Few of my takeaways from Q1 FY25 of Protean eGov Technologies

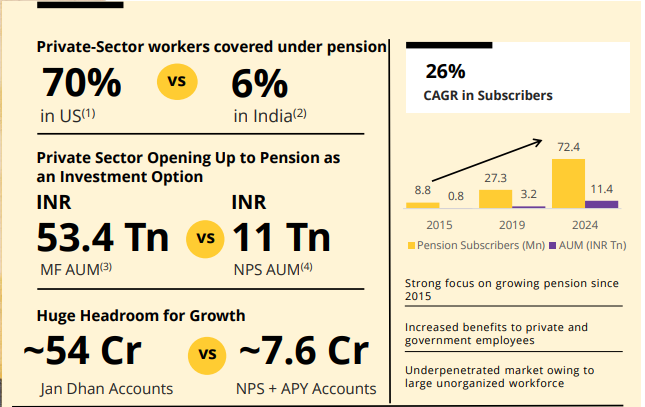

Protean eGov Technologies appears well-positioned to capitalize on India’s ongoing digital transformation. The company’s core businesses in tax services, pension administration, and identity verification continue to show strength, with pension and identity services growing at double-digit rates. While tax services saw a temporary slowdown due to election activities, management expects this segment to rebound. The company is also making inroads into new high-potential areas like digital commerce (ONDC), agriculture, education/skilling, and healthcare through its involvement in building digital public infrastructure.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

Protean is strategically expanding beyond its traditional government services into more innovative areas. Key initiatives include developing the Agristack for agriculture data exchange, launching ProteanX for blockchain-based verifiable credentials, and introducing eSignPro for end-to-end digital document signing. The company is also pursuing international opportunities, with active engagements in 12 countries and 18 potential deals in the pipeline.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

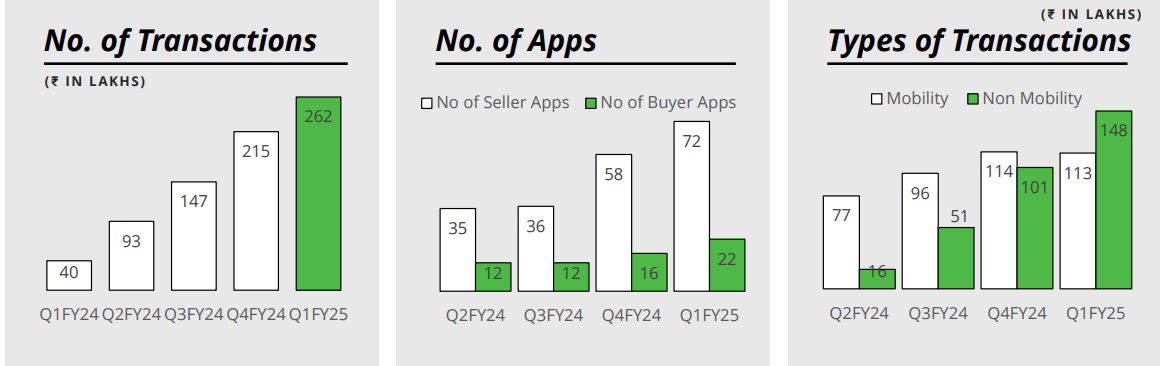

The overarching theme is India’s push towards digitalization across sectors. This is evident in the growth of digital identity services, increasing pension penetration, and the development of open digital ecosystems like ONDC for e-commerce. The trend towards paperless, digital processes is driving demand for Protean’s newer offerings like eSignPro.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

Strong government support for digital initiatives provides significant tailwinds. The recent budget emphasized development of digital public infrastructure across sectors like agriculture, education, and healthcare - all areas where Protean is building capabilities. Increasing internet and smartphone penetration in India also bodes well for adoption of digital services.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

The main headwind appears to be the cyclical nature of some government-related business, as seen in the temporary slowdown in PAN card issuances due to elections. Dependency on government contracts and policy decisions could lead to occasional volatility in revenues.

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

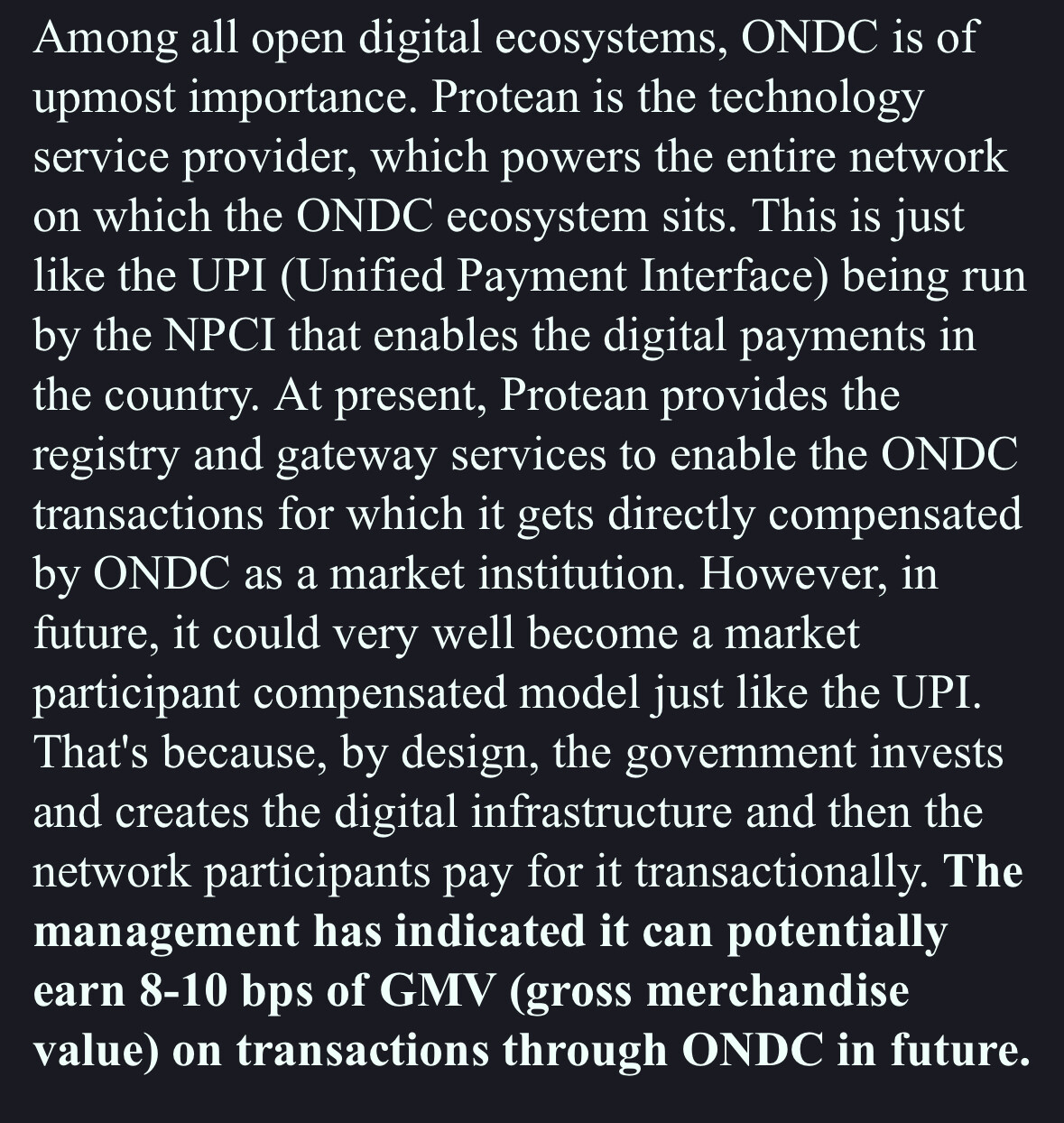

A key concern is the timeline for monetization of new initiatives like ONDC. Management indicated that while they are currently reimbursed for infrastructure costs, a transaction-based revenue model is expected in the future once the ecosystem reaches critical mass. For international expansion, management acknowledged the long sales cycles but expressed optimism about near-term breakthroughs.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

In core areas like PAN card issuance and pension administration, Protean enjoys dominant market positions. For newer digital offerings, the competitive landscape is still evolving. The company’s long-standing relationships with government entities and experience in building large-scale digital infrastructure could provide an edge.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

Management refrained from providing specific numerical guidance but expressed confidence in growth prospects across both traditional and new business lines. They expect the online channel for PAN issuance to continue growing, which should benefit margins.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

With a strong cash position of over 700 crore rupees and zero debt, Protean is well-positioned for inorganic growth. Management indicated they are actively seeking acquisition opportunities that could provide faster go-to-market capabilities or access to cutting-edge technologies.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Key opportunities lie in the massive untapped potential for digital services in India, particularly in sectors like agriculture and education. The main risks include execution challenges in scaling up new initiatives and potential shifts in government policies or priorities.

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐥𝐢𝐦𝐚𝐭𝐞:

The regulatory environment appears largely supportive, with government initiatives aligning closely with Protean’s focus areas. However, the company’s heavy reliance on government-related business means it remains vulnerable to any adverse policy changes.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

The growth in areas like digital identity services and pension subscriptions suggests positive customer adoption. For B2B offerings like eSignPro, management indicated early traction with corporate customers, particularly in the financial services sector.

Disclaimer: This is a general analysis and does not constitute financial advice.