ABOUT

Priti International Ltd is an Indian furniture & lifestyle brand that offers interior collections for homes.

Priti International Ltd (PIL) was established in 2005. It’s a family owned and operated business with a handful of employees and 3 factories in Jodhpur. Company has grown to an employee base of 80+ employees & 250+ skilled Artisans.

Products

The company manufactures 750+ products including

1 Living Room Furniture: Sofas, coffee tables, Side Boards, etc.

2 Bedroom Furniture: Beds, Cabinets, etc.

3 Dining Room Furniture: Dining tables, chairs, sideboards, etc.

4 Office Furniture: Desks, chairs, filing cabinets, etc.

5 Custom Furniture:

FY21 Revenue Breakup Company generated ~99% revenue from Wooden and Iron Handicrafts, with the remainder coming from textile handicrafts.

FY21 Geographical breakup

Exports ~ 84% (vs 97.6% in FY20)

Domestic: 16% (vs 2.4% in FY20)

At present, PIL products are exported to 22+ countries including USA, Spain, Holland, Turkey, China, and many other destinations.

Ecommerce Presence Company has a significant presence across Ecommerce platforms such as Amazon, Flipkart, etc.

Manufacturing

As of FY23, the company has 3 manufacturing facilities in Jodhpur.

PriAuction.com

In Nov,23, company launched it’s new auction website “PriAuction.com. The website is auction experience for collectors of premium furniture and antique pieces.

Offline store in Jodhpur

In Nov,23, company opened its new B2B furniture store, PRITI HOME at Boranada, in Jodhpur, Rajasthan.

Order from AAI, Hyderabad

In July,23, company got its order for Airport Furniture Segment from Airport Authority of India, Begumpet Airport, Hyderabad. The order consists of furniture solutions, including seating arrangements, waiting lounges, information kiosks etc.

Subsidiary

The Company had incorporated a new Subsidiary company viz. “Priti Innovations Private Limited” on September 29, 2022.

Strengths:

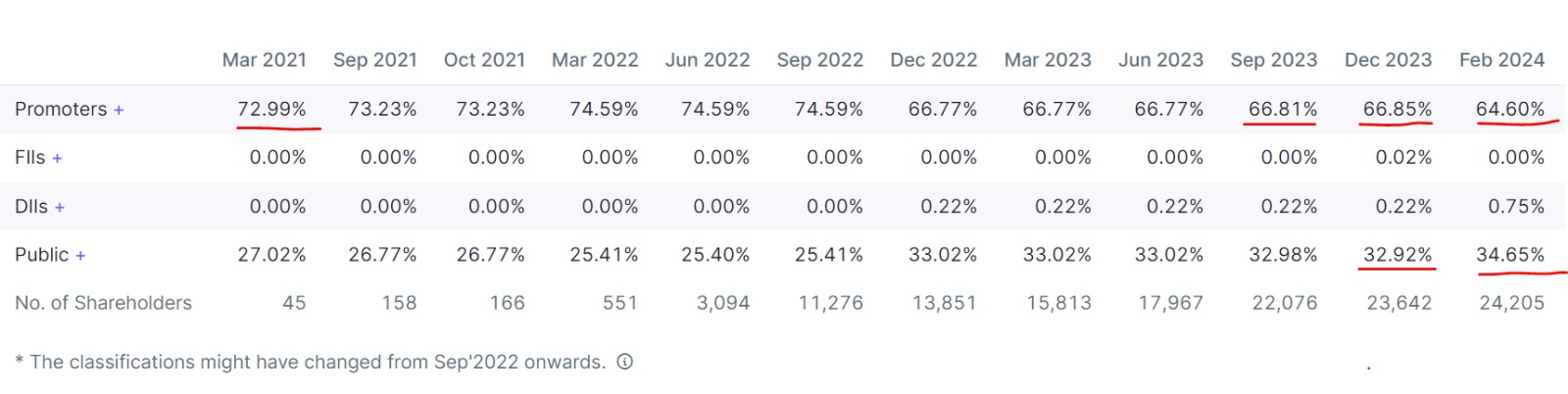

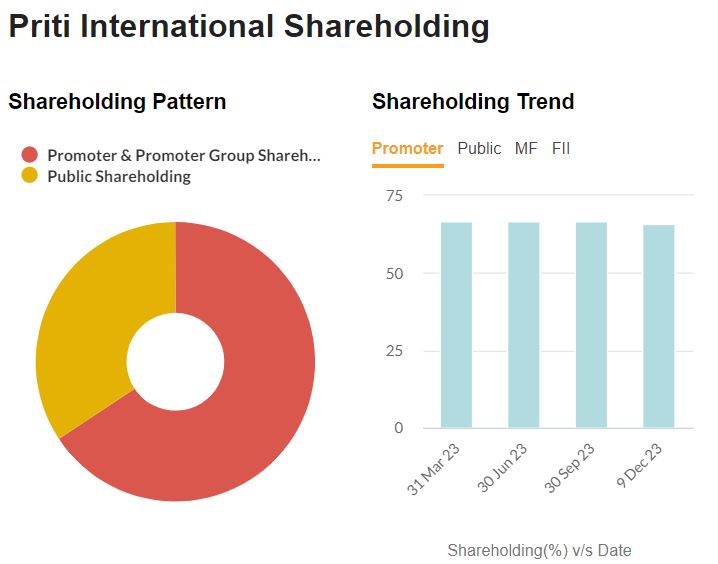

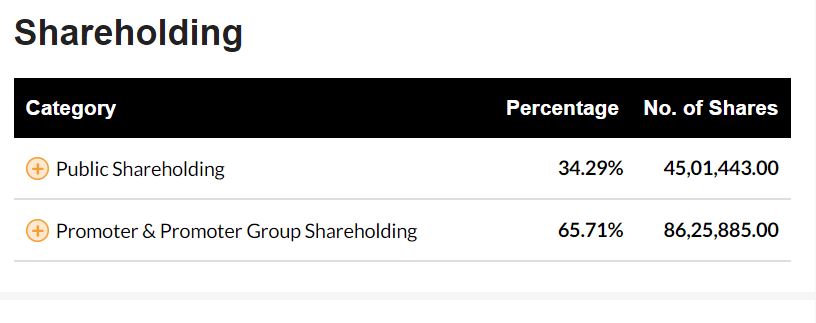

- Strong Promotors & promotor Holding 65%

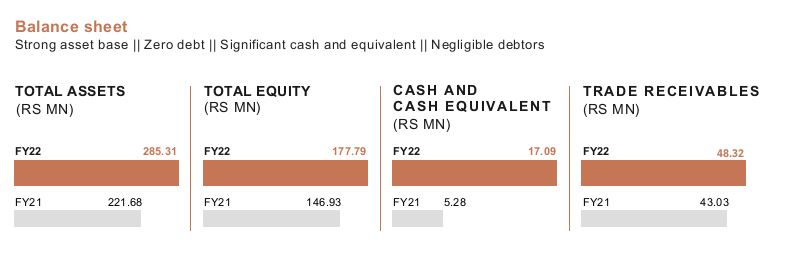

- Company with No Debt

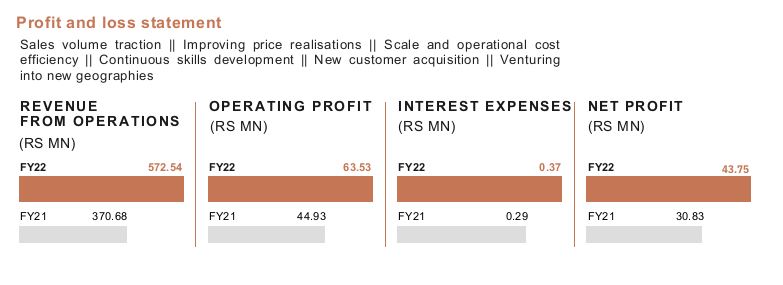

- Company with high TTM EPS Growth

- Growth in Net Profit with increasing Profit Margin (QoQ)

- Growth in Quarterly Net Profit with increasing Profit Margin (YoY)

- Annual Net Profits improving for last 2 years

- Company with Zero Promoter Pledge

- Growth in Operating Profit with increase in operating margins (YoY)

Weakness:

- Low OPM

- Depends on Trees & Woods high raw materials prices.

- Stock is categorized as micro-cap less than 300 Cr M.Cap.

Opportunities:

-

Global Expansion: The mention of the distribution of products in the United States, Europe, Australia, and Asia, especially the Middle East and India, suggests an opportunity for further global expansion. The emphasis on being amongst the highest furniture sellers on platforms like Amazon indicates success in international markets.

-

Changing Furniture Purchase Habits in India: The growing middle-class population, rising disposable income, and increasing urbanization in India present an opportunity for the expansion of the domestic furniture market. The focus on modular, particle board, and state-of-the-art furniture aligns with changing consumer preferences.

-

WFH (Work From Home) Furniture: The emergence of a new category in the form of WFH furniture due to the COVID-19 pandemic opens up new opportunities. The company’s launch of an e-commerce site and presence on other large aggregator e-commerce sites positions it well to cater to the increased demand for online furniture.

-

Government Policies: The increase in customs duty on imported furniture into India to promote localized occupation in the employment-intensive sector and support the “Make in India” initiative presents an advantage for the company, which focuses on the Indian market.

-

Domestic Business Growth: The positive performance of the domestic business amid the COVID-19 pandemic and the anticipation of strong momentum and growth within the next 2-3 years indicate an opportunity for further expansion in the Indian market.

-

Brand Building: The focus on building brand Priti in the domestic market indicates a strategic move to establish a strong presence and recognition within India.

-

E-Auction Site for Vintage Furniture: The development of India’s first-ever vintage furniture e-auction site presents an innovative approach to selling period pieces, original antiques, and collector’s items, creating a new revenue stream and an inclusive ecosystem.

-

Process and System Strengthening: The commitment to developing stronger processes and systems reflects a focus on operational efficiency and scalability, laying the groundwork for future growth.

-

Diversification from China: The diversion of orders away from China due to COVID-19-related challenges, regulatory uncertainty, and global buyers looking to de-risk their business provides an opportunity for the company to capture a larger share of the international market.

-

Omni-Channel Strategy: The aspiration to become India’s number one furniture and home décor brand through an omni-channel strategy, including e-commerce, offline stores, and B2B sales, aligns with the trend of consumers shifting from the unorganized to the organized sector.

Threats:

-

It’s a Microcap stock with low domestic market exposure.

-

Valuations are turning to Expensive.

-

Supply Chain Disruptions: The reliance on skilled artisans and the production of handmade wooden and iron handicrafts may expose the company to supply chain disruptions due to factors like labor shortages, raw material availability, or transportation issues.

-

Global Economic Downturn: A global economic downturn could impact consumer spending on non-essential items such as furniture, affecting the company’s revenue, especially in export markets.

-

Competition: Intense competition from unorganized players in the furniture and lifestyle industry could pose a threat, with other players offering similar products and services, potentially affecting market share and pricing.

-

Regulatory Changes: Changes in trade policies, tariffs, or regulations in the export destinations could affect the company’s ability to operate smoothly in international markets.

-

Pandemic Impact: Ongoing or future pandemics may disrupt manufacturing operations, supply chains, and consumer behavior, impacting the company’s overall business operations.

-

Dependency on Handicrafts: The company’s heavy reliance on wooden and iron handicrafts exposes it to changing consumer preferences or shifts in demand for these specific products.

-

Environmental Concerns: Increasing environmental awareness and regulations may impact the sourcing of materials or production processes, potentially affecting costs and operations.

-

Economic Challenges in Domestic Market: Despite growth in the domestic market, economic challenges, such as inflation or reduced consumer spending, could impact the company’s revenue from domestic sales.

Disclosure : Invested