If we talk specifically about price so according to management commentary they said that they are participating in Jal Jeevan Mission. In PVC they have participated in SWP not that keen but yes they participated, reason for not actively participating is extremally difficult margins and also demand is not consistent. so accordingly, it is one of the growth driver for industry but not the primary driver for growth of industry.

1 Like

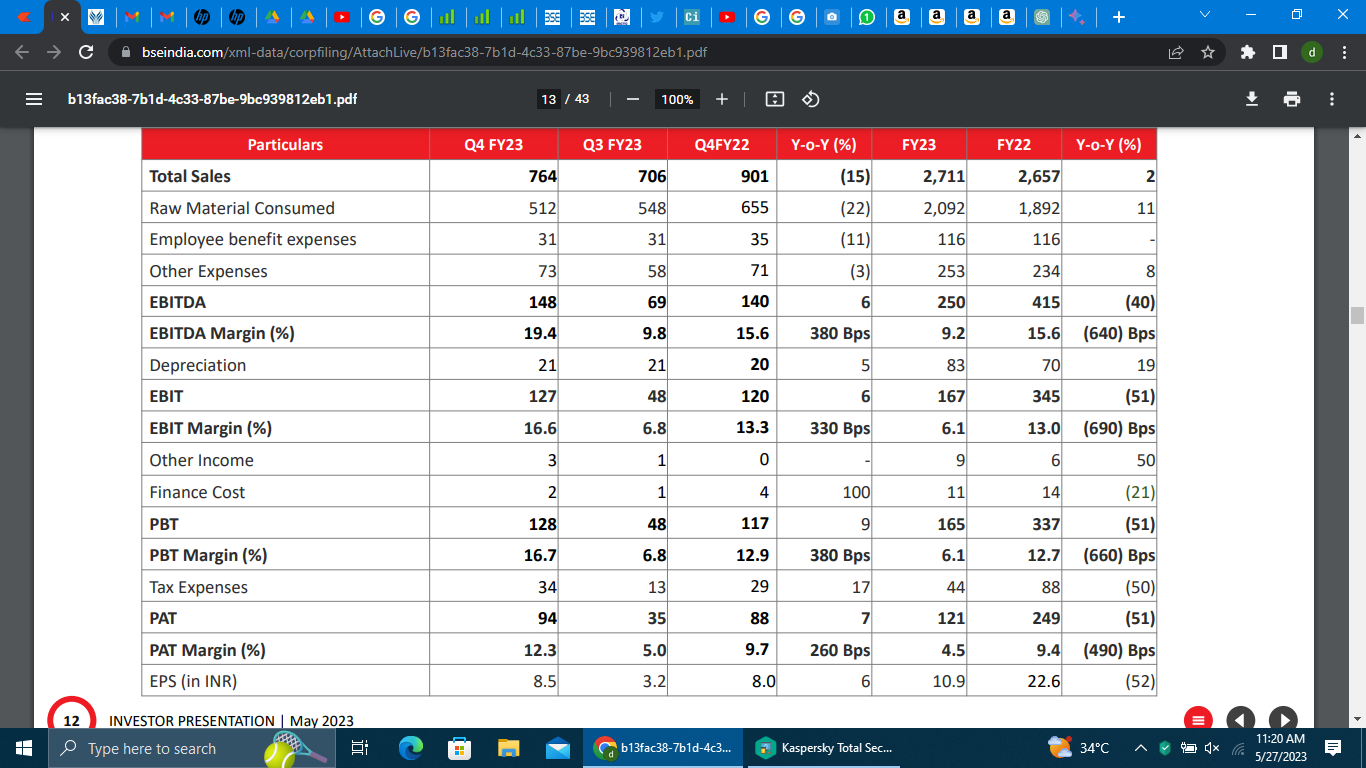

Prince Pipe update Q4 FY 23

Q4 FY23 revenues at ₹ 764 crore as compared to ₹ 901 crore in Q4 FY22

o Volumes in Q4 FY23 at 44,317MT as compared to 45,287 MT in Q4 FY22

o EBITDA for Q4 FY23 improved by 6% YoY at ₹ 148 crore versus ₹ 140 crore in Q4 FY22

➢ Margins enhanced significantly by 380 bps YoY to 19.4% in Q4 FY23

o PAT improved by 7% YoY for the quarter at ₹ 94 crore as compared to ₹ 88 crore in Q4 FY22

o Company continues to remain long term debt free during the quarter

Revenues in FY23 grew by 2% YoY to ₹ 2,711 crore from ₹ 2,657 crore in FY22

o Volumes improved by 13% YoY in FY23 to 157,717 MT compared to 139,034 MT in FY22

o EBITDA at ₹ 250 crore in FY23 vs. ₹ 415 crore in FY22

o PAT in FY23 at ₹ 121 crore as compared to ₹ 249 crore in FY22

o Short term debt reduced from ₹ 150 crore in March 2022 to ₹ 58 crore in March 2023

o Working capital days – 57 days as on March 2023, (68 days as on March 2022)

➢ Inventory days ‐ 57 days vs. 85 days as on March 2022

➢ Debtor days ‐ 56 days vs. 60 days as on March 2022

➢ Creditor days ‐ 56 days vs. 77 days as on March 2022

Looks like the Inventory loss cycle is finally over. The same has been bought out by the management. There has been decent growth in volumes for the year even though it has not been that profitable.

Performance for FY23 was adversely impacted by sharp decline in PVC prices leading to destocking

and inventory losses severely impacting performance in H1 FY23.

➢ After a steep correction of ~ Rs. 66 per kg from April till November 2022, PVC prices recovered by ~ Rs. 11 per kg till March 2023.

➢ Capex of 150 cr for eastern region

➢ Implementation of ERP

➢ launched wirefit and one fit for industrial use

➢

➢Ebitda Margin is back to high doiuble digit.

➢company has gained market share in this downturn.

➢Operating leverage will kick in with growth in revenue and fresh inventory being at low price.

➢ Management talks of benefit from industry consolidation and balance sheet constraints in many small unorganized players.

The same should be visible in piping players as a group.

waiting for their concall for better understanding, though this business doesn’t have lot of moving parts.

best

Divyansh

6 Likes

Q4FY23 Con-call Updates

-

Continue product expansion with launch of state of art products in piping division which brings innovation & global products in Indian market.

-

planned greenfield expansion in state of Bihar. The expected capacity of piping plant would be around 35000 MT initially which is investment of Rs. 150Cr. which includes land and adequate infrastructure plan to commence production by Q4FY25.

-

Bathroom Segment: Vendors and designed have been finalized & core team building including 3 state heads & services engineers have already been appointed.

-

Set to launch entire bathware range in end of Q1FY24.

-

Debtor days decreases from 60 in 2020 to 56 days in 2023.

-

Inventory days decreases from 85 days in 2020 to 57 days in 2023.

-

Overall working capital days was 68 in march 2022 to 57 days in march 2023.

-

Transferring from traditional legacy system to Global ERP system this implementation face certain challenges & thus affect Q1FY24 result.

-

They have done 30Cr. of net sales in FY23 and for FY24 they are planning to double there sales of water tank.

-

Margin in storage tank is same as pipes & fittings which is 12 to 14%.

-

FY24 capex 80-84Cr. for land & building in Bihar and 80-85Cr. maintenances capex.

-

Total Advertising expenses in Q4Fy23 is Rs. 12 Cr. and for whole year is 125Cr.

-

Company source 45% of Raw material (PVC resin) locally from reliance and chemplast and remaining import.

-

Company has 10% market share in CPVC and 7% market share as whole.

6 Likes

Prince pipes Q4 concall -

Q4 outcomes -

Revenues at 764 vs 901 cr YoY

Volumes at 44.3k MT vs 45.3k MT

EBITDA at 148 vs 140 cr, Margins at 19.4 pc vs 15.6 pc (significant improvement)

PAT at 94 vs 88 cr

FY 23 outcomes -

Revenues at 2711 vs 2657 cr

Volumes at 157k MT vs 139k MT (up 13 pc)

EBITDA at 250 vs 415 cr

PAT at 121 vs 250 cr

Short term debt reduced from 150 to 58 cr

Inventory days at 58 vs 85 days

Working capital days at 57 vs 68 days

FY 23 performance adversely affected by steep fall in RM prices in H1 causing inventory losses

To launch One Fit and Wire Fit products in piping division to bring global technology to India

Aiming to add 35k MT capacity in Bihar(Greenfield)

Bathware launch planned in End of Q1

Company migrating to ERP from legacy systems. May have some adverse impact in Q1

Current number of production facilities - 07, Warehouses - 09, SKUs - 7200

Capex towards Bihar expansion to be around 80 cr. To commence production by Q4 of FY 25. Plus around 70 cr of maint capex

Uptick in RE industry is strong

Q1-Q3 saw significant sale losses due inventory de-stocking due RM price cuts

Q4 saw an inventory gain of apron 25 cr

Demand continues to be extremely strong in Q1 across Agri and RE sector

Channel inventory is low due strong end demand

Previously commissioned plant at Telangana operating at 40 pc

Storage water tanks sales in FY 23 @ 30 cr. Intend to double it in FY 24

CPVC is a key focus area for the company specially after the flow guard ( Lubrizol ) tie-up

Jal Se Nal is a decent revenue contributor

Company doesn’t sell directly to the Govt. Sells it through local distributors to avoid credit risk

Jal Se Nal scheme is likely to continue for foreseeable future

Ex of Q1, expect 10-12 pc volume growth in FY 24

RE (building materials) is the main focus area for the company

Agri segment helps absorb fixed costs

Advertisement expenses for FY 23 @ 42 cr

90 pc of cost for changing over to ERP system already baked in FY 23 numbers

Company procures CPVC from Lubrizol and PVC from RIL and Chemplast Sunmar in addition to imports ( in case of PVC )

Expect 14-15 pc EBITDA margins over long term

Most inventory gains/losses should even out over 4 Qtrs barring wild fluctuations in RM prices that company saw in FY 22, 23

Inventory loss in FY 23 was 125 cr

CPVC prices have also cooled off

Local players and Lubrizol increasing CPVC capacities in India - long term positive

This will make CPVC more affordable and help the top 4 players

Infra demand comprises aprox 10-12 pc of Industry today

Expecting 15-20 pc 2-3 yr CAGR volume growth going fwd

Company has early mover advantage in East India

Company’s CPVC mkt share is around 10 pc which contributes 25 pc of company’s revenues. Overall Mkt share is around 7 pc

Disc: holding

5 Likes

The company has moved into sanitary ware and had a launch meeting in Goa today.

It’s a natural horizontal expansion for the company becuae the same customers use the pipes who use new sanitry ware like sinks bathroom fittings and commodes etc.

If quality of products is decent then it will be a great fit for the company.

It’s slightly less cluttered than pipes segment. In pipes duplicate products is rampant. So i think better margins shoild come in this segment if played correctly by the company.

The project in Bihar’s begusarai is going to give a huge edge because transportation is the biggest overhead in terms of charges. Almost all big pipe companies operate from the west India only

4 Likes

My notes of Q1FY24 concall

- Q1FY24 faced operational challenges due to an ERP upgrade.

- Disruptions impacted volumes and product mix, particularly in pipe fittings.

- Unfavorable product mix and pipe fitting ratios led to significantly lower margins.

- Expectations of normalization in pipe fitting ratios in the upcoming quarter.

- Positive outlook due to affordable polymer prices and healthy economic activity in India.

- Focus on branded products, particularly in the Bathware segment.

- Expansion of in-house manufacturing for water tanks.

- Acquisition of land for the eighth manufacturing facility in Bihar to cater to the Eastern market.

Revenue:

- Q1FY24 revenue: Rs. 554 crores.

- Sales volume increased by 19% YoY to 37,155 metric tonnes.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization):

- Q1FY24 EBITDA: Rs. 45 crores, compared to Rs. 44 crores in Q1FY23.

- EBITDA margin for Q1FY24: 8.1%.

Profit After Tax (PAT):

- PAT for Q1FY24: Rs. 20 crores, a 25% YoY improvement compared to Rs. 16 crores in Q1FY23.

Working Capital:

- Net working capital days as of June '23: 59 days, compared to 57 days in March '23.

- Debtor days increased to 64 days in June '23 from 56 days in March '23, acknowledging the need for better control.

Inventory:

- Inventory days as of June '23: 73 days, up from 57 days in March '23 and 78 days in June '22.

- Company maintains optimal finished goods inventory to meet demand.

Polymer Price Stability:

- Expectations of stable polymer prices for the next few months.

Channel Finance Program:

- Steady progress in the channel finance program.

- Increased credit limits of channel partners from Rs. 70 crores to Rs. 105 crores.

- Number of channel partners engaged in the program increased from 76 to 132.

Net Cash Position:

- Maintained a net cash position of Rs. 164 crores as of June '23.

Volume Outlook and Growth Guidance:

- July volumes have been encouraging.

- Optimism about sustained demand, with real estate performing well and affordable polymer prices.

- Expectation of high double-digit growth over a 3- to 5-year period.

- Confidence in the pipe segment’s growth despite entry into water tanks and Bathware.

Competitive Intensity and Pricing:

- Increased capacity additions in the industry, but supply is not expected to outpace demand.

- No need for predatory pricing, and growth is expected to be sustainable and profitable.

CPVC Segment:

- Correction in CPVC prices across the industry, with room for further correction.

- Local capacities in India expected to make CPVC more affordable, promoting long-term growth.

Plumbing Business:

- Plumbing growth has been double-digit for Prince Pipes in recent years, largely driven by building material.

- Focus on building material and setting up capacities for plumbing and SWR segments.

Capex Plans and Capacity Expansion Overview:

- FY '24 Capex allocated primarily for debottlenecking.

- Capex estimate for FY '24: Rs. 90-100 crores focused on existing plants.

- Excludes Bihar project land acquisition and East expansion.

- Covers debottlenecking, maintenance, and potential capacity additions (e.g., water tanks or HDPE) in some facilities.

- Current capacity: 323,000 MT.

- De-bottlenecking of existing plants to contribute 20-30,000 MT by FY '24.

- Bihar plant set to begin commercial production in March '25, adding around 40,000 MT in Phase 1.

- Phase 1 expansion target: 35,000 to 40,000 MT, commencing in March '25.

- Phase 2 expansion details to be determined later.

- Potential for further capacity expansions due to new piping applications, but specifics for FY '25 are uncertain.

Brownfield Capacity Addition:

- Consideration of debottlenecking for capacity enhancement.

- Feasibility identified at several plants.

- Feasible plants: Jaipur, Telangana, Haridwar, and Agra.

- Some plants (Athal, Kolhapur, Chennai) have limited expansion potential.

- Estimated lead time for brownfield capacity: 3 to 4 months.

Capacity Utilization:

- Company-level utilization has been steady at around 50% to 55% of installed capacity.

- In Q1, utilization was slightly lower due to disruptions.

- Telangana plant has seen good utilization since its setup in late '21, estimated at around 35% to 40%.

Realization:

- Realization per ton in the quarter decreased sharply due to unfavorable pipe fitting ratios and product mix.

- Expectations of improvement in realization from the current levels.

- Pricing power has improved over the years due to branding efforts, and product mix has also improved.

Sourcing Mix for PVC:

- Sourcing mix for PVC is currently 60% import and 40% domestic.

Bathware Strategy:

- Bathware is seen as a front-of-the-wall product where brand equity is crucial.

- Investment focus on digital, visual merchandising, brand visibility, and technology.

- Investment in the right people and branding.

- Focus on building a strong distribution network across urban, semi-urban, and rural areas.

- Initially, a combination of retail and project sales with a long-term focus on retail and distribution.

- Leveraging existing relationships with real estate developers for Bathware sales.

- Initial investment in 1Q for the launch event: Approximately Rs.2 crores (one-time).

- Annual investment: Rs.5 crores to Rs.6 crores in manpower and Rs.10 crores to Rs.12 crores in brand building for the Bathware vertical.

- Expansion into faucets manufacturing within 18 months.

- Prepared for initial Bathware investment, with an expectation of it becoming non-dilutive to core profitability after 6 to 8 quarters.

- Long-term vision for Bathware is to achieve better operating margins compared to the short-term investment.

- Targeting the mass premium segment in the Bathware market.

- Aims to address the largest chunk of the market, which is just below Jaguar in terms of premium positioning.

- Will have collections across different price points (premium, mid, economical) but with a primary focus on the mass premium segment.

Participation in Infrastructure Segment:

- Participating in the infrastructure sector, but not aggressively.

- Focusing on improving debtor days to manage receivables.

- Steady growth in DWC and HDPE segments.

- HDPE capacity expansion is planned at the Jaipur facility.

- Bihar will start manufacturing HDPE from the first day of commercial production.

- DWC (Double Wall Corrugated) pipes have seen strong volume growth in the infrastructure segment.

- Infrastructure currently contributes approximately 3% to 5% of total revenue.

Margins Expectations:

- Medium-term margin estimate: 13% to 14%.

- Aspirational for better margins.

- Factors for improvement: product mix, CPVC contribution, operating leverage, and volume growth.

East and North East Expansion:

- Long-term vision for an integrated complex.

- Planned products include PVC, CPVC, DWC, HDPE, water tanks, and fittings.

- Potential for becoming one of the largest facilities within 3 years.

- Current sales in the East region approximately 15% to 20%.

- Expected freight savings and improved quality with local production.

Value-Added Products:

- Value-added products currently include CPVC, PPR systems, and PVC fittings.

- Historical contribution percentages:

- Pipe fittings: 30% to 35% of revenue.

- CPVC: 20% to 25% of revenue.

- PPR: Approximately 4% to 5% of revenue.

One-Off Expenses:

- ERP-related expenses are considered intangible and have been absorbed into the gross block.

- Operating expenses related to ERP implementation are not significant.

- The only one-off expense in the quarter is related to Bathware launches, amounting to approximately Rs.2 crores.

Inventory Loss:

- There was an inventory loss of approximately Rs.10 crores in Q1.

- The impact of PVC price movements on inventory gains in the second quarter is uncertain.

Fittings Segment Margins:

- Fittings segment margins are expected to normalize from the next quarter.

- The guidance of 13% to 14% margin range is inclusive of all expenses, including those related to Bathware.

- In Q1, the company’s margin was affected because of an unfavorable product mix.

- The margin of fittings, an essential product, is significantly higher (1.5x to 2x) than that of pipes.

- Margin should be evaluated on a blended basis for pipe fittings, considering its contribution to revenue.

- In Q1, the contribution of fittings to revenue was lower (around 25%) compared to the usual (32% to 33%).

- Operating margin is expected to return to 12% to 14% over the next 9 months.

Participation in Jal Jeevan Projects:

- The company actively participates in Jal Jeevan Mission projects through contractors.

- Participation will continue as long as the receivable cycle remains disciplined.

- Over the next 2 to 3 years, the demand from Jal Jeevan Mission projects is expected to support industry growth.

Advertising Spend Breakdown:

-

Piping Vertical:

- Ad spend during the quarter: Rs. 12 crores.

- Typically invest 2% of revenue into branding.

-

Bathware Business:

- Estimated ad spend for Bathware: Rs. 10 crores to Rs. 12 crores.

- Percentage of revenue not specified due to the establishment phase.

Chief Technical Officer (CTO) or Technical Head Absent

- The company does not have a Chief Technical Officer (CTO) position.

- Similarly, there is no designated technical head within the organization.

7 Likes

Does anyone have any explanation for the lack of a technical head/ CTO?

1 Like

Pipes and related products are fairly simple and don’t evolve on short time frames. I could not think why would a CTO be required if at all. What changes can prince do by getting a CTO. Also how many times in the past has technology disrupted this sector and how. I could only think of astral doing a tie up with lubriziol. And that also did not change the purpose of the products but did change the quality and usage. As such western world will be way ahead in construction related changes and Indian companies would be keeping a eye on the same. To me prince is more of a play on ancillary to real estate industry in India.

Best

Divyansh

Disc : invested from lower levels

2 Likes

Anyone tracking recent events of Prince Pipes?

Couple of resignations from KMP has happened which can be noticed as hit in stock price also…

Prince Pipes Q2 highlights -

Revenues up 3 pc to 656 vs 636 cr ( despite drop in RM prices )

Sales volumes up 8 pc @ 41.5k MT vs 38.5k M, YoY

EBITDA at 94 vs (-) 11 cr ( margins @ 14.3 pc )

PAT at 71 vs (-) 24 cr ( includes an exceptional gain of Rs 17 cr )

A&P spends for Q2 @ 15 cr

H1 volume growth at 13 pc

H1 EBITDA at 139 vs 33 cr

Prince Bathware receiving good response from channel partners and customers ( launched in Jun 23 - in North, West )

Current facilities -

Athal - 9.3 k MT

Dadra - 65.6 k MT

Haridwar - 98.9 k MT

Chennai - 43.3 k MT

Kolhapur - 16.1 k MT

Jaipur - 38.9 k MT

Telangana - 56.9 k MT

New Capex in Bihar to come online by end of FY 25

Company maintaining long term Debt free status

Fall in RM prices in Sep-Oct led to some de-stocking in Q2. Prices have improved and is causing re-stocking in Q3

Plan to launch bathware in Eastern India by Q4

RE sector sales remain buoyant - specially in Mid and Premium categories. Unsold inventory @ decadal low. Augurs really well for building materials companies !!!

Company’s volume growth for last 2-3 Qtrs has been lagging wrt peers. Company aims to reverse this trend in next 2-3 Qtrs through a mix of pricing actions and HDPE capacity expansion. HDPE is one segment where company has been a laggard

Q2 did bear branding and employee cost. Revenues from this segment will get reflected from Q3 onwards. Aim to hit Qtly sales of 8cr to begin with

PPR pipes are slowly gaining momentum ( an advanced material even vs CPVC ). Prince is a mkt leader here. PPR manufacturing requires completely separate infra vs CPVC manufacturing

Currently CPVC pipes and fittings for 20-25 pc of company’s revenues

Currently there is an anti-dumping duty on CPVC polymer. Its extension or otherwise is a key monitorable

Piping Industry is growing volumes at around 14-15 pc YoY. Company aims to be at that level of volume growth as soon as possible

HDPE pipes contribute to aprox 3 pc of company’s sales volumes. These are mostly used in Infra projects. This segment has lower margins and higher working capital cycle. HDPE business to pick up Mar 24 onwards

CPVC costs have come down because of fall in PVC prices - also led to some de-stocking in Q2

Company’s overall capacity utilisation currently at about 50 pc. Telangana facility operating @ 50 pc - Gives the company a huge Operating leverage possibility in future !!!

Capex guidance for this FY @ 150-160 cr. Out of this, 70 odd cr has been earmarked for Bihar facility

Lubrizol’s new CPVC plant coming up in FY 25 in India. Prince and Aashirvad likely to remain only 2 licences for Lubrizol in India. Local facility will make CPVC far more affordable and should be a great news for the Industry

Disc: holding, biased, not SEBI registered

2 Likes

Regarding capacity utilisation, piping industry doesn’t go as high as 85-90% like in pharma or elsewhere. It is likely to stay around 60-65% at max utilisation. This was clarified in one of the concalls a couple of years ago.

So my understanding is that 50% is as good as around 80-85% for Prince. Not much room unless further capex is done.

5 Likes

Promoter holding has decreased by two percent ,any idea what can be the reaon

My Take

Company has been in consolidation for nearly 2 years and Above, But Why?

Company deals into pipe fitting products and Raw material such as PVC price were going through Volatility and Destocking result in Collapse of margin badly At The same time housing crises in China, Europe & us led dumping in India

One thing to Notice company OPM% For last 10Y average remains above 12% and this year reported 9% which is Outlier

Recent Q2FY24 Showed up Good numbers where OPM% Touched 13%

Greenfield Expansion in Bihar of About 35000 MT will be commercialized Q4FY25 with Nearly 150 Cr Capex and Current Capacity is around 328500 MT and De Bottlenecking may increase 20-30K MT So we can expect Touching 385000 MT Q1FY26

Currently Operating at 50-55% Utilization and Now Real-estate Performance, Jal Jeevan Mission will support the Growth Story of This Segment

Telangana Also at 40% Utilization and which likely to Improve based on Demand going Forward

CPVC where Company Accounts 10% Market share and now remains to be more Focused area due to Lubrizol Tie-up

At the Same time Company entered in Bath ware, Sanitary may further strengthen the Margin of the company

Key Trigger: Product Mix, CPVC Contribution, Operating Leverage & Volume Growth would be main Driver for the Company

Dis: No Buy/Sell Pure Learning

3 Likes

Q1 FY25 Concall Summary

Business Updates

- Marketing initiatives are being enhanced aggressively through clear visibility at strategic locations especially at travel locations ensuring visibility at locations of higher footfalls

Participants

Dolat Capital

HDFC Securities

BOB Capital

Axis Capital

Nuvama

PL Capital

Kotak

DAM Capital

QnA

- The growth has been across agriculture, plumbing and infrastructure and it is across the board

- On a long term basis EBITDA margins should range between 12-13% and that is a sustainable level

- The margins in Q1 are lower than the long term range primarily due to higher growth in agri space where margins are lower and also higher A&P spends which is a conscious effort from the management side

- Capacity addition will be an ongoing process as the long term outlook on the sector is positive and with CPVC becoming affordable and local production of CPVC increasing the market size of this product shall increase disproportionately

- The aspirations on volume growth are much higher than what is being delivered currently and thus capacities are being added and from a margin point of view some quarters get affected negatively due to being heavier on the agriculture side and also higher marketing costs being incurred currently

- Since the capacity addition is immediate and sales realisations take some time to reach optimum utilization the asset turn ratios will look lower currently

- The inventory will always range between 60-70 days and the top priority remains to keep good supply and thus management will not shy away from storing higher inventory

- On PVC anti dumping tough to speculate whether anti dumping will come and current PVC prices are lower for most PVC manufacturers who are struggling at current prices

- There was no inventory gains/losses during the current quarter

- Over the next couple of quarters the footprints in South and East India will be expanded on the bath ware side

- The outlook for growth over the next 2-3 years looks very good and on EBITDA margin side it should range between 12-14% with better control on receivables

- From a consumption point of view in terms of PVC India is one of the key market that is doing well and hence all PVC supplies of the world are being directed in India

- The company has seven manufacturing units with the eight one coming up in Bihar which will start in January and add 45000 tons of production capacity

- The overall industry is growing and there is no need to do predatory pricing and selling by undercutting others

- Inventory losses and gains are part of this industry and thus margins should always be analysed ex of inventory adjustements

1 Like

Prince Pipes and Fittings Limited Q1 FY25 Analysis: Key takeaways!!

Prince Pipes delivers strong Q1 performance, driven by growth across key segments. Positive industry outlook fuels optimism for accelerated growth.

Strategic Initiatives:

- Prince Pipes is aggressively enhancing its branding initiatives across various travel hubs and modes to strengthen its top-of-mind recall among customers.

- The company is making steady progress in building its bathware segment, “Aquel by Prince,” with plans to expand its presence across all zones in India over the next 2 quarters.

- The construction of the new manufacturing facility in Begusarai, Bihar is progressing on course, which is expected to cater to the fast-growing demand in the East Indian market.

- The company continues to focus on strengthening its distribution network and expanding its product portfolio to drive volume growth.

Trends and Themes:

- The Union Budget 2024-25 outlined several initiatives that are favorable for the pipes and fittings industry, such as the promotion of natural farming, investment in infrastructure development, and support for MSMEs.

- The company is witnessing a shift in demand patterns, with agriculture being a significant contributor to volume growth in Q1 FY25.

- The industry is experiencing consolidation, with smaller players struggling due to volatility in raw material prices, providing acquisition opportunities for the larger players like Prince Pipes.

Industry Tailwinds:

- Robust demand in real estate, agriculture, and infrastructure sectors.

- Favorable government policies and initiatives, such as the Prime Minister Awas Yojana Urban 2.0 and the development of investment-ready industrial parks.

- Increasing affordability of raw materials, particularly PVC, driving industry-wide volume growth.

Industry Headwinds:

- Volatility in raw material prices, particularly PVC, which may impact profitability in the short term.

- Potential anti-dumping duty on PVC, which could affect pricing dynamics in the industry.

Analyst Concerns and Management Response:

- Analysts questioned the decline in EBITDA margins in Q1 FY25 despite the strong volume growth, to which the management attributed it to a higher contribution from the lower-margin agriculture segment and increased branding expenses.

- Management reiterated its commitment to maintaining EBITDA margins in the 12-13% range on a long-term basis, excluding inventory gains or losses.

- Analysts also raised concerns about the increase in inventory days, to which the management responded that it was a conscious decision to ensure adequate supply to meet the growing demand.

Competitive Landscape:

- Prince Pipes is among the leading players in the industry, competing with other major players like Astral, Supreme, and Finolex.

- The company is focusing on strengthening its brand, expanding its distribution network, and driving volume growth to maintain its competitive position.

Guidance and Outlook:

- The company maintains its guidance of 15% volume growth for FY25, with plans to aggressively add capacity through debottlenecking of existing facilities and the new Begusarai plant.

- Management remains confident about sustaining EBITDA margins in the 12-13% range on a long-term basis, despite the short-term pressures.

Capital Allocation Strategy:

- The company is prioritizing capacity expansion and new product development to drive volume growth and market share gains.

- The management also emphasized the importance of improving working capital management, particularly through tighter control on receivables, to support its growth plans.

Opportunities & Risks:

- Opportunities: Favorable government policies, growing demand in real estate, agriculture, and infrastructure sectors, and industry consolidation.

- Risks: Volatility in raw material prices, potential anti-dumping duties, and competitive pressures.

Regulatory Environment:

- The Union Budget 2024-25 introduced several initiatives that are expected to benefit the pipes and fittings industry, such as the promotion of natural farming and investment in infrastructure development.

Customer Sentiment:

- The company’s focus on strengthening its brand visibility and engaging more actively with channel partners is translating into improved customer loyalty and trust.

- The recognition of the company’s “UDAAN” loyalty program for the third consecutive year is a testament to its efforts in building strong relationships with its plumber partners.

Top 3 Takeaways:

- Aggressive capacity expansion plans, with the new Begusarai plant and debottlenecking of existing facilities, to cater to the growing demand.

- Unwavering focus on volume growth and market share gains, despite short-term margin pressures.

- Robust industry tailwinds, such as favorable government policies and growing demand in key end-user segments, provide a positive outlook for the company.

3 Likes

- Revenue grew 9% YoY to Rs. 604 crores in Q1 FY25

- Volume growth of 14% YoY, reaching 42,180 MT

- EBITDA grew 29% YoY to Rs. 58 crores

- PAT increased 25% YoY to Rs. 25 crores

- EBITDA margin at 9.6% for Q1, lower than usual due to product mix and higher branding costs

- Management maintains long-term EBITDA margin guidance of 12-13%

- Working capital days reduced to 80 days from 95 days in March 2024

- Receivable days improved to 61 days from 83 days

- Inventory days increased to 70 days from 52 days

- Aggressive branding and marketing initiatives undertaken

- Expanding bathware segment (Aquel by Prince) across all zones in India

- Continued focus on strengthening distribution and brand

- Strong demand across agriculture, plumbing, and infrastructure segments

- Industry experiencing consolidation, with larger players gaining market share

- Affordable PVC prices driving volume growth

- Real estate and infrastructure sectors performing well

- Potential anti-dumping duty on PVC could impact raw material prices

- Begusarai plant in Bihar to be operational by January 2025, adding 45,000 MT capacity

- Additional 35,000-40,000 MT capacity being added across existing plants

- Total capacity addition of ~80,000-85,000 MT in next few quarters

- Management confident of sustaining strong volume growth

- Aiming to be among the fastest-growing players in the industry

- Long-term EBITDA margin guidance of 12-13% maintained

- Focused on improving working capital management, especially receivable days

- Optimistic about industry growth prospects for next 2-3 years

- Opportunities in growing market share due to industry consolidation

- Risk of inventory losses if PVC prices continue to decline

4 Likes

Thanks for the update.

Capacity addition amounts to ~25% of current capacity.

Double digit vol growth is always encouraging.

Looks like this should (in the best case) keep growing >15% in the next few years if everything goes as expected. Valuation could be better though.

Invested.

2 Likes

Latest Conference Call Highlights – Key Points

- Outlook:

- Weak volumes in Jun-Jul’24; recovery in Sep’24.

- Muted Oct’24 due to festivities and channel destocking.

- PVC price rise from Nov’24 expected to drive restocking and volume growth.

- Strong end-consumption demand supported by infrastructure, urbanization, and government policies.

- Guidance:

- FY25 volume growth: 8%-10%; margins: 12%.

- Bathware FY25 revenue target: ₹250mn, breakeven by 3QFY26.

- PVC Prices:

- Declined 16% QoQ in 2QFY25 but now stabilizing.

- Channel Destocking:

- Caused by PVC price volatility; restocking likely from Nov’24.

- Volume Growth:

- 2QFY25 volumes grew 4% YoY, led by Plumbing and SWR segments.

- Growth impacted by destocking and monsoon.

- CPVC maintained strong performance in 1HFY25.

- Realizations:

- Flat QoQ despite lower PVC prices due to improved product mix.

- Inventory Loss:

- ₹120-150mn inventory loss in 2QFY25.

- EBITDA Margin:

- Impacted by trade incentives (2%-2.5%), inventory loss, bathware losses (₹30mn), and lack of operating leverage.

- Trade Incentives:

- Provided in 2Q and continued through Oct’24 to boost volumes.

- Bihar Plant:

- Phase 1 operational by 4QFY25; 55 kmtpa capacity.

- Reduced freight costs and strengthened supply chain in East India.

- East India Market:

- Focus on branding (Durga Puja installations, plumber training).

- East India seen as a high-growth market due to delayed urbanization.

- Branding Initiatives:

- Expanded visibility through travel modes and upskilling plumbers (1,848 trained in 2QFY25).

- Bathware Segment:

- 2QFY25 revenue: ₹70mn, EBIT loss: ₹30mn.

- Pan-India presence expected by 2HFY25; breakeven by 3QFY26.

- Tanks:

- 2QFY25 revenue: ₹120mn; 65% of the market remains unorganized.

- Capex Plans:

- FY25 capex: ₹3.3–3.5bn (Bihar expansion, maintenance, bathware acquisition).

- Bathware maintenance capex: ₹50-70mn over 12 months.

- Working Capital:

- Inventory days high due to muted demand in 2Q.

- Normalized inventory days of 65-70 and receivable days <50 by FY25-end.

- Brand Spend:

- 2.5% of revenue for 2Q/1H/FY25E.

4 Likes