Most of you have already read the article & aware of the same. Incase not then pls find the link.

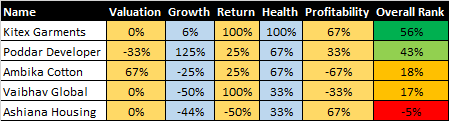

I have put these stocks in my fundamental analysis framework and arrived at below ranks.

Clearly few of them looks like attractive value bets, however as with many stocks - lack of integrity of management is a perennial problem. Its actually the real hidden gem/stone as the case may be. One may add Kaveri Seeds, Eros Int and a few more as well.However, overall global slowdown, market correction etc have kind of created lollapalooza effect- downwards !

This is a complex puzzle, many times best analysed-good quality multibaggers have thrown it away !

From framework, Ambika cotton growth and profitability are poor, while valuation, financial health and returns are good. In my opinion either growth & margins has to improve or valuation has to become super attractive. With 18% overall score its worth in watchlist, not in portfolio.

Jokes apart. Disc : I am not invested in any of these. Also this framework does not capture accounting and management goof up, fraud, corp gov etc…3 months into equities - I am not as worried about recession, macro slowdown as much as I am worried about ethics & crop gov of individual scrips.

A debt free co. giving 18-20% stable and predictable RoE should atleast trade at 2 times book value since an FD’s interest rate is 7-8%. Ambika cotton (with spindle addition also on the anvil) is a good investment option at CMP IMO.

To emphasize slightly more : even if the co. Offers zero growth, the stock is below fair value IMO. Like I mentioned, in an FD, your RoE is say 7.5%. In an FD, price to book value of ur investment is 1 (since the ‘market price’ and the ‘book value’ r the same) . so if an investment yields 7.5*2=15% predictable RoE, it should quote at 2 times book value. (And if the investment is in form of a share, add 2-3% to the 15%, since Owning stocks is riskier than owning an FD)

Ambika’s RoE is arnd 18% and book value is arnd 550/- and CMP is 800/-.

Please go through the ambika cotton thread. IIRC, they are doing 30% capacity expansion (?).

I personally like Ashiana Housing the most even though it ranks the lowest. The reason for its dismal performance lately has been due to downturn in the realty sector. Also one must remember that it changed its accounting policy in the past two years which is a lot more conservative in nature. Right now no one wants to own this stock or any other stock in this sector which makes it even more attractive to me.

I like the management and have full faith in them. I am looking at this company from a 8-10 year perspective. I like companies who change the value proposition(affordable and senior housing) and the value chain( asset light model) with focus on the right metrics like ROIC and FCF.

Real estate cycles have longer runs. A stock bull run is of 3 years avg and bear run of 1.5 year. RE cycles for the same is 12 years and 6 years…all approx. now betting on RE recovery and hoping ashiana will emerge will requires patience.

In FA framework above ashiana scored poorly on returns, efficiency and growth. Scores good in valuation, health and margins

Jokes apart. Disc : I am not invested in any of these. Also this framework does not capture accounting and management goof up, fraud, corp gov etc…3 months into equities - I am not as worried about recession, macro slowdown as much as I am worried about ethics & crop gov of individual scrips.

Jokes apart. Disc : I am not invested in any of these. Also this framework does not capture accounting and management goof up, fraud, corp gov etc…3 months into equities - I am not as worried about recession, macro slowdown as much as I am worried about ethics & crop gov of individual scrips.