A personal observation about CLSA’s re rating calls. In past CLSA had said Tata power will go through a poor re rating cycle and that the stock will fall from then CMP of 250-280 Rs band to 180 Rs. I hold a good position in tata power and i didnt sell. Every sign about company was positive and management’s commentary was very promising. I hold on and even added on dips. The stock eventually moved up and today stands beyond 400 Rs.

Since then, i made a mental note. Look at CLSA calls but dont trust them!

Though i am positive about Prestige and I am invested. Here are other broker and fund houses calls that i have collated:

Rating calls have no accountability. It’s best to look at who the individual analyst is and how their thesis and the price has fared, if there is a correlation.

Most analysts have to follow multiple sectors and jave a target set of reports right after a quarter or earnings call. It’s done like a factory. A lot of them are kids (2-5 years of work experience), you can check profiles on LinkedIn.

Find a good analyst and follow them. Best is find someone in your circle who works in the industry, they can explain how things work and you’ll get an insiders view also.

The best way to analysis is just get through last Investor Presentation , couple of concalls and last 6 month management interview (Mr.Irfan Razak & teams) you will easily understand the sector and Prestige estate future prospect, Real estate cycle in midway it will easily last another couple of year say 3-4 year , just compare the presales date and future launches ,existing land bank etc. Do your own analysis before investing.

It recorded sales of ₹40,226 mn during Q2 FY25 (as against ₹70,926

mn during Q2 FY24). For H1 FY25, the sales sum up to ₹70,522 mn (as against

₹110,073 mn during H1 FY24)

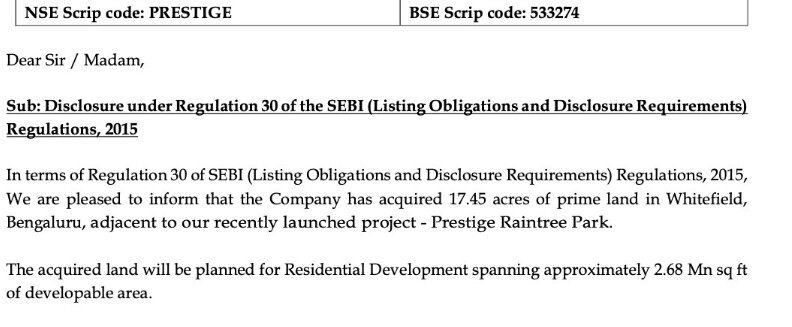

Prestige acquires 17.45 acres of land in Whitefield, Bengaluru to develop

residential project spanning over 2.68 Mn Sft. The cost of acquisition is around ₹462 Cr.

This is a detailed summary of the Prestige Estates Q2 FY23 earnings call focusing on the points requested.

Financial Performance

First half revenue was 4,448 crores, with EBITDA of 1,791 crores, reflecting an EBITDA margin of 38.43%.

PAT for the first half was 541 crores, with a margin of 12.18%.

As of September 30th, net debt was 3,592 crores, and the debt-to-equity ratio is down to .21.

Margin Guidance

EBITDA margin guidance for the new launches in H2 FY23 is 35%.

PAT margin on new launches in H2 FY23 is expected to be around 15% to 18%.

Business Segment Performance

Office Portfolio: Leasing activity remains robust with a 90% occupancy rate across the existing portfolio.

Exit rental for the office segment is projected to reach 3,326 crores by FY28.

Retail Segment: Strong performance in all malls with an occupancy rate of 99.2%.

Exit rental for retail is expected to reach nearly 1,000 crores by FY29.

Hospitality Segment: Operating hotels delivered revenue of 415 crores, with a gross operating profit margin of 44%.

Revenue in the hospitality segment is projected to reach 2,346 crores.

Management Guidance for the Future

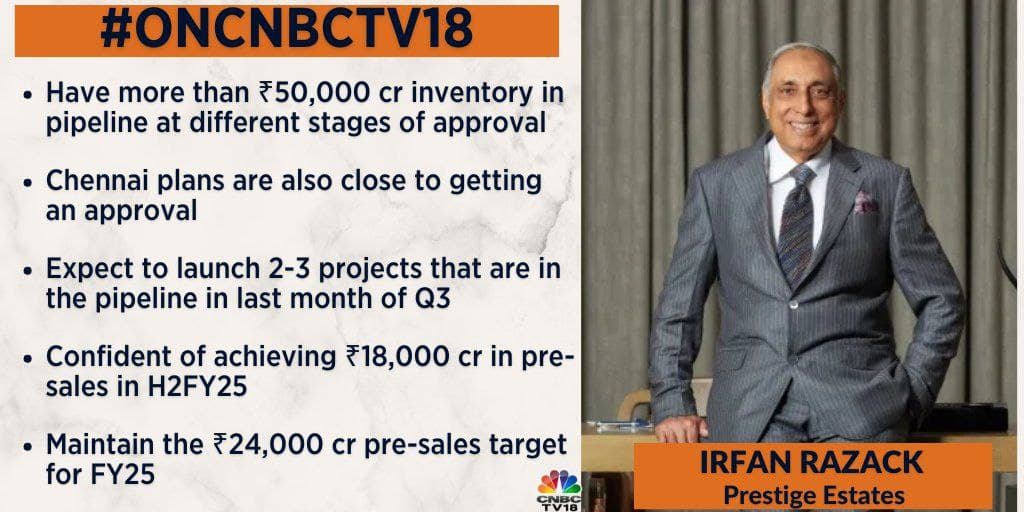

The company is working on several business development opportunities that will be added to its pipeline.

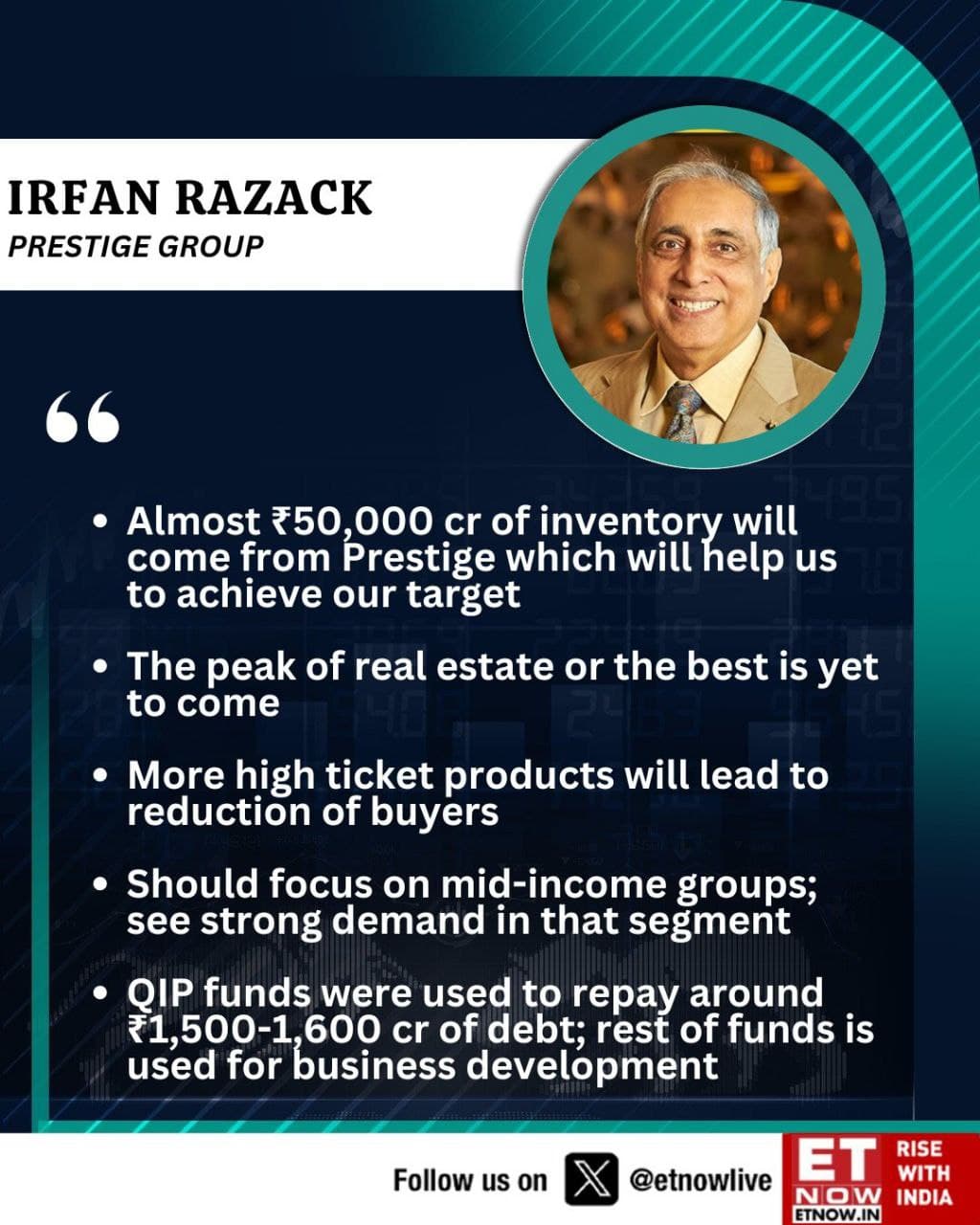

Management expressed confidence in achieving the pre-sales guidance of 24,000 crores for FY23.

They expect strong pre-sales in H2 FY23 due to a robust launch pipeline.

The company is focusing on disciplined growth and delivering sustained value to its stakeholders.

Key Risks in the Business

Delays in Obtaining Approvals: The management acknowledged delays in obtaining approvals, which is a concern for the timely launch of projects. They expect the situation to improve after the elections in Maharashtra.

Potential Oversupply in H2 FY23: There is a potential risk of oversupply in the market in H2 FY23, as most developers are planning a significant number of launches during this period.

Industry Outlook

Demand for residential real estate continues to be strong, particularly in the mid-income segment.

There is a pent-up demand for projects in all the cities where Prestige Estates operates.

Key Highlights

Successful completion of the QIP in Q2, raising 5,000 crores.

Consolidation of stakes in related party entities, resulting in the addition of approximately 20,000 crores of GDV and 8,000 crores of EBITDA.

Plans for an IPO of the hospitality business are underway.

The company is focusing on maintaining its product quality and pricing discipline to ensure continued success.

This summary provides a great overview of the main points of the conversation. It accurately captures the investor concerns about Prestige Estates’ sales guidance and the company’s responses to those concerns.

Here are some additional details from the sources, which offer further insights into the conversation:

Prestige Estates is sticking to its guidance of 24,000 crores for the year, despite only achieving 29% of that target in the first half. The company leadership believes they can make up for the shortfall in the second half of the year.

The company attributes the lower-than-expected sales in the first half of the year to regulatory delays in obtaining approvals for new projects. These delays have impacted their ability to launch new inventory into the market.

Despite the delays, Prestige Estates emphasizes that there is a strong demand for their projects. They highlight that whenever they bring new inventory to the market, it “gets lapped up” and “gets sold off”. There is a “big pent-up” demand, with people reaching out to the company daily, including to the chairman directly.

The company plans to launch a significant amount of new inventory in the second half of the year. They mention specific projects planned for launch in Delhi NCR, Hyderabad, Bangalore, Goa, and Chennai.

Prestige Estates clarifies that their sales guidance of 24,000 crores does not include sales from their large-scale “Maki” projects. This is because these projects are focused on office and hospitality sectors rather than residential.

In response to a question about a specific land bid in Noida, the company leadership indicates that they are not participating in every opportunity that comes their way. They state that they are selective in their land acquisition strategy and will only participate in bids where the numbers make sense.

The company leadership emphasizes that they are confident in their ability to achieve their sales targets. They cite the company’s brand, bandwidth, and resources as reasons for their confidence.

Hi, I had query regarding the realty space? When does something get categories as Revenue in the Quarterly or Yearly numbers? When the apartment possession is given or even pre-sales is considered?