It varies from company to company. For eg, I was invested in a small cap real estate firm…Asiana Housing…they recognised revenue after receiving full amount against a particular flat. (PS not invested anymore)

Most of the companies, however, recognise revenue on flat’s booking.

Prestige Estates upcoming launches expected to have a Gross

Development Value of 752,000 crore, potentially resulting in pre-sales of ‹20,000 crore to ‹22,000 crore.

Issues with approvals for most of the real estate plays. Overhang and dead inventory may arise or might have arisen due to such developments.

But short term pain for a long term investor in real estate businesses. All due to elections last year

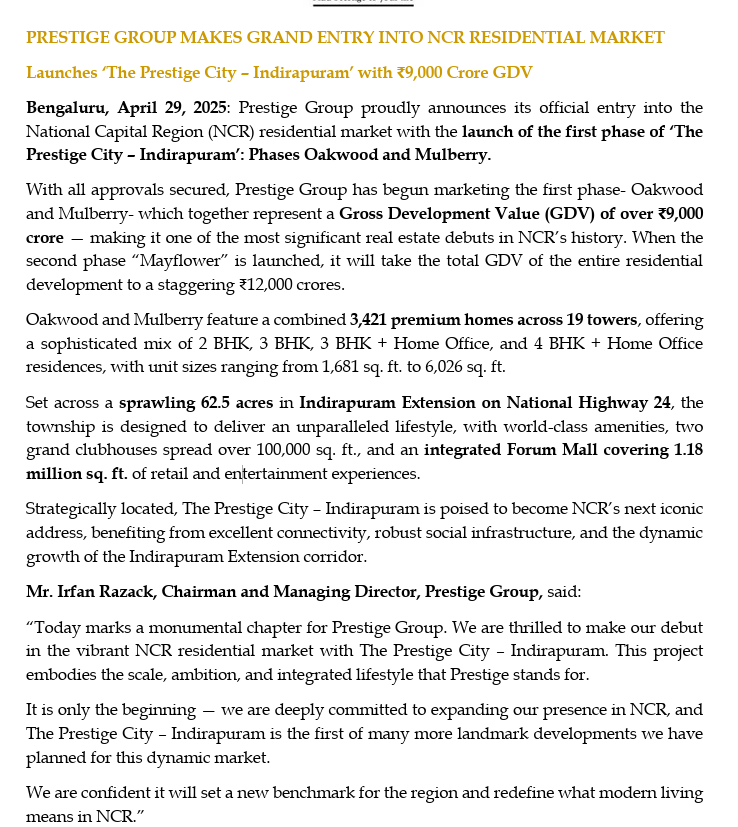

In my view, Indirapuram stands out as the highest ROI project, not merely due to its higher GDV but primarily because it falls within the mid-value segment rather than luxury.

One key challenge with luxury projects is that, despite higher margins, collections take longer, leading to inventory buildup and impacting the ROCE. This is evident in the management’s commentary as well.

For instance, in Q3FY25 Concall, the management stated that they expect ₹2,000 crore in pre-sales from the Nautilus project, which has a GDV of ₹8,600 crore and an average GDV per sq ft of ~₹30,000 per sq. ft (Source: Investor Presentation) making it a luxury segment. This translates to a pre-sales percentage of just 23%.

In contrast, for Indirapuram, they anticipate ₹5,000 crore in pre-sales on a GDV of ₹11,500 crore, reflecting a significantly higher pre-sales percentage of ~43%.

It may seem like a very cursory question - But I want to understand how does Prestige recognises revenue? I heard Irfan say in an interaction in some projects they do it on Percentage Completion and on some projects on completed method. Want understanding on this

As per the Annual Report, the Company recognises revenue from the sale of real estate inventory property at a point in time either upon transfer of legal title or handing over of physical possession to the customer, whichever occurs earlier. However, in the case of JDAs, where the landowner is entitled to a share of constructed area or revenue proceeds, the Company recognises revenue over time using the % of Completion method.