More observations

Receivables have jumped 4.5x vs sales of just 2x between fiscal 17 vs fiscal 21

Payables have jumped 3x in the same duration

Inventory too by 3x

Cash have jumped 8x, which puts a question mark on efficient capital allocation and utilization.

There is a mismatch in the loan amount between the closing balance of 16-17 & opening balance of 17-18

There is a dilly dallying of remuneration for the promoters. Why the company has decremented the salary in 17-18 & 18-19 when sales as well as profit has grown?

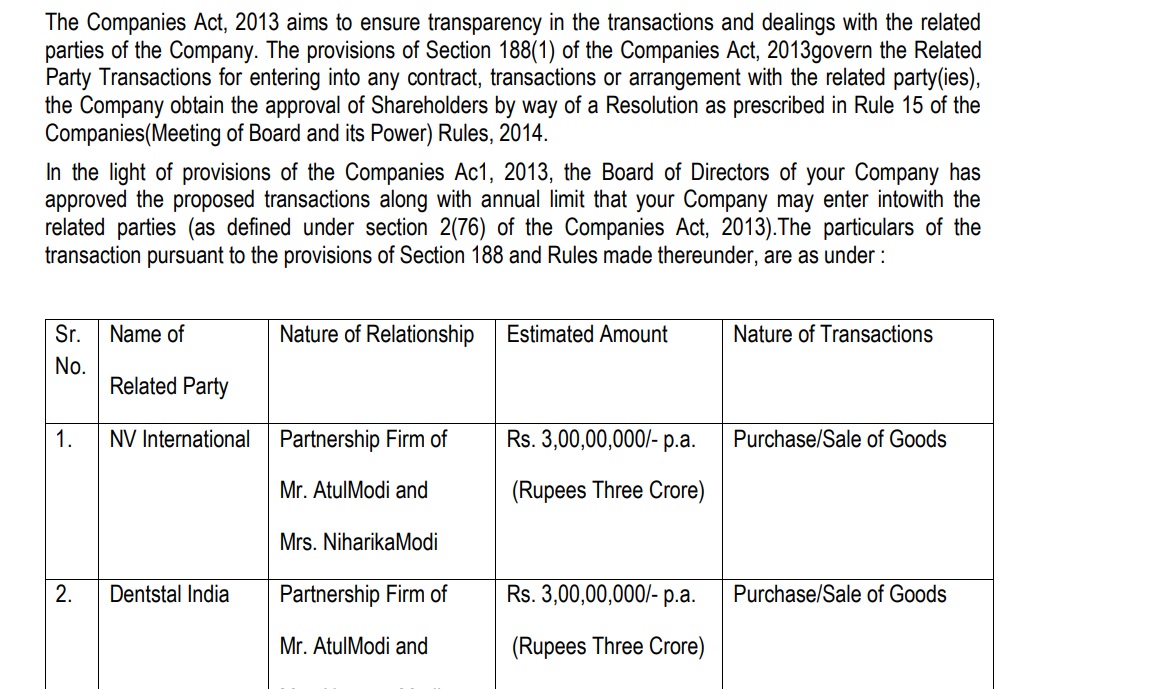

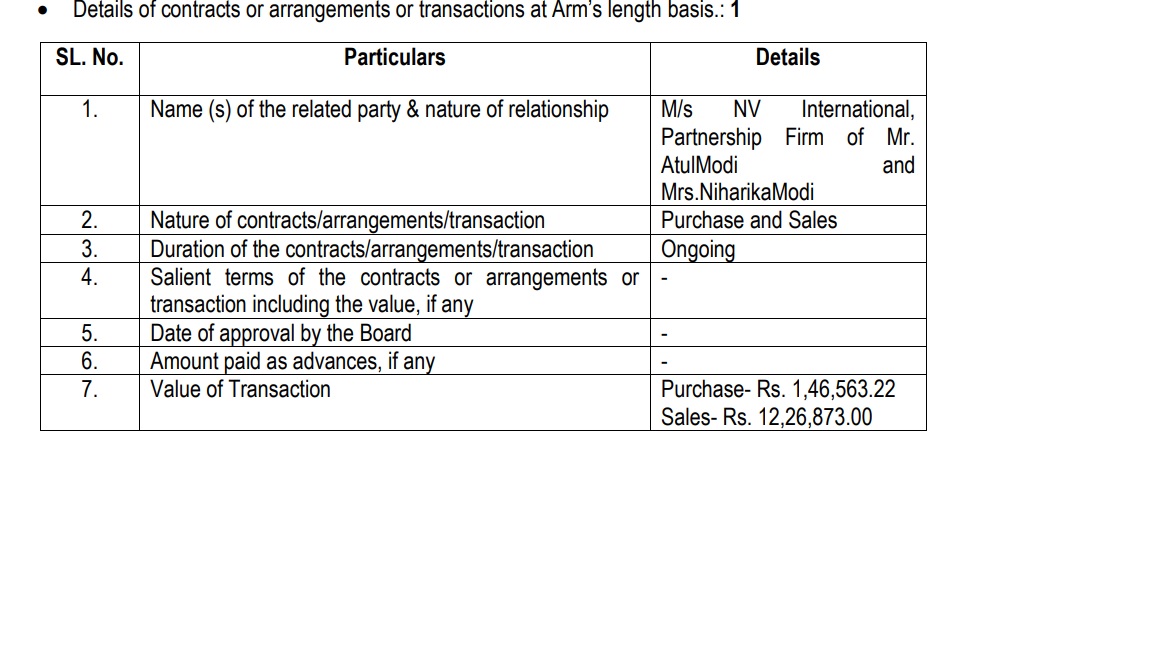

Related party transaction makes 20% of the the turnover for the previous fiscal

There is component like other expense unit 1 in 17-18 which accounts for almost 10% of that years profit

There are 3 BS and PL statement for 15-16 one at page 20, another at page 23 & one at page 32 and all with different numbers. Same with fiscal 16-17.

Somehow i couldn’t tally up the P&L numbers with the BS numbers. Hence for the time being i have put my buy decision on hold. Will observe for couple of quarters and then might take the call

It seems they have received export excellence award by Federation of Indian Exporters Organization. I believe every such government organization/body have access to detailed export data and verifies the export data submitted by any company participating in the award before giving out award. Though I haven’t checked the exact process of FIEO for selecting awardee.

Please check slide No. 15 of latest investor presentation.

I have listened to their 2 conf calls and did little bit of scuttlebutt on this. My sense is that to win doctor’s, they will need to do lot more marketing than currently being done. This is becoz you are competing against MNCs who have deep pocket. So I agree with comments on this thread that it will take time and will have to see how they walk the talk.

Hi Rudresh,

I was trying to find out related party transactions for previous fiscal as mentioned by you.

But according to AR of 20-21, related party transactions are sales 146000/- and purchase 12,26,900/- with NV International. For approx. turnover of 28Cr this does not even amount to 1% of revenue. Am I missing something? Or do I need to check at other regulatory filings? Please let me know.

Or is it that you are considering the maximum limit granted by board for related party transactions for the year into consideration. that is 3CR each for 2 firms owned by mgmt.?

The management’s repeated use of positive adjectives to describe their business seems boastful. Further, FDA approval doesn’t translate to sales. They haven’t got the domestic market captured yet so, a lot needs to happen for them to deliver on their targets. The management is betting that being a low-cost competitor will translate to sales. Nothing happens by itself. This is a big execution play.

Disclosure - Tracking closely. I will invest only when I see market share improve domestically and the management delivers on its export promises (primarily US and EMEA)

The way I understood from the management commentary that, they are actually betting on exports with various approvals and certifications in both regulated & un-regulated markets and not aiming much on the domestic side due to intense MNC competition ?

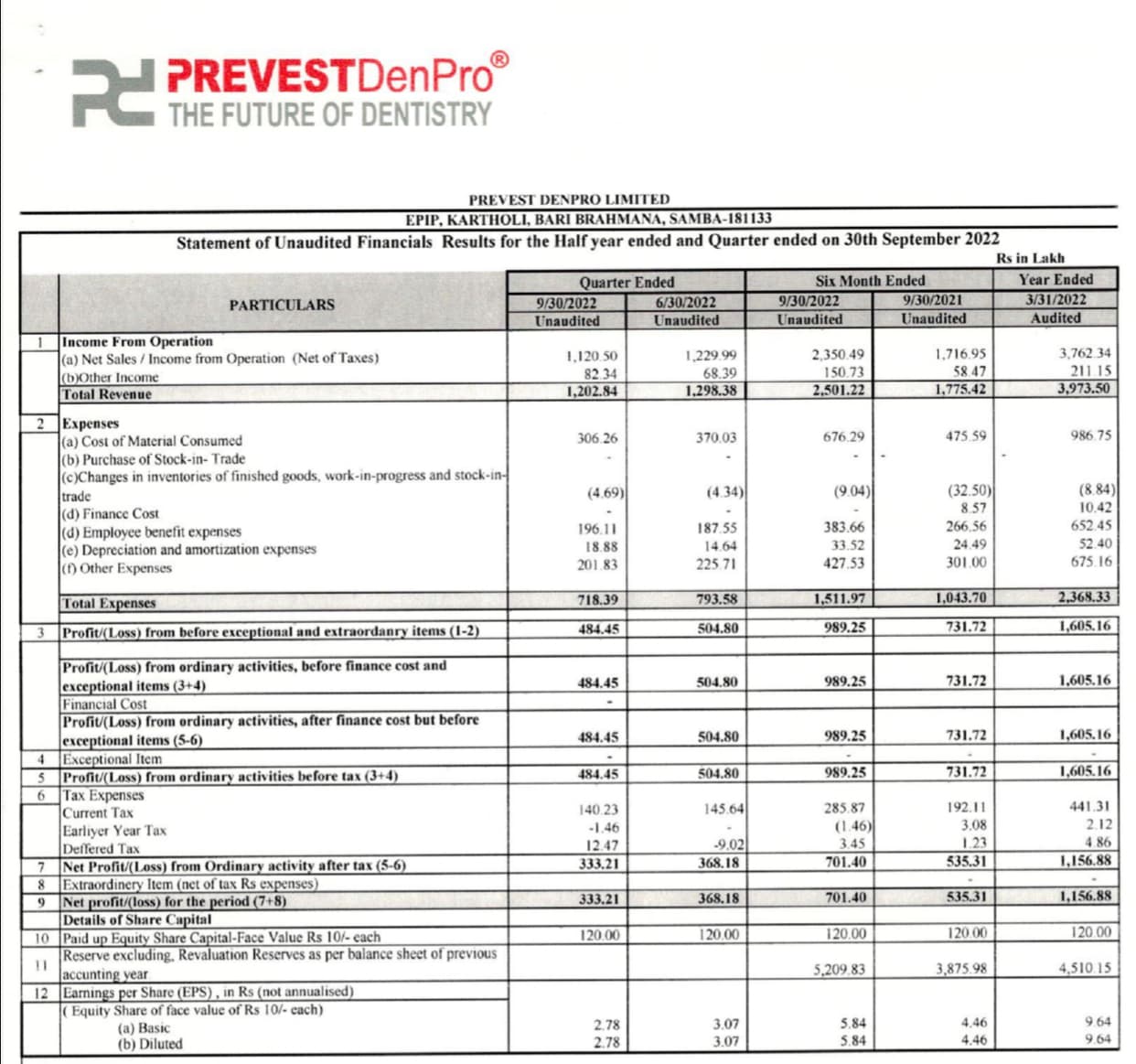

Conservatively assuming all remaining quarters of FY23 have same EPS as 1QFY23 (Rs3.07) FY23 EPS likely to be Rs12.28 implying stock trading at 27.4x FY23 at Rs337 which is very reasonable for the kind of growth expected in Prevest

Commenting on the earnings, Mr Atul Modi, Chairman and Managing Director at Prevest DenPro, said that "The Company has shown strong set of numbers for the first quarter of the financial year 2022-23 and we expect the healthy trajectory of performance to continue. We are moving in the right direction. Prevest DenPro’s products are sold in more than 80 countries and India contributes only about one third of our revenue. We are creating a big buzz globally and planning to contribute more in

India’s journey of becoming ‘Atmanirbhar’ (self-reliant) in the fields of dental materials. We are geared up for producing hygiene, oral care, and bio-materials products, and the quality will continue to remain our prime focus," Mr Atul Modi added.

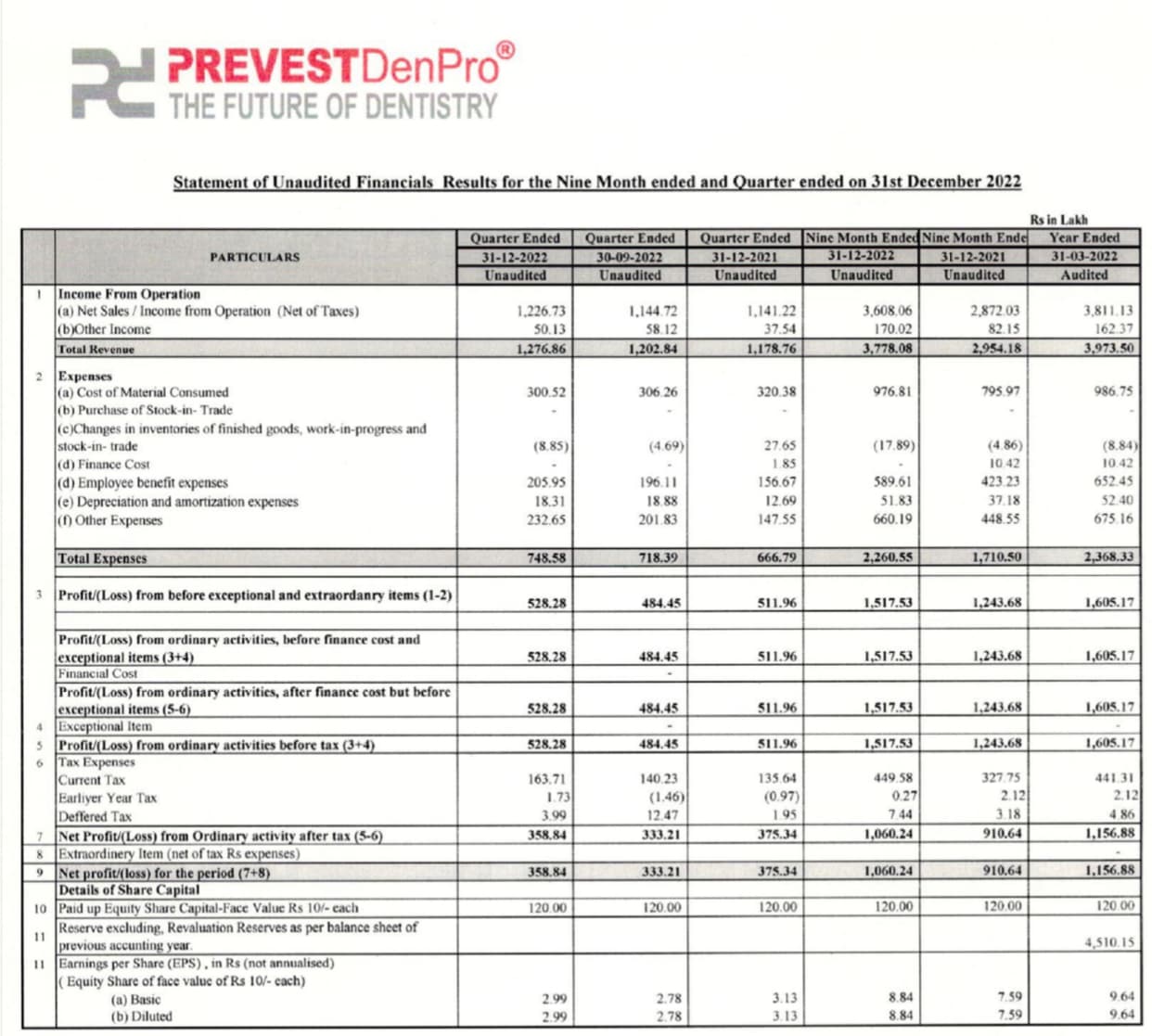

Material cost in this quarter has increased drastically from 25% in December quarter to 30% in current quarter. No explanation provided by management in IP or concall.

It looks the rise in material cost is in line with inflation. All prices are rising, so is the material cost may be. The key here is whether prevest can pass on these to the end consumer.

The management has explained that revenue in the present quarter has been impacted due to new licensing requirements, application w.e.f. from 30th September. Take away from concall:-

R&D facility has become operational. The new manufacturing facility is likely to be operational by Q4.

New manufacturing facility will be fully operational by next year and may contribute 25 Cr. to the topline.

Expected US export revenue is 10 Cr. next year.

Both the domestic and export sale is growing at a healthy rate of 30-40%.

Management has been forthcoming with all information. Happy reading. Prevest Concall.pdf (3.1 MB)

What impacted sales in 2QFY23?

Dental material comes under the category of medical device and all medical devices have come under the Medical Device Regulation that is MDR. All medical devices manufacturers have to obtain manufacturing licenses from by 30th September 2022.

Prevest is the first Indian manufacturer of dental matenal that received the manufacturing license well within this speculative deadline as by the CDFCO. Now they can freely manufacture and export dental material. Export dispatches were held up after 20th September due to delay in issue of the manufacturing license and some of the orders due for September were rolled over to 3QFY23.

USA website of Prevest Denpro is functional. Prevest DenPro USA Inc. is a wholly-owned subsidiary of Prevest DenPro Limited, India. The primary objective of the company is to provide top quality materials to dental professionals in USA.

Considering slowdown in export market, the results are spectacular. Once some sale starts trickling from USA, we may see a quantum jump.

Key takeaway from investor presentation:

-Research and Development centre is ready.

-They have developed raisin for 3D printing.

-New manufacturing facility shall be opearational by 2024.

-They have already received USFDA approval for 20 products. They have SFDA approval for Saudi Arabia, and MDSAP certification.

-Indian Dental Market is likely to grow at a compounded growth rate of 20-30%.

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.bseindia.com/xml-data/corpfiling/AttachLive/149fb83b-d0fa-4363-bc39-69e9d88c6c28.pdf

On Q2 rolled over orders

Those orders were small in qty, were served in 1st mth of qtr. Some Europe orders were impacted. We still grew by 7-8%. No details given on impacted European orders

On Guidance

50cr rev guidance for entire fy23 (in line with earlier projections)

min. 25%-30% growth expected next yr

sustainability of ebitda margin (40%)? - will be maintained in future. Will continue to add value added products

On US Market

When will it fire? - attended exhibition in US, signed an agreement with a US based company worth $1.7M (~14 cr) to supply products for next 5 years - have started execution - have got advanced payment for 1 order - expecting multiple orders spaced out in 4-5 years from this co as part of deal

Other companies are also there; we are selective at the moment - in advance stage of finalizing agreement with 2 other companies - we cannot quantify today - but once it is finalized we will inform you - there are lot of companies - they need long term agreement so that they are assured of supply. We are looking for min $1M contracts with these companies

On Succession planning

Next generation will soon be involved in the business - not involved presently

On Other markets

Started the process for registering our products in Canada; tough market

40% growth yoy (9 mths) in domestic market, it’s a growing market

Other Asian countries to whom we supply - bangladesh, philippines, indonesia, sri lanka, malaysia, vietnam

Named few European countries too including Russia and Netherlands

On New facility (for sanitizers, mouthwashes etc…)

New facility for new products, 16ksqft fy24 - how much topline will it contribute? - facility will be ready by end of this FY, but will be usable in next FY because lot of regulatory compliances need to be fulfilled. Upon fulfilling compliances, we expect to do 10-15% capacity utilization in 1st year & generate 3-5cr; marketing these new products will take time

What is the max revenue you can generate from this new facility - it will take time in selling those products; it’s a new line - in 3-4 years we will get there with 50% utilization (50cr target to marketing team); 75-100 cr. we can generate , but capacity can be enhanced, and also product mix (high value added) change can generate higher revenue, tough to quantify at this moment. 75 cr is a conservative estimate at 100% utilization

On Differentiation/Comp adv. & Entry barriers

Differentiating factor → pricing due to low cost, quality at par with MNCs

What about competition from domestic players in future since margins are juicy? - quality, R&D - no facility out there that can compete except MNCs - even if it comes, we can beat with quality and pricing

Entry to barriers - inhouse formulations - learning curve/experience/expertise - it takes time to establish - now we are doing innovation with R&D dept

On products not being popular with top tier dentists

how are you trying to win over top tier dentists to use prevest products over 3M, sirona dentsply etc…? - free samples, trying to win them. Secondly, its not that none of the top tier dentist use our products

Dr. Sai, director with prevest, also a dentist & professor says that - dentist have a perception that intl. brands are better than Indian brands, they hv been trained on European brands. That is why we are giving our products to dental institutes to fix the problem at the core - it takes time to change the perception, can take 5-6 years

On products, market etc…

Top 20 products contributing to 80% of revenue; rest of the products are just complimenting these top products

140 distributors - 90 dealers for intl market, 60 for domestic mkt

Materials market - domestic mkt is ~1000cr; Intl market data not available, but much bigger than domestic mkt

My read is that topline numbers are the key monitorable here. Mgmt. is super bullish on 25-30% growth as always. In sync with earlier guidance for FY23. But, last 4-5 qtrs. have been flattish and hence next 2-3 should be imp from that perspective.