Below I present my current portfolio breakup of my stocks I hold. This is my first post here and requesting your feedback.

Most of these stocks are discussed in detail in VP and my rationale for investing in these are betting on its growth and potential in the upcoming years. I am looking at 30% annualized return in 3-4 years period.

Please advise if i am right on my selection of these stocks? Any tweaks required in terms of allocation?

I plan to add more on these in dips.

To enable us to advise you on whether you are correct in your selection, you need to first provide a rationale for each of the companies. “a bet on growth and potential” is not a rationale.

Intrigued by your target of 30% annualized return. What is the rationale behind you expecting this return? Have you checked what is the average last 5 year earnings growth for these companies for you to expect this return?

Its been a while i have updated this thread. I had to exit equity markets around end of 2017 due to some personal constraints and started investing again from last May. Nevertheless, I have been reading VP and learnt a lot during this course of time. Also in retrospect, had I stayed with my original portfolio my losses would be huge I believe. Below is my current portfolio built over last 1.5 years mostly after reading a lot of great advice from Hitesh G, Donald, Bheeshma, Yogesh and many others from this wonderful forum. I want to preserve capital and build a coffee can type portfolio while taking few calculated risks in the long run.

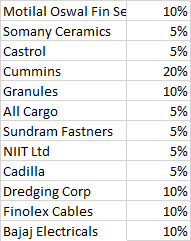

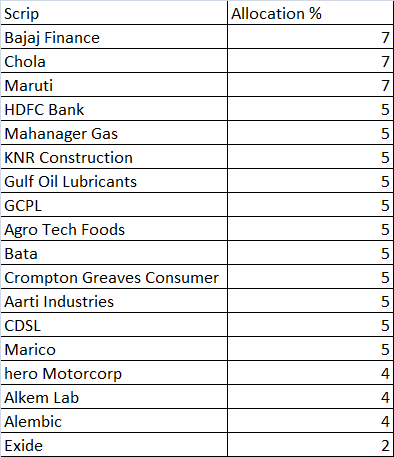

Bajaj finance - 7%

Leading Nbfc and excellent performance so far. Well equipped to cater quick loans in consumer durables and sme segment and a market leader. Holding for long term and adding in every decline.

Cholamandalam finance - 7%

A indirect bet on auto revival. A conservative nbfc run by well known murugappa group. This stock hasn’t corrected much during the last year and slowly building positions. My guess is that they will grow steadily over the years to come as they have strong tieups with many dealerships.

Maruti-5% - Market leader with more than 50% of market. Though there are good entrants like kia, MG Hector and Venue selling like hot cakes, the majority still will buy Maruti for its brand name and resale value. A long term holding and adding in declines

Hdfc bank - 5% - leading private bank, capable management and well run basically. Can compound well as long as growth is there.

Mahanagar gas - 5% - Huge network, infrasture already setup, monopoly in Mumbai area are positives. Sticky business and imo they have a long steady runway for growth.

Knr construction - 5% - Added as a bet on highway construction and infrastructure development. Their growth will depend on the future projects from the government . Many players around and closely watching this one.

Gcpl-5%- innovative company always launching new products. Though domestic market is not doing that great but their overseas market seem to be doing well. Can be a long term compounder.

Gulf oil lubricants - 5%

Small cap company and decent growth so far and hasn’t corrected much. Noticied when Castrol was posting poor numbers and this small cap company started posting good results.

Agro tech foods - 5% not a well known fmcg but they seem to be doing things right. MNC with unique product portfolio and market leader in popcorn. Their peanut butter is also quite good. Oil market seems crowded at the moment. Few new products in pipeline too. As consumer spending increases, there will be growth.

Bata - 3%- Household name in footwear. Strong physical and online presence. Their recent offerings are on par with the global brands and if they offer a new line in well made premium hand crafted leather shoes like Allen edmonds in US, they can create a niche and aid to further growth. Still remains as an aspirational brand for many in tier 2 and tier 3 cities.

Crompton greaves consumer - 3% - well diversified product portfolio. Though this segment seems to be crowded I feel there is enough pie to be had for everyone given the no of construction going around. A bet on consumer spending. Also like orient electricals who seem to be targeting the higher end of the consumer. Currently not adding any new positions.

Less than 6%

Apl apollo tubes, aarti industries, solar industries,marico

International mutual funds - 10%( 6% us based, 2% China and Japan respectively )

Debt and liquid funds - 10%

Cash around 25%

Exited all the international mutual funds with decent profits as us markets were at all time high and due to Corona implications in China. Deployed the proceeds in some new names and added to some existing positions. Will reassess in 3 months.

Latest Portfolio:

Increased allocation to hdfc bank, gulf oil lubricants, cdsl and reduced alkem and alembic allocation.

Also added whirlpool and Hul. Sold off Aarti industries and agro tech with profit and deployed in above.

Also playing around buying some put options to contain losses, so far it has worked well. If market falls further by another 10- 15% planning to sell out debt funds and deploy into stocks.

Watchlist : Nestle, Asian paints, Pidilite, Petronet lng, gmm pfaulder.

I haven’t updated here a while as I sold most of my debt and equity holdings and still sitting on majority of cash. Was playing on put options in March and arrested the drawdown of portfolio a bit. I had sold off Chola, Gulf oil, Maruti, exide ,hero,cdsl and knr completely in some amount of losses and trimmed my other holdings as well. The rationale behind this is to get rid of all cyclical and Nbfcs as the recovery seems to be longer and take some tax advantage of carry forwarding the losses . I was expecting market to further fall but it seems we are forming a base but only time has to tell if this is the bottom. Increased small allocation to alembic and alkem since pharma started turning around and the Outlook seems better. Current portfolio looks like this

Bajaj finance 3%

Hdfc bank 3%

Mahanagar gas 3%

Whirlpool 3%

Hul 3%

Marico 5%

Gcpl 5%

Bata 5%

Alkem 4%

Alembic 5%

Currently I am planning to wait out for a while and see how the lockdown extensions and return to normalcy play out and then take a call on where to invest and stay out of cyclicals.

Watchlist : Aarti industries, Vinati organics, Page industries, Trent, Asian paints, Pidilite, Nestle, gmm pfaulder, petronet lng, Reliance

Glad I am holding winners(most)and sold out loosers early.

Below is the updated portfolio. Since pharma seems to be coming out of a long downcycle, jumped on it last month after seeing that it’s not a dead cat bounce. Also observed the market favourites for a while aren’t participating in this rally so didn’t allocate more to them. Picked up few beaten down midcaps/small caps.

Updated portfolio looks like below.

Bajaj finance 3%

Hdfc bank 3%

Mahanagar gas 3%

Whirlpool 3%

Hul 3%

Marico 5%

Gcpl 5%

Bata 5%

Alkem 10%

Alembic 10%

Ajanta 3%

Solara 3%

Jyoti labs 3%

Petronet lng 3%

Bajaj consumer3%

Still sitting with some considerable cash and slowly will deploy in next two quarters if pharma continues the momentum.

With todays rally, i sqaured off all my positions in following scrips.

Chola, marico, gcpl.

No change in remaining positions. Will move the sold amount to liquid funds and going to wait for a while. Will trim more if we surpass 14k in next few weeks to reenter at better levels