About

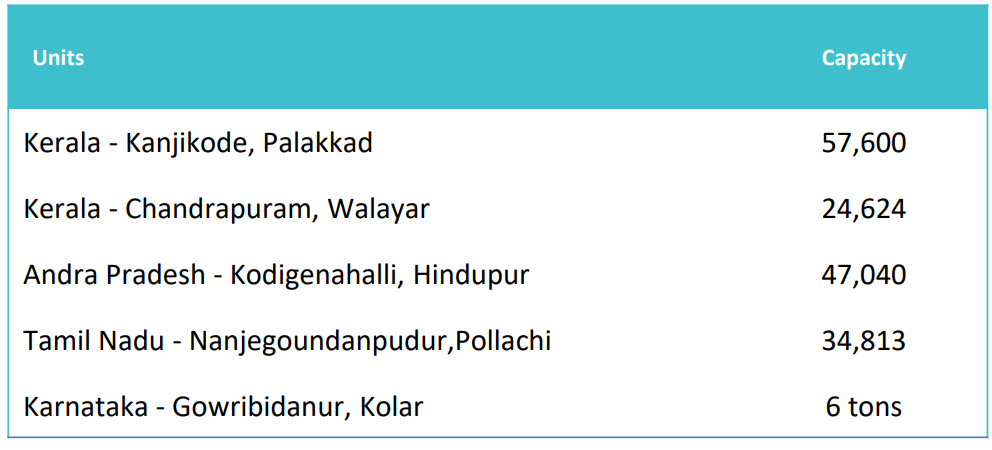

Precot Limited is in the textile industry since 1962 and is engaged in manufacturing of yarn and technical textile product. It has a vertically integrated business model and has units located in four southern states: Tamil Nadu, Kerala, Andhra Pradesh and Karnataka with a total spinning capacity of 1,63,000 spindle. They are one of India’s top suppliers of cotton products to textile mills, manufacturers and brands and aim to be the Market Leader in the Feminine Hygiene and Cosmetics Business.

It is in the B2B (Yarn and Threads to garment manufacturers and technical textiles) as well as B2C (Technical Textiles) business. They have in total 7 plants and a business presence in over 18 countries.

It generates it’s revenue from two segments -

- Yarn and Threads

- Technical Textile

Guidance

- Vision is to be the market leader in the feminine hygiene and cosmetics business.

- Aim to increase their revenue share in the technical textiles segment from 11% (historical) to 35% by FY25. Currently around 25% as of FY24.

- Plans to export to new geographies, such as MENA & Southeast Asia in the next 2-3 years through increased reach and marketing

- The technical textiles division will continue to be the driver for future growth

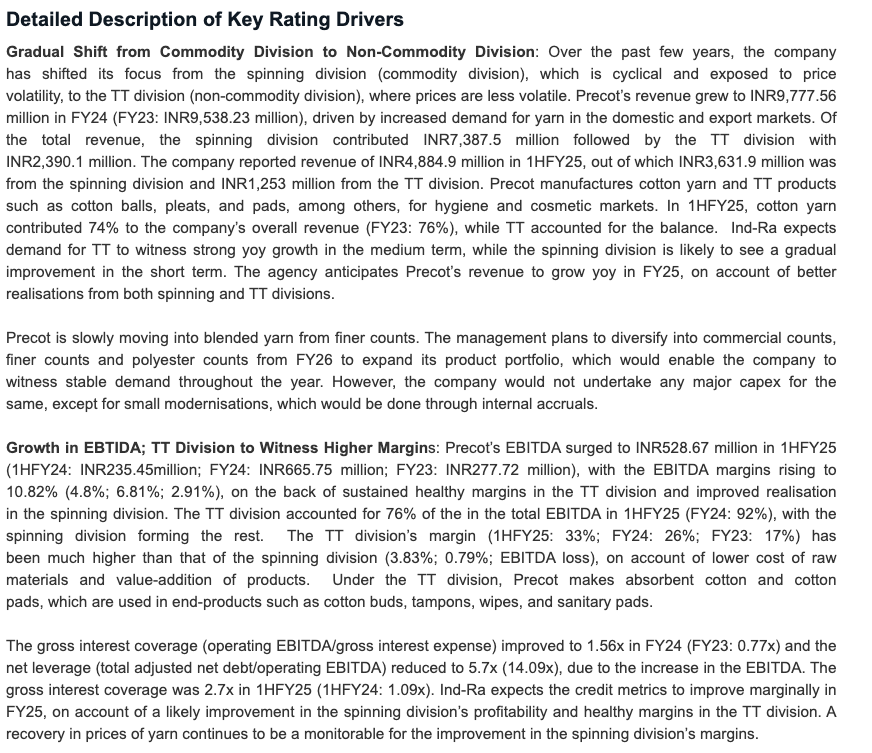

Product

Yarn and Threads

- Procedure of Cotton → Yarn

- 100% compact yarn enabled

- 1.65 lakhs spindles with a capacity of 70 tons yarn per day

- They have yarns and threads made from organic, BCI and normal cotton as well as polyester cotton blend.

- 100% Organic combed cotton Ring spun and Compact yarn for Knitting and Weaving Ne 20s to 60s

- 100% BCI Knitting and Weaving Ring Spun and Compact yarn Ne 20s to 60s

- Doubled yarns - Ne 20/2 to 80/2 (Knitting and Weaving)

- Gassed yarns - Ne 40/2 to 80/2, Ne 30/1 to 60/1

- Polyester Cotton Blended Yarn - Knitting and Weaving yarns with different blends - 20/80, 40/60 and 52/48 Count range Ne 12 to 40

- Polyester Sewing Thread - Bulk and mini cones in raw white and optic white

- Polyester sewing yarn ranges from Ne 20/2, 20/3, 42/2, 48/2, 55/2, 55/3 and 60/3

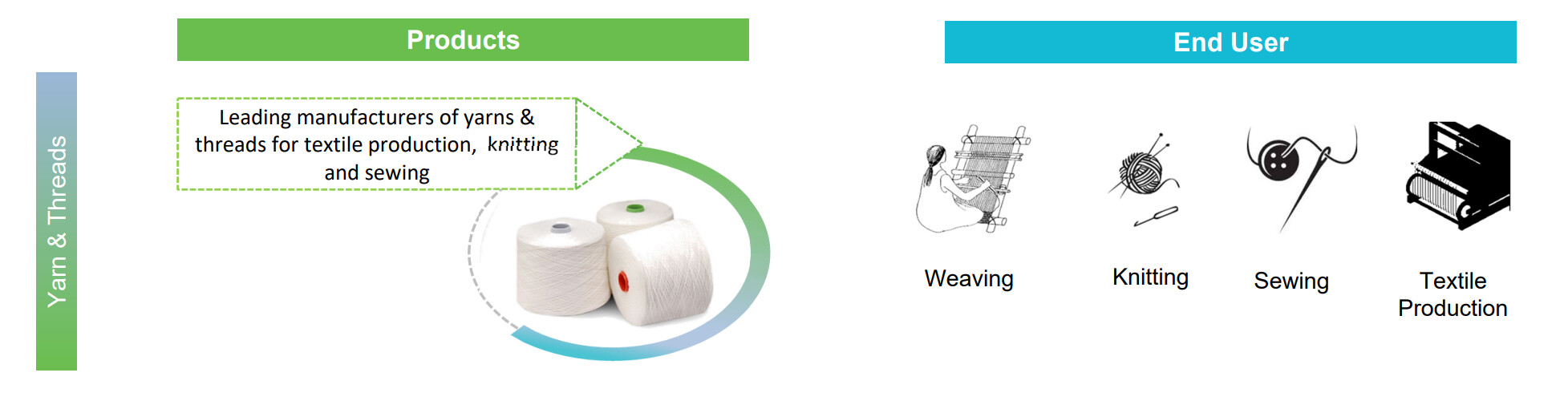

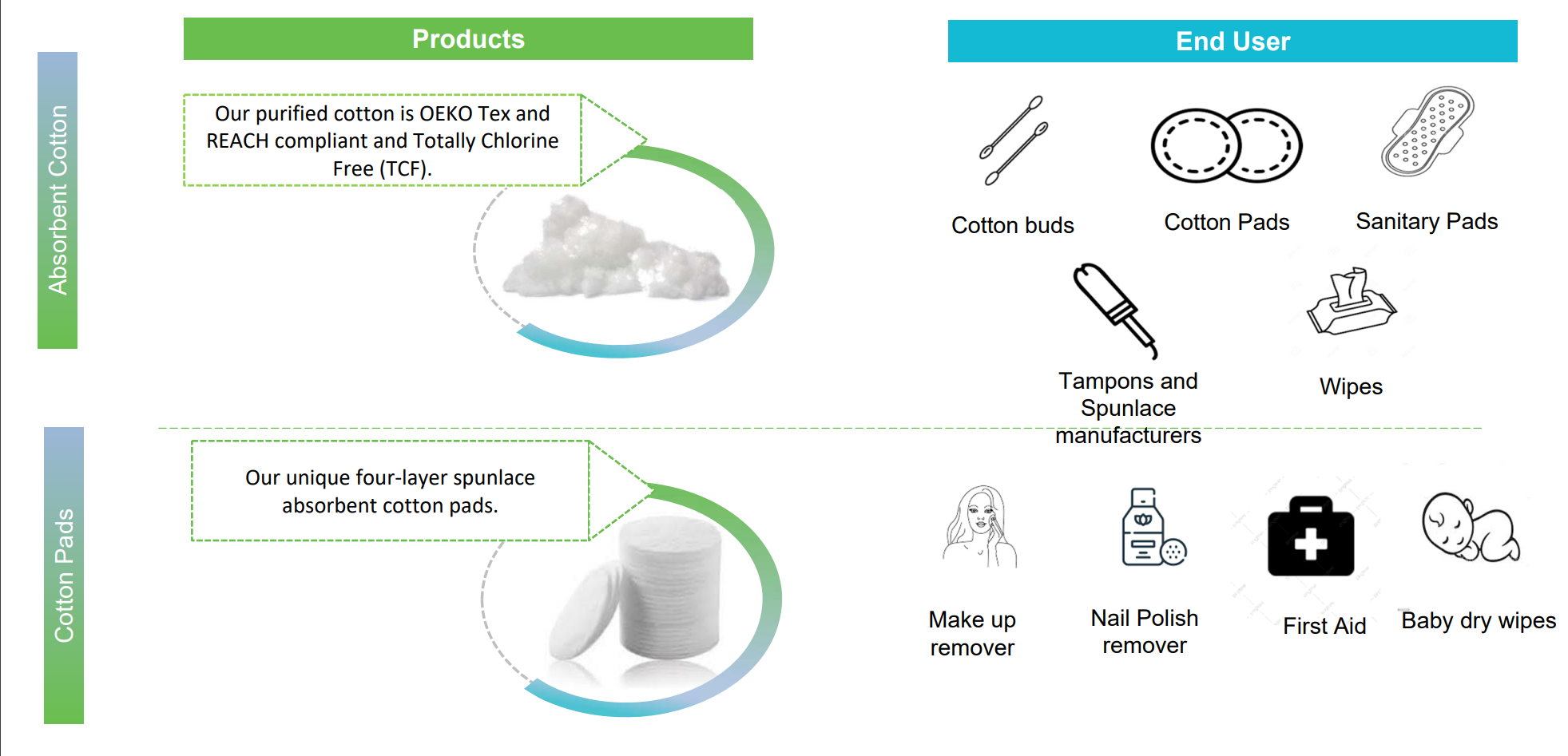

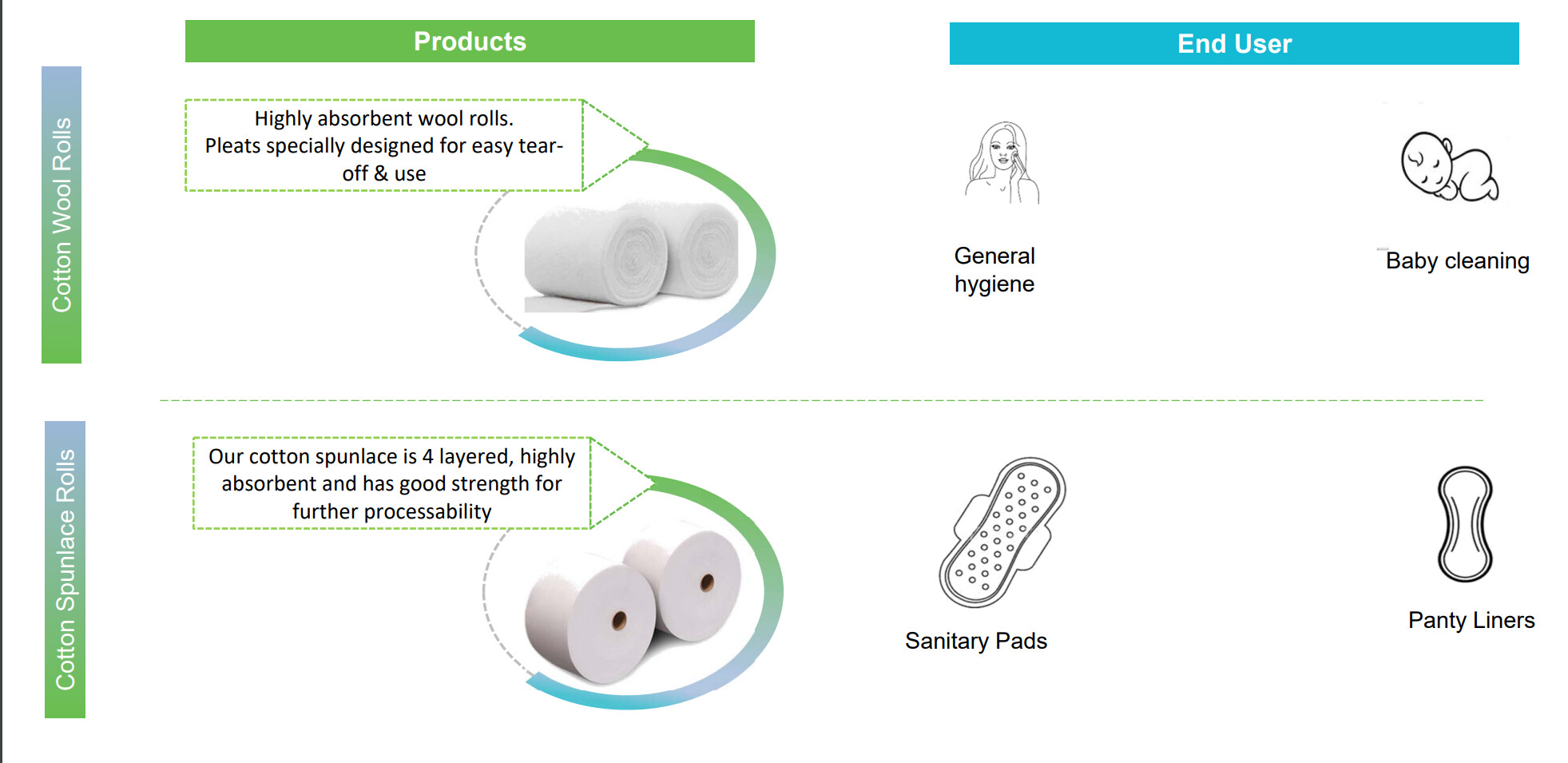

Technical Textiles

- The thread and yarn segment can be considered as the commodity segment while textile segment is the VAP.

- There is a 25.5% contribution (FY 24) from technical textile while the rest is from the Yarn and Thread.

- There is a robust demand for Hygiene products in overseas markets (VAP technical textile)

- They operate as a private label specialist, supplying their products to international retailers, distributors, and brands

Geography

-

Export stood at 47% while domestic sales was 53% in FY24.

-

Facilities:

-

Also have facility in Hassan, Karnataka (SEZ)

-

In 2013, the company set up a Greenfield technical textile with Spunlace Technology at Hassan in Karnataka and a planned capacity expansion is in progress and will come on stream during the second quarter of FY25

-

They are concentrated in South India, close to the source of raw material, skilled and unskilled labor, connectivity to ports and roads which helps them control logistic and other costs.

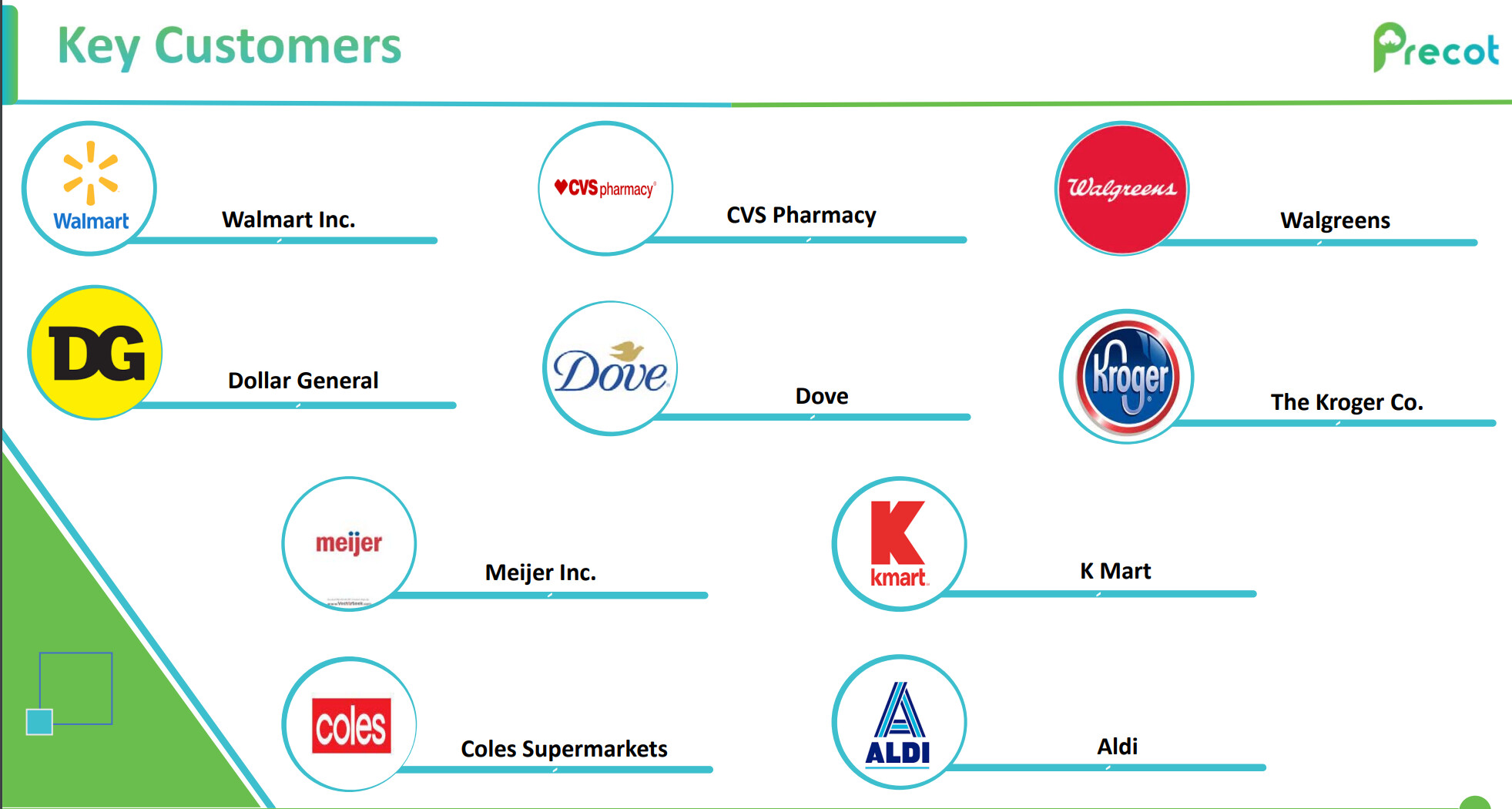

Customers

- One customer within India contributed to 6.89% of their trade receivables, while one outside of India contributed 8.47% as of March 31, 2024

- In FY23, 3 customers had 23.5% of their trade receivable in domestic share which has now reduced.

Raw Materials

- Cotton is the raw material from them and hence, the revenue and margins are highly dependent on it’s prices in the global market.

- 82.66% of the cotton consumed was from domestic market while the rest was imported in FY24 which was 69% in FY23

- 80% of cotton is procured domestically and balance from USA and Australia for Value Added products

- They aim to use sustainable cotton with fewer chemicals and optimum water; 20% of the cotton is organically grown.

- A sensitivity analysis reveals that a 5% increase/decrease in cotton prices would lead to a comparable negative/positive impact on profits, underscoring the company’s vulnerability to price fluctuations.

[Source]

- Their material cost have a lag of a quarter or two and margins have an extremely high correlation with the price.

- A problem which the management points out is with respect to cotton yields due to inferior cotton seed technology. The cotton import duty continues to be a pain point and is eroding the competitiveness of Indian spinners.

- There is also a price volatility, which they try to mitigate by hedging.

- They face competition from Bangladesh and Vietnam in the yarn market like all the other players in the market.

- They had losses in FY23 due to their spinning division.

- Indian prices did not fall even though there was a drop by 40% in international prices due to poor domestic crop.

- High raw material prices, inflationary pressures affecting consumer spending, and excess inventory in the supply chain lead to poor demand for their yarn segment.

- In FY24, they had a turnaround due to:

- Improved utilization (95% vs 72% in previous FY) and higher demand due to destocking bottoming out.

- Good growth in their Technical textile segment and raw material price cool down in Indian cotton.

- Focus on reducing finished goods stock and optimizing production across its spinning units.

Industry

-

Yarn and Thread Segment

- The global cotton yarn market size was valued at USD 82.81 billion in 2023 and is projected to grow from USD 86.11 billion in 2024 to USD 117.79 billion by 2032, exhibiting a CAGR of 4.0% during the forecast period. The cotton yarn market in the U.S. is projected to grow significantly, reaching an estimated value of USD 759.55 million by 2032. [Source]

- Indian government has launched different policies to promote the growth of the textile sector, which include schemes such as allowing 100% Foreign Direct Investments in the sector under the automatic route.

- Growth aspects include government support, improving demand in the apparel segment.

- Risks in this segment include higher prices over synthetic yarn, fluctuating cotton prices, commoditized and high competition. Many companies are moving up the value chain to expand their offerings and capture better margins up the value chain.

-

Technical Textile

-

National Technical Textiles Mission has been set up that aims at an average growth rate of 15-20% to increase the domestic market size of technical textiles to $40-50 Bn by 2024 [Source]

-

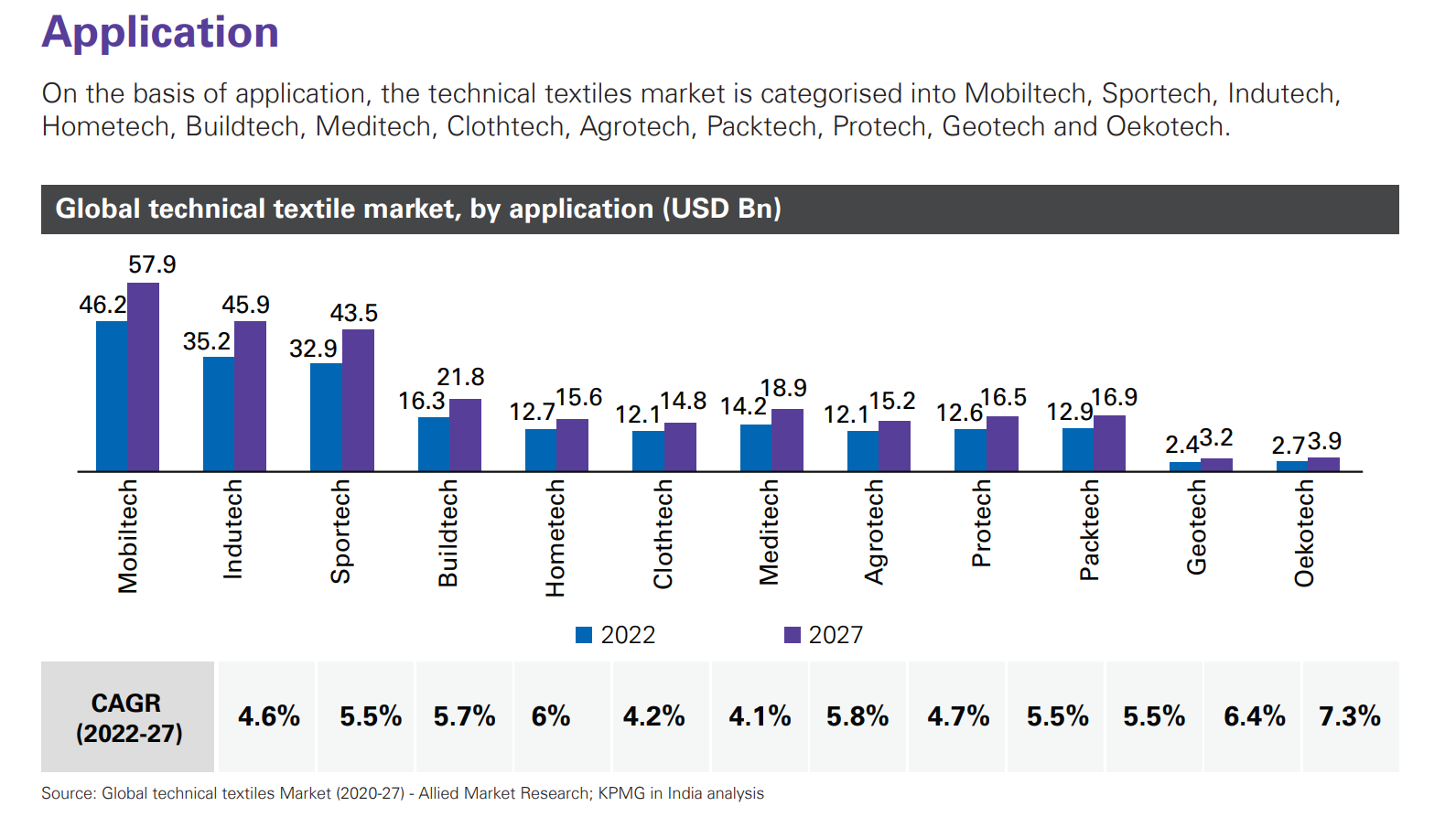

The global technical textiles market is estimated at USD 212 billion in 2022 and is expected to reach USD 274 billion by 2027, growing at a CAGR of 5.2% during 2022-27. The Asia-Pacific region is poised to grow fastest at a CAGR of 6%, reaching USD 102.6 billion by 2027.

-

There are two segments - Natural and Synthetic and the natural is expected to grow at 6% CAGR over the same period. This is due to rise in demand for ecofriendly and sustainable products across industries such as packaging, automotive, healthcare and others.

- In the past five years (pre FY22), Indian technical textiles market has grown at a rate of 8-10 per cent per annum.

- The penetration level of technical textiles in India varied from 5-10 per cent across different application areas compared to 30-70 per cent globally in 2021-22.

- The feminine hygiene products market size is expected to grow to $44.19 billion in 2029 at a compound annual growth rate (CAGR) of 7.7% [Source]. Precot aims to be market leader in the feminine hygiene segment.

- The demand for Precot’s product is expected to be high due to higher demand for hygiene products internationally, improving geographic mix, acting as a private label for companies.

- Key risks in the segment include high competition, raw material price fluctuation, skilled labor shortage, high export dependance, technological advancements.

-

-

I’m skipping over the details in the report as it’ll become a copy paste. I’ll highly suggest giving a read to it India 2047 – Vision and strategic roadmap for technical textiles

Notes

- Key strengths and opportunity include growth in their Technical textile segment along with it’s global demand, moving into VAP, government support to the industry, China+1, demand coming back in textile sector, export demand, focusing on branding and promotion.

- Key Risks and threat include cotton price fluctuation, high contribution of their yarn business in overall revenue, high competition, skilled labor availability, technological advancement.

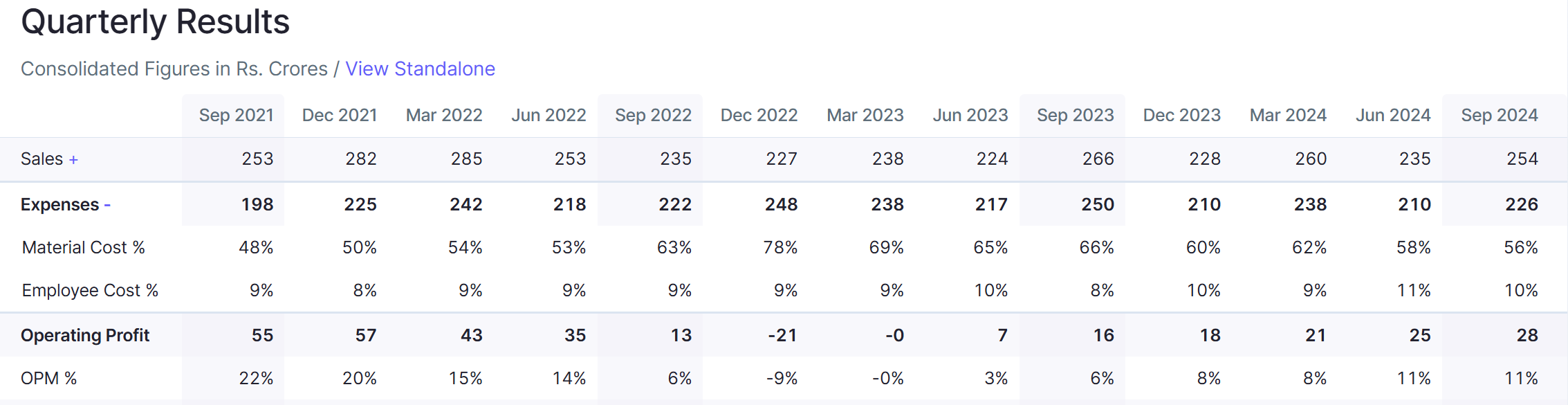

- They have a OPM of around 11% for the last 2 quarters however, one needs to track cotton prices for this company, their material cost keeps fluctuating quite a bit which in turn affects their margins a lot, atleast for now.

- The company is focusing on reducing cost in the spinning division by Continuous improvement in productivity, Yarn realization, Optimization of power consumption

- The capacity utilization in the spinning division improved to 95% (FY24) from 72% the previous year, leading to a 2.5% increase in turnover despite a 21% drop in yarn prices.

- The Company monitors its capital using gearing ratio, which is net debt divided to total equity

- Suprem Associates (Partnership firm) is one of the subsidiary however it has no operations

- 47% increase in export revenues from the Spinning Division was due to improved demand for value-added products in FY24.

- The credit period on sales of goods ranges from 21 to 60 days without security. No interest is charged on trade receivables up-to the end of the credit period.

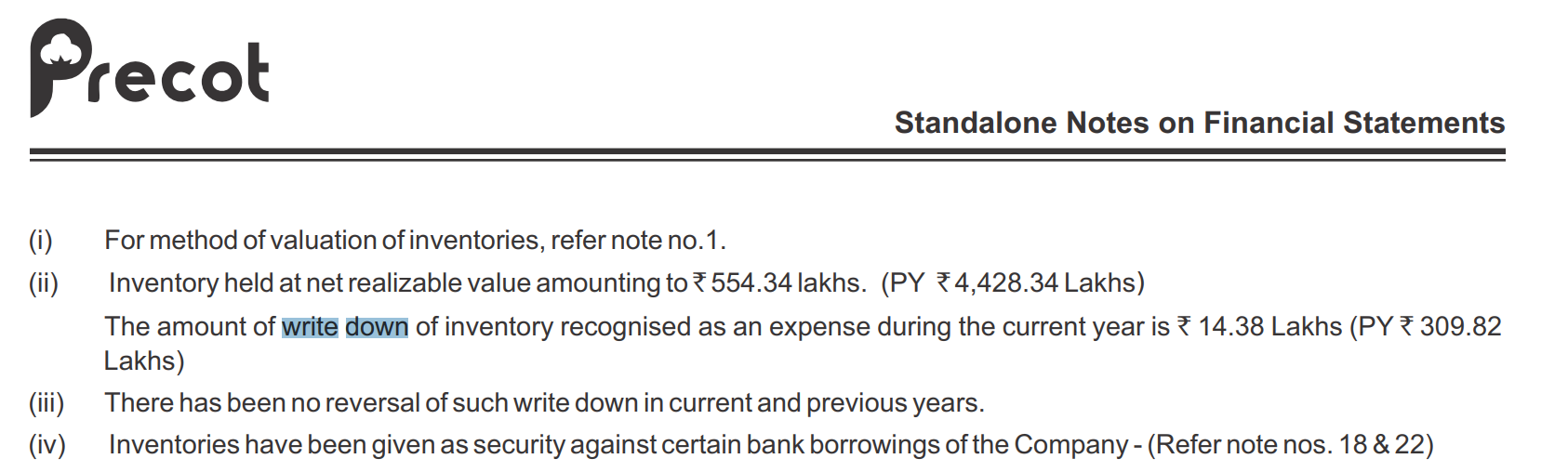

- An inventory provision is recognized for cases where the realizable value is estimated to be lower than the inventory carrying value.

Note: Most of the information is from credit ratings, AR, PPTs and some general reports about the textile sector. Not a lot of information is present for this company, I hope they do some concals in the near future.

Disclosure: Tracking position. My thesis for it is the textile sector growth coming back post the destocking issue, cotton price cooldown which should help them maintain margins and the company moving to better margins products; change in the product mix.