution). And they will continue to do so in future (specially coated paper).

o Revenue from outsourced products increased from 3% tro 7% of sales.

o This will increase the ROE but will reduce the margins.

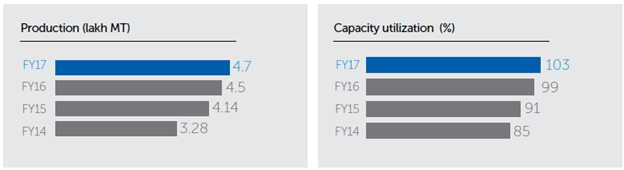

• Already running at more than 100% capacity from last 2 years.

• “We expect to increase the proportion of outsourced products withing our overall revenues, validating our growing brand strength, progressivelt liberating our sales from a complete dependence on captive manufacturing. “ Quotes from Annual report.

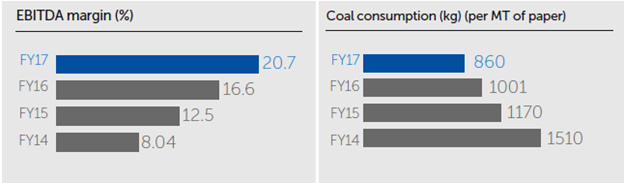

• In 2012-13, 23% of costs were from power and fuel. This declined to 7.68% in FY17.

• Packaging board business to 20% of revenues in FY17. Company emerged among the three largest virgin fibre packaging board players in India.

• Working capital has been reducing as they manage to keep the raw material inventory as low as possible as they source it from nearby area.

• There has been rating upgrade which is being resulted as reduction in interest rate.

• Shifted its focus from furnance oil to lime. Furnance oil is widely used in industry but it is costly.

• Will set up an additional capacity of 2,00,000 tonne in gujarat. It will be brownfield expansion.

o Debt to equity 1000:450 (total Rs. 1450 crore.)

o New plant will run at 80% capacity utilisation in first year.

o It will take 24 months to 30 months to commision after enviormental clearance.

• Sirpur acquisition cost is 150 crore and extra debt will be on the books of sirpur mill only and will be repayed from the EBIDTA of sirpur only.

• JKP already running at 110% capacity utilisation. Growth will come from outsourcing.

• There is scope for margin improvement of half % if they procure 80% wood requirement from 200 KM (Current 60%).

Q4FY18 concall highlights:

• Total Vol: 131000

• Uncoated paper vol: 82000

• Coated paper vol: 23000

• Packaging paper/board vol: 25000.

• NSR 56

• Will set up an additional capacity of 2,00,000 tonne in gujarat. It will be brownfield expansion.

• Debt will increase by 1000 crores. 450 will be funded by internal accruals. Total expenditure is around 1450 crores.

• new plant will commence its production in 24 months to 20 months after the environmental clearance.

• Sirpur acquisition cost is 150 crore and extra debt will be on the books of sirpur mill only and will be repayed from the EBIDTA of sirpur only.

• Packaging industry growing at 12 to 14%. There will be more demand than supply in 2020.

• “I do not think any major announcement from the A grade players barring the Emami packaging board has come in. TNPL setup their packing board machine last year and they are not fully stabilized, so I do not think they may announce any major investment at this stage, may be in the writing and printing paper they can think of in the next two years. Ballarpur I do not think that they can put any major investment at this stage because they are not yet out of the wood and West Coast I do not know whether they will invest. It is very difficult to say, yes all the players may further augment their capacities in times to come when there is a good demand.” -Transcript Q4FY18

• Other markets are more intersting for foreign players. So they are not very much active in India.

• In odisha – Produces 100% in first year only.

• In new plant, it will be 80%+ in first year after commisioning.

• Foreign integrated packaging player has margin ratio of 18% to 20%.

• Expecting 2 to 3% increase in NSR per KG for FY19.

• Sirpur plant was shut for 4 years. It may take more six months to start the mill.

• Sirpur plant has closer proximity to coal and pulp.

• Total vol for an year is at 501000 tonne.

• For acquisition of sirpur plant, they have been rewarded in terms of electricity, GST, wood and coal.

• There can be antidumping duty on Paper.

• JKP already running at 110% capacity utilisation. Growth will come from outsourcing.

Challenges/Threats :

• Access to quality and cost competitive raw material

o India is wood fibre deficient country as government of India doesnot permit industrial plantations in the country

o recovery rate of wastepaper in India is quite low (~30%) due to lack of an effective collection mechanism.

o So the players depend on the imports of pulp, wastepaper and even pulpwood to meet their raw material needs and often have to pay premium for availing them thereby impacting profitability and capacity addition

• Competition from imports

o Imports are 20% of the paper consumtion in India

o No anti-dumping duti on Paper imports in India

o Imports from ASEAN countries surge 67% in FY17, china imports increase by 44%

• Technology

o raw material as well as the power consumption is higher as compared to a modern paper mill in India

• Issue with Industrial plantation policies

• Also, India does not have robust system of waste paper collection, sorting, grading.